A new CGFS study suggests that [i] bond market makers’ risk tolerance and warehousing have declined and [ii] tighter risk management has augmented pro-cyclicality of liquidity. A gap seems to have opened between more precarious liquidity supply and more voracious liquidity demand, due to rising assets under management at funds that allow daily redemptions.

Committee on the Global Financial System (2014), “Market-making and proprietary trading: industry trends, drivers and policy implications”, CGFS Papers No 52, Report submitted by a Study Group established by the Committee on the Global Financial System, November 2014

http://www.bis.org/publ/cgfs52.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

The basics of bond market making

“The vast majority of bonds are traded over the counter (OTC) rather than on the central limit order books of exchanges. The dominance of the OTC market structure reflects a number of bond market characteristics, such as: (i) the large number of issued bonds, which reduces the probability of finding matches in investor supply and demand for any given bond; (ii) the fixed maturity of bonds, allowing buy and hold investors to recoup their invested funds without trading in secondary markets, often resulting in ever fewer trades towards the bond’s date of maturity; and (iii) the prevalence of institutional investors who require execution of large-volume transactions that could potentially have a strong price impact when trading on a fully disclosed central limit order book. In the absence of continuous two-way markets for buyers and sellers, broker dealers, such as banks and securities trading firms, facilitate bond transactions.”

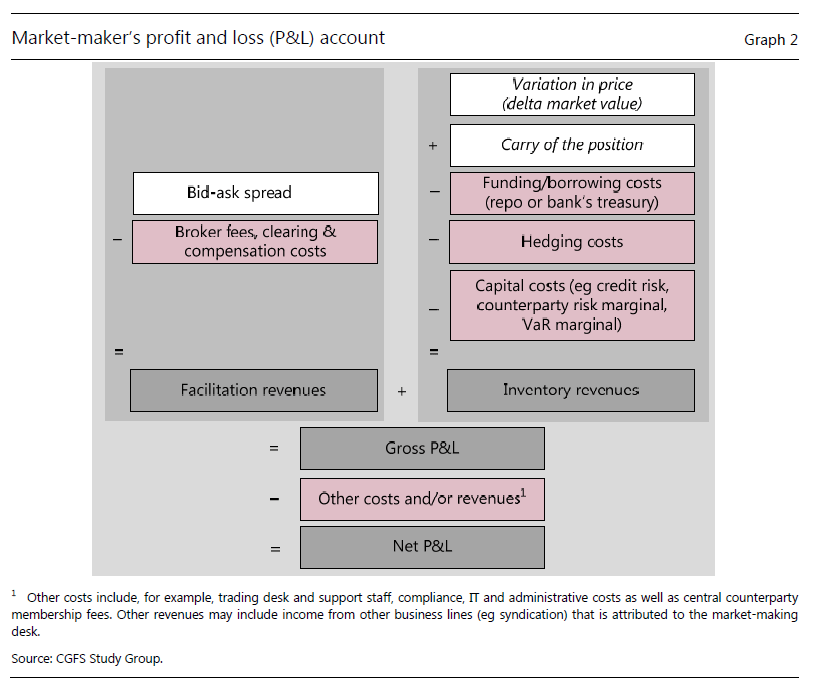

“A simplified market-maker’s profit and loss (P&L) account highlights…revenues and costs [graph below]. Two broad categories of (net) revenues can be defined: first, facilitation revenues, which reflect the realised spread on the bid and ask prices, net of the cost of trading. Second, unless trades can be immediately offset by opposing trades (i.e. the market-maker matches existing orders so that inventories remain unaffected) the P&L account is complemented by inventory revenues. These comprise changes in the value of the warehoused asset, carry of the position (e.g. accrued interest), the cost of funding as well as hedging costs. Regulatory requirements and similar constraints are another important factor.”

“Changes in the market environment and sentiment affect the provision of liquidity. Market-makers can respond to such changes by adjusting their bid-ask spreads, the quantities they are willing to trade at these prices, or their quoting behaviour. Rising market volatility, for example, can weigh on dealers’ willingness to hold inventory as the associated VaR rises and the cost of hedging exposures increases. Markets could then witness a widening of bid-ask spreads and a decline in quoted depth (i.e. the quantities that can be traded at the best bid and ask price), before market-makers eventually discontinue quoting on an ongoing basis and only passively respond to clients’ requests for quotes.”

The warehousing issue

“One apparent trend is market-makers’ increasing focus on activities requiring less capital and balance sheet capacity…Especially in Europe and the United States, many interviewees underscored the view that market-makers’ willingness to hold large inventory positions had decreased, particularly in less liquid instruments. Market-makers are reportedly focusing on activities that require less capital and balance sheet capacity, i.e. reducing the share of inventory revenues in their P&L accounts, and have been shifting towards more order-driven and/or brokerage models. As a result, the execution of large trades tends to require more time, at least in the less liquid markets.”

“Market participants from various jurisdictions underscore the decline in dealers’ risk tolerance as one major driver of the reduction in market making. Market-makers in many jurisdictions are thus raising the risk premia they demand, reassessing their risk management frameworks and developing more granular assessments of the value of trades, driving up the cost of taking risk.”

“In addition, some market-makers have adopted a more selective approach to offering client services, with the total cost and revenue of client relationships coming under increased scrutiny…Assessment of the value of trades has evolved.. Rather than return on risk-weighted assets (RWA) being reported at divisional levels, this measure is now calculated per trade per client (pre-execution) by some financial institutions. Funding and capital costs have thus become more important, with gross revenue only one factor in dealers’ overall assessment.”

