A theoretical Bank of Japan paper suggests that instability and herding in bond markets arises from low overall confidence of investors, great importance of public information (such as central bank announcements), and high value of privileged information. This analysis goes some way in explaining drastic bond market moves in the age of quantitative easing, such as the 2013 JGB market sell-off.

“Confidence Erosion and Herding Behavior in Bond Markets: An Essay on Central Bank Communication Strategy”, Koichiro Kamada and Ko Miura

Bank of Japan Working Paper Series, No.14-E-6, April 2014

http://www.boj.or.jp/en/research/wps_rev/wps_2014/data/wp14e06.pdf

The below are excerpts from the paper. Emphasis and cursive text has been added.

The general idea

“When confidence is eroded, markets are driven by herding behavior among investors. Feeling that they lack sufficient information, investors pay more attention to other investors’ actions and try to pick up as much information as they can. Herding emerges from these rational actions of individual investors and amplifies price fluctuations in the market.”

The gist of the model

“This study develops a theoretical model and employs it for stochastic simulations to show that volatility of bond prices and trading volumes is affected by a number of factors, such as investors’ confidence in the financial environment, the usefulness or value of information available in the market, and the market liquidity of bonds.”

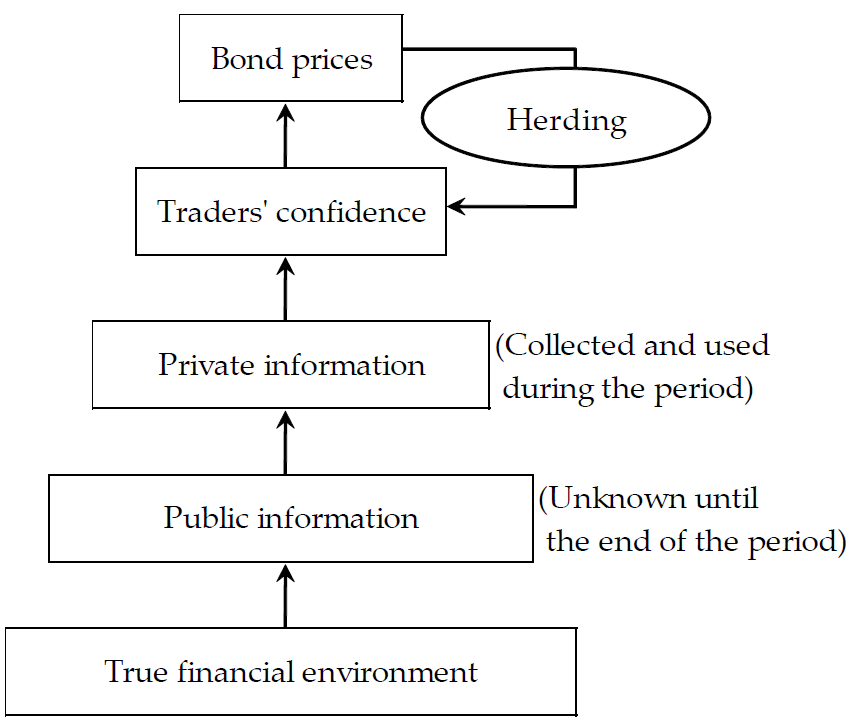

“[The basis of the analysis] Nirei’s model [of herding in financial markets] has two important ingredients: (i) investors obtain private information…before making investment decisions; (ii) they make inferences on other investors’ private information based on their observations of market conditions…”

“Traders face uncertainty about the financial environment…We assume that there are two states regarding the financial environment: state H is a low interest rate environment where bond prices are high; and state L is a high interest rate environment where bond prices are low. Traders do not know which state they find themselves in…but have an ex ante subjective probability distribution regarding the current environment. They believe that they are trading in state H with probability b and in state L with probability 1-b….special case where b=0.5, traders have no confidence.”

“In order to incorporate government bond markets into Nirei’s model [which only considers private information] we extend his model to deal with a double‐layered information structure consisting of both public and private information…By public information we mean all information that is related to interest rates and to which all traders have equal access…By private information we mean unpublicized information that each trader collects to predict public information.”

“Public information does not always convey correct information about the financial environment. We assume that public information is correct with probability q [>50%]. For instance, if the true financial environment is state H, public information indicates state H with probability q and state L with probability 1-q. We assume that q is common and known to all traders… we call q the value of information… q is a parameter measuring both the degree of certainty of public information and its relevance to interest rates.”

The main propositions of model analysis

“As traders’ confidence in the financial environment weakens [probabilities based on private information for state H and L converge to 50%], the volatility of bond prices increases… [Also,] the volatility of bond prices increases as the value of public information increases [simulated as probability that this information is correct and relevant increasing from 60% to 80%]. [High public information value] gives informed traders the opportunity to make large profits. However, at the same time, uninformed traders raise their ask prices and lower their bid prices in the hope of gaining from the price change. This reduces the opportunity for informed traders to make a profit and thus lowers transactions by them…there is also the well‐known rule of thumb among practitioners that interest rate volatility in the government bond market often increases when major statistics are released.”

“[As a direct effect] the volatility of bond prices declines when market liquidity increases. However, another force emerges that amplifies bond price volatility when market liquidity increases. Namely, as market liquidity increases, more favorable prices are offered to informed traders by uninformed traders; and thus more informed traders are attracted into the market to gain from bond transactions. Bond price volatility is determined by the balance of these two forces. Therefore, high market liquidity does not necessarily mean small volatility in bond prices.”

“When the accuracy of private information is high, its information value is also high. This prompts herding behavior among market participants and thus increases the volatility of bond prices and trading volumes… Simulated distributions…clearly show that the volatility of bond prices and trading volumes is greater when the standard deviation is smaller, i.e., the accuracy of private information increases.”

The 2013 JGB market sell-off

“On April 4, 2013, the Bank of Japan (BOJ) introduced quantitative and qualitative monetary easing (view post here). The policy had a substantial impact on bond markets.10‐year government bond yields rose rapidly from a low of 0.446 percent in April to a peak of 0.933 percent in May and continued to fluctuate throughout the summer.”

“We…fitted the model to actual interest rate data and showed that the model can explain, albeit quite roughly, the developments in long‐term interest rates around the time of the BOJ’s introduction of quantitative and qualitative easing. Furthermore, examining the fitness of the model, we find that the value of public information, including the central bank’s communication, plays an important role in explaining fluctuations of long‐term interest rates in 2013.”

“The key to understanding the developments in long‐term interest rates [in 2013] lies in how traders interpreted information flows in the market, especially the announcement by the Bank of Japan regarding its policy change, and in capturing the extent to which their confidence was weakened or strengthened by those information flows.”