Chinese commodity financing deals exemplify how regulation and circumvention can distort more than one major market. These transactions have been a means for circumventing capital controls and facilitated short USD-CNY carry trades. Thereby they generated capital inflows into China, and distorted demand for physical metals (particularly copper) vis-a-vis futures. As China’s State Administration of Foreign Exchange (SAFE) has issued new regulation to curb these transactions, rapid unwinding might cause reverse distortions.

Copper curve ball – Chinese financing deals likely to end

Goldman Sachs Commodities Research, May 22, 2013

The basics

“The combination of Chinese capital controls and a significant positive domestic (CNY) to foreign (USD) interest rate differential has, in recent years, resulted in…large-scale ‘[commodity] financing deals’…These ‘financing deals’ typically use commodities with high value-to-density ratios such as gold, copper, nickel and ‘high-tech’ goods, as a tool to enable interest rate arbitrage. ”

A typical Chinese Copper Financing Deal (CCFD )involves 4 parties and 4 steps. [The parties are] (A) an offshore trading house, (B) an onshore trading house, (C) an offshore subsidiary of B, and (D) banks registered onshore serving B as a client.

- “[In step 1] offshore trader A sells warrant of bonded copper (copper in China’s bonded warehouse that is exempted from VAT payment before customs declaration) or inbound copper (i.e. copper on ship in transit to bonded) to onshore party B at price X…A is paid USD letter of credit, issued by onshore bank D.”

- “[In step 2] onshore entity B sells and re-exports the copper by sending the warrant documentation (not the physical copper which stays in bonded warehouse ‘offshore’) to the offshore subsidiary C. C pays B USD or CNH cash (CNH is offshore CNY). Using the cash from C, B gets bank D to convert the USD or CNH into onshore CNY.”

- “[In step 3] offshore subsidiary C sells the warrant back to A (again, no move in physical copper which stays in bonded warehouse ‘offshore’), and A pays C USD or CNH cash with a price of X minus USD10-20/t, i.e. a discount to the price sold by A to B in Step 1.”

- “[In step 4 the parties] repeat Step 1-Step 3 as many times as possible, during the period of the letter-of-credit (usually 6 months). This could be 10-30 times…with the limitation being the amount of time it takes to clear the paperwork. In this way, the total notional letter-of-credits issued over a particular tonne of bonded or inbound copper over the course of a year would be 10-30 times the value of the physical copper involved. “

“Through the whole process each tonne of copper involved in CCFDs is hedged by selling futures on LME futures curve (deals typically involve a long physical position and short futures position over the life of the CCFDs). Though typically owned and hedged by Party A, the hedger can be Party A, B, C and D, depending on the ownership of the copper warrant.”

The size at stake

“Chinese ‘financing deals’… likely…contribute to China’s FX inflows. For CCFDs, the immediate cross-border conversion of FX to onshore CNY after Party C pays Party B for the copper warrant (Step 2) directly contributes to China’s FX inflows. In terms of outflows, the issuance of letter-of-credit (FX short-term lending) by Party D to Party A (Step 1) is not associated FX outflow by definition, and when the letter-of-credits expire they tend to be rolled forward. Step 3 occurs offshore, so there is flow related to this transaction. In this way, the net Chinese FX inflows/outflows associated with CCFDs are equivalent to the change in the value of the notional letter-of-credits.”

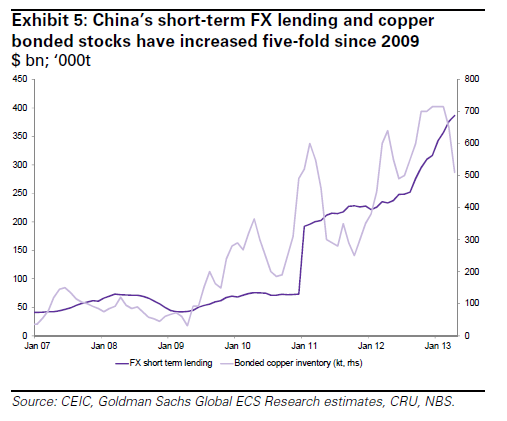

“Our best estimate suggests that roughly 10% of China’s short-term FX lending could have been associated with CCFDs since the beginning of 2012. In April 2013, we estimate that CCFDs accounted for USD35-40 bn of China’s total short-term FX lending. More broadly, Chinese bonded inventories and short-term FX lending has been positively correlated in recent years ”

Regulatory backlash

“With the notional value of ‘financing deals’ far exceeding the export/import value of the commodities used, and likely significantly contributing to the recent run-up in China’s short-term FX lending (and related upward pressure on the CNY), China’s State Administration of Foreign Exchange (SAFE) announced new regulations to address these issues (May 5), to be implemented in June…The new policies are in our view likely to bring to an end to these financing deals.”

“The new regulations can be split into two parts, and broadly summarised as follows:

The first measure targets Chinese bank balance sheets. This measure aims to

(i) directly reduce the scale of China’s FX loans, thus reducing the scale of letter of credit (letter-of-credit) financing (bank loans), thereby reducing the volume of funding available for…[commodity financing deals]… SAFE aims to implement a bank loan to bank deposit ratio of 75%-100% going forward, compared to an existing ratio of >150%

(ii) raise banks’ FX net open positions (banks are required to hold a minimum net long FX position at the expense of CNY liabilities), thus raising letter-of-credit financing costs, thereby increasing the cost of funding [of commodity financing deals].

The second measure targets…trade firms’ by identifying any activities that mainly result in FX inflows above normal export/import backed activities…This measure would force entities to curb their balance sheets if they are found to be involved in such activities.”

“A complete unwind of CCFDs would likely be bearish for copper prices as the copper used to unlock the interest rate differential shifts from being a positive return/carry asset to a negative carry asset.”