A Bank of England paper integrates commodity futures with bond yield curves. It finds that bond factors exert significant influence on commodities. It also finds that risk premia paid in crude oil futures have shifted over the decades from negative to positive, as crude’s hedge value faded with the memory of the oil crises. Gold futures have long paid a positive risk premium for lack of empirical hedge value.

Chin, Michael and Zhuoshi Liu (2015), “A joint affine model of commodity futures and US Treasury yields”, Bank of England, Working Paper No. 526

http://www.bankofengland.co.uk/research/Documents/workingpapers/2015/wp526.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

The term structure of commodity prices

“[Commodity futures price] models can be broadly defined as either structural models or reduced-form time series models. The structural models are usually based on theories…

- The theory of storage argues that the slope of the term structure of commodity futures prices is mainly determined by the level of commodity inventories. According to this theory, a downward sloping futures curve (i.e. a backwardated market) is an indication of tight inventories [and a high premium for immediate access to physical commodity], and an upward-sloping futures curve (i.e. a contango market) reflects a high level of inventories [and relatively low premium for immediate access to physical]… The convenience yield represents the net benefit associated with physical holdings of a given commodity, and if this yield is positive, it discounts the forward price relative to the current spot price. An example of this is where an oil refiner would prefer to hold oil physically than to wait for oil to be delivered in the future, because holding stocks of oil protects against increases in demand and the risk of shortages. If the benefits of owning physical oil exceed storage and financing costs, the forward price must be lower to encourage the refinery plant to enter into the contract.

- Hedging pressure theory, on the other hand, focuses on the determination of optimal hedging and speculative positions for hedgers and speculators within the futures market. The hypothesis predicts futures prices should be lower than the expected spot price (i.e. a positive risk premium) if hedgers [typically commercial producers and consumers] have net short positions within the market, and that futures prices should be higher than the expected spot price (i.e. a negative risk premium) if hedgers are net long…futures premia…[hence] reflect compensation to speculators for taking on residual risk from hedgers.”

“Reduced-form models focus on… the time series behaviour of commodity prices and their futures prices, and our models fall into this category… our model is based on a dynamic stochastic framework where no-arbitrage conditions are imposed.”

“Previous work has found that futures prices do not accurately predict future commodity prices…there are factors other than expectations… We can think of a futures price as being made up of two components, the expected future price and the risk premium. These components cannot be observed separately.”

The link with the term structure of bond yields

“Factors extracted from the US Treasury market play a significant role in the pricing of the commodity futures term structure, which is consistent with other empirical studies…We use a preliminary principal component analysis to identify the number of factors that explain the bond, oil and gold term structures.”

“We jointly model the US yield curve (i.e. the interest rates on US government bonds of different maturities), and the futures prices of two commodities: oil and gold,…Until recently, models of interest rate and commodity markets have mostly been developed in isolation, and this separation may have been increasingly unjustified over time, as over the past decade or so, financial institutions have become more involved in commodity markets while maintaining a significant presence in interest rate markets.”

Crude oil and gold futures risk premia

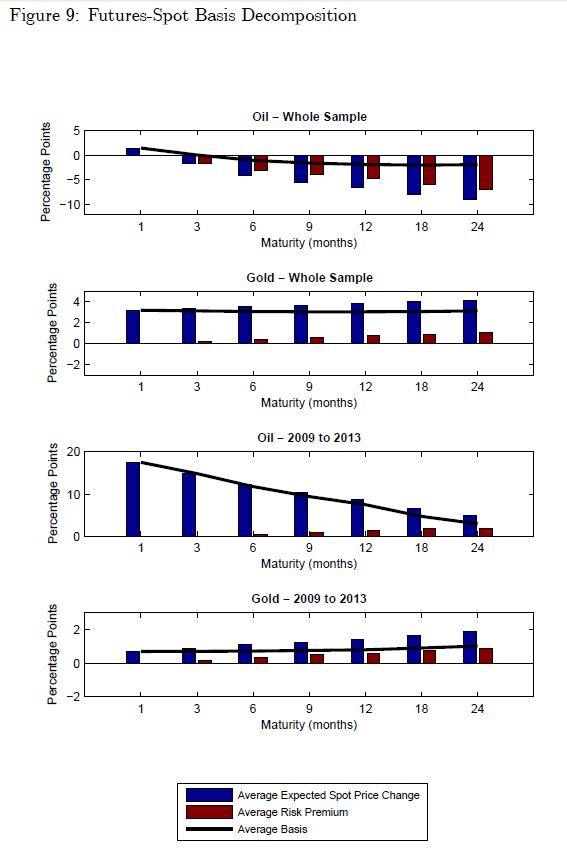

“We find that there is a significant difference between the risk premium in oil futures and the premium in gold futures. On average, the risk premium is negative for oil contracts, while it is positive for gold. Oil and gold have been perceived rather differently in financial markets.

- While the oil risk premium is negative over large parts of the period covered by our data, it follows an upward trend during the 2000s and recently turns positive. This behaviour could reflect the changing nature of the oil market over time, where the relative importance of demand and supply factors may have changed. In general, positive demand shocks are more likely to be associated with oil price increases, whereas negative supply shocks can imply oil price increases that put downward pressure on economic growth. To the extent that there have been large supply shocks in the oil market, an investor might actually have benefitted from holding oil, since the value of their holding would have increased in difficult times. Since investors prefer to hold assets that pay off in situations when their income is low (for example, a recession), they are willing to pay a premium for this type of asset, and this would imply a negative risk premium. Previous evidence suggests that supply influences on the price of oil were more important in the past, though have diminished over time, where demand shocks have been more prominent recently. This is consistent with the value of holdings co-varying positively with the economic cycle in more recent times.

- We estimate that the gold premium is mostly positive, indicating that in general investors require additional compensation for holding gold relative to US government bonds. This suggests that gold holdings are not perceived as providing better protection against economic downturns relative to US government bonds, where the value of gold generally falls in bad states of the world…The premium also appears to display counter-cyclical behavior, where the premium increases during recession periods.”

“The first two charts [in the figure below] show the decomposition of the futures basis into the expectation and risk premium components. The line and bars represent the average values over the whole sample of the futures basis, expected spot price changes and risk premia, respectively.”

“According to our estimates, the risk premium components of oil and gold futures prices can be relatively large. The importance of this component does appear to change over time. We find that risk premia vary depending on the level of economic activity and inflation.”

“We also find a significant relationship between risk premia and a measure of hedging pressure, suggesting that the balance of long and short hedging activity is also an important determinant of commodity futures premia.”