A very interesting Banca d’Italia study shows how euro area break-up expectations are becoming self-reinforcing, i.e. precipitating a divergence of sovereign yields and financial conditions beyond what is consistent with sovereign credit fundamentals.

http://www.bancaditalia.it/pubblicazioni/econo/quest_ecofin_2/qef128/QEF_128.pdf

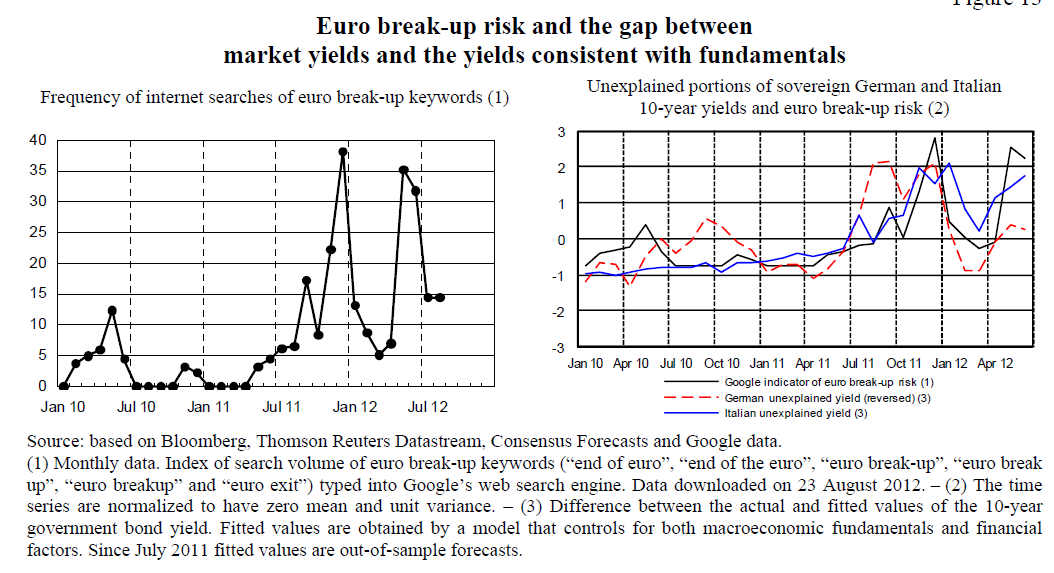

“Studies on the most recent period – i.e. since the onset of the Greek sovereign debt crisis at the end of 2009 – generally find that the surge in sovereign spreads experienced in several euro-area countries cannot be fully explained by changes in macroeconomic fundamentals. For Italian government bonds, most estimates of the 10-year spread fall around 200 basis points, as opposed to a market value of almost 450 points (at end-August 2012). Furthermore, large differences between the market spreads and those warranted by fundamentals are also found on shorter maturities.

- First, the fact that the deviation of sovereign yields from their model-based value is negative for some “core” countries and positive for “non-core” countries…

- Second, the divergence between sovereign spreads and their model-based values has emerged in a phase of exceptionally high volatility in financial markets, when the risk of a break-up of the euro is mentioned more and more frequently by market participants….

- [Third] there has been a growing divergence between Belgian rates and Italian and Spanish rates, with the former becoming closer to French and German rates. This suggests a clustering of interest rates along geo-economic patterns that were discernible before the introduction of the single currency and is consistent with a progressive loss of confidence in the integrity of the euro area.