The capital regulation issue

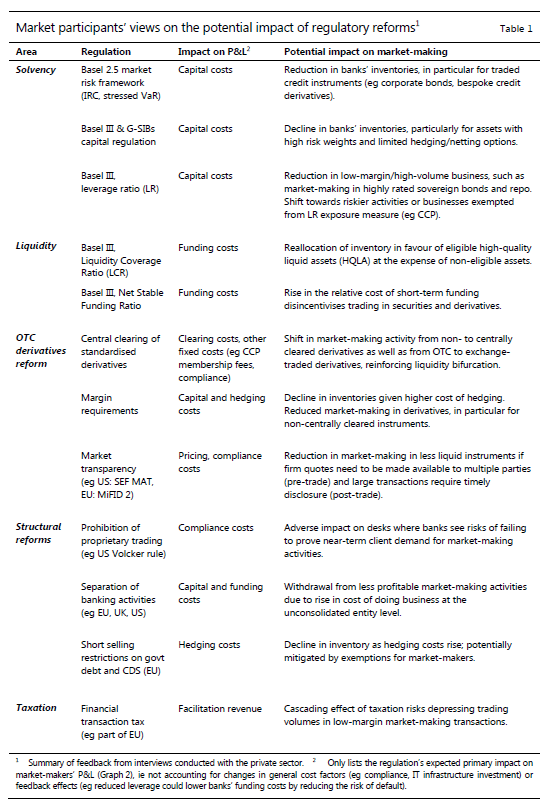

“The totality of current regulatory changes is likely to affect market-makers’ balance sheets and P&L accounts in a rather complex fashion…Many market participants expect the cost of market-making to rise, with less liquid assets, e.g. those with lumpy trading and/or less developed markets for hedging instruments… given the typical low-margin/highvolume nature of market-making, the leverage ratio tends to be seen by market participants as the most important possible constraint for market-makers in many jurisdictions and across fixed income instruments – both through its direct impact on capital allocations and inventory revenue as well as any impact on repo market activity and, hence, market-makers’ ability to manage inventory risk.”

“For corporate bonds, many market participants also point to increased regulatory capital charges adding to inventory costs (e.g. via the incremental risk capital charge and the stressed VaR requirements for the trading book introduced by the revisions to the Basel II market risk framework). The ineligibility of less liquid corporate bonds for the liquidity coverage ratio, in turn, is expected to further reduce the willingness of banks to warehouse these assets.”

On the key points of regulatory tightening view also post here.

The risk management issue

“Risk measures, such as VaR [Value-at-Risk], tend to mechanically rise with rising volatility, pushing estimated risks closer to any given VaR limits or other trading constraints. Dealer feedback indicates that risk measures have become more sensitive to changes in volatility because they now tend to give more weight to recent observations. Risk measures will thus rise more quickly when market volatility picks up, and market-makers may be forced to reduce their exposures more aggressively than in the past.”

“Since market liquidity, particularly during times of sizeable supply-demand imbalances, hinges on the willingness and ability of market-makers to take inventory risks, a marked decline in dealer risk tolerance could adversely affect financial market resilience.”

“One issue is that a larger share of liquidity risks has been shifted to investors, as market-makers appear less willing to take on these risks. This requires investors to adjust their risk management to adequately reflect higher liquidity risks. One particular challenge in this regard is to account for the dependence of liquidity on market conditions. Reaction functions that mechanistically apply risk limits and other thresholds, particularly if widely used by market participants, risk aggravating market liquidity conditions and setting off adverse feedback loops.”

On an example for VaR shocks view post here.

The proprietary trading issue

“PropRietary trading has reportedly diminished or assumed more marginal importance for banks in most jurisdictions, particularly in the euro area. Expectations are for banks’ proprietary trading to generally decline further or to be shifted to less regulated entities in response to regulatory reforms targeting these activities. This contrasts with trends in individual jurisdictions, particularly in Asia, that have been less affected by the recent crisis.”

“Market-makers are not the only market participants that contribute to market liquidity. Proprietary traders can, in principle, also contribute to absorbing temporary market imbalances and their activities are often closely tied to those of market-makers within the same institution.”

The liquidity demand issue

“Primary bond market expansion amid significant flows of funds to market participants that require immediacy services point to growing demand for market-making. There are also signs of increasing concentration among market participants that demand immediacy services, such as asset managers. As a result, market liquidity could become more dependent on the portfolio allocation decisions of only a few large institutions…Indeed, the total net bond holdings of the 20 largest asset managers alone increased by more than $4 trillion from 2008 to 2012, accounting for about 40% of their total net assets ($23.4 trillion). These managers accounted for more than 60% of the assets under management of the 300 largest firms in 2012, up from 50% in 2002.”

“Unprecedentedly low bond yields have incentivised risk-taking by some investors. Given the thin secondary market liquidity in most corporate bond markets, particularly for high-yield instruments, bond funds that promise daily liquidity on a best endeavours basis – such as the implicit expectation from investors that they can redeem from a mutual fund on a daily basis and sell exchange-traded funds (ETFs) at any point in time – have attracted significant inflows from both institutional and retail investors. In the United States, for example, mutual funds have raised their corporate and foreign bond holdings by nearly USD1.2 trillion since the beginning of 2008, while ETFs have accumulated an additional USD166 billion reflecting a more than tenfold increase in their holdings… Yet, given reduced immediacy provision by dealers, liquidating these assets could prove more difficult than expected when market sentiment deteriorates.”

“Diverging trends for market-making supply and demand generally imply upward pressure on trading costs, reduced market liquidity in secondary markets and, potentially, higher costs of financing in primary markets…Liquidity premia may have been compressed to artificially low levels in those bond markets where growth in demand has significantly outpaced net issuance over the past years, potentially masking the impact of reduced market-making supply.”