The rise in global temperatures calls for a lower-carbon economy overtime. This poses systemic financial risk in two ways. First, large fossil-fuel reserves may become unburnable, triggering a collapse in asset valuations and a rise in corporate and sovereign default risk. Second, ecological deterioration may trigger belated and sudden policy adjustments, forcing the financial system to confront large underestimated carbon risk exposure and an economic recession at the same time.

The below are excerpts from the paper. Headings, links and cursive text have been added.

Ecological imbalances

“The overuse of the environment as a sink for greenhouse-gas emissions and pollution and over-exploitation of water and raw materials have led to climate change, depletion of natural resources and loss of biodiversity. The development of these ecological imbalances is partly linear…but is partly also highly unpredictable, especially as imbalances become larger, with sudden tipping points and feedback loops after which recovery is no longer possible. A set of nine planetary boundaries has been identified within which there is a “safe operating space for humanity”. Three boundaries have already been passed (climate change, biodiversity and the nitrogen cycle) and two are coming close to being passed (ocean acidification and the phosphorus cycle).”

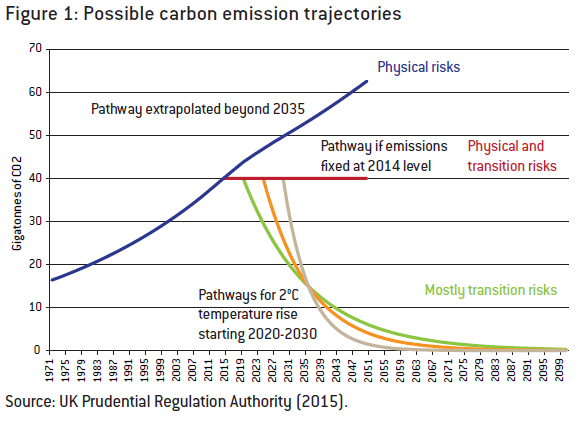

“In the Paris Agreement on climate change…countries reconfirmed the target of limiting the rise in global average temperatures relative to those in the pre-industrial world to two degrees Celsius…The speed with which the limit is reached depends on the emissions pathway. If current emissions are not drastically cut, the 2°C limit would be reached in less than two decades… There are many uncertainties about climate change.”

“Current market pricing might reflect both a lack of awareness of the challenges posed by climate change and uncertainty about the path of policy.”

The risk of a ‘carbon bubble’ burst

“One of the most studied risks to the financial system stemming from ecological imbalances is the so called ‘carbon bubble’ or the overvaluation of fossil-fuel reserves and related assets should the world manage to tackle global warming. Staying within a 2°C temperature rise puts a limit on future carbon emissions and hence on the amount of fossil fuels that can be burned, requiring a sharp bending of the current trend.”

“This could strand many existing fossil fuel reserves. Without carbon sequestration, McGlade and Ekins (2015) estimate that if global warming is to be kept below 2°C up to 2050, approximately 35 percent of known oil reserves, 52 percent of gas reserves and 88 percent of coal reserves are unburnable.”

“Private oil, gas and coal mining companies own about a quarter of fossil fuel reserves; sovereigns and their oil, gas and coal companies own the remainder. If a large part of these reserves cannot be extracted or extraction becomes commercially unviable, the valuation of these companies and their ability to repay their debt is reduced.”

“However, the effect of the bursting of the carbon bubble will not be limited to the oil, gas and coal sectors alone. A sudden transition will be a shock to all sectors that use fossil fuels as an input, either in the production or in the use of their products and services.”

The risk of a late-transition shock

“There is a risk of late…[transition to a low-carbon economy], resulting in a hard landing…The main risk is basically a policy risk that governments will suddenly take drastic actions. There is also a scenario of crossing the ecologic boundaries leading to floods and droughts due to climate change.”

“In the scenario of a late and sudden transition to a low-carbon economy, the financial sector can be heavily exposed to environmental risks… by its exposure to carbon-intensive real and financial assets. Moreover, reduced energy supply and increased energy costs would impair macroeconomic activity, as the hard landing forces a rapid transition away from fossil-fuel based energy production.”

“While a gradual transition would allow for a gradual write-down of long-lasting carbon-intensive infrastructures and assets, a rapid transition would force more radical write-downs because of the negligible scrap value of stranded assets and not fully anticipated losses.”