The non-bank financial sector in the euro area has doubled in size over the last 10 years. It has become a concern for three reasons. First, its tight links with regulated banks imply contagion risk. Second, investment funds’ supply of liquidity has become critical for many markets, but is pro-cyclical. And third, rising synthetic leverage aggravates pro-cyclicality of both market prices and liquidity conditions.

European Central Bank (2015), “Financial Stability Review – Chapter 3: Euro area financial institutions”, May 2015.

http://www.ecb.europa.eu/pub/pdf/other/financialstabilityreview201505.en.pdf?9ef72154d2bddeb46bd7f3596b54c04d

On the basics of the function and systemic risks of shadow banking view the financial system summary page here.

The below are excerpts from the publication. Headings and cursive text have been added.

Size and expansion of euro area shadow banking

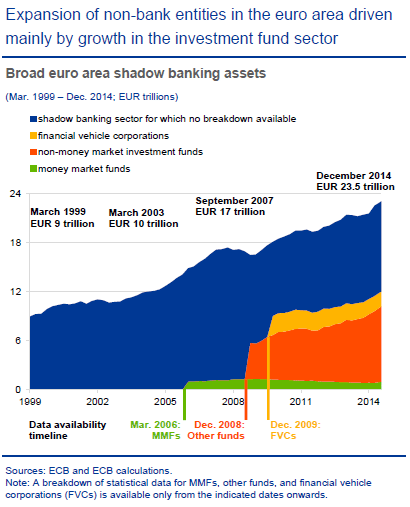

“The role of non-bank entities in credit intermediation…has strengthened amid historically low nominal rates and an ongoing search for yield. Using the broad definition of shadow banking by the Financial Stability Board, assets of non-bank financial entities in the euro area have more than doubled over the past decade, to reach EUR23.5 trillion [or over 210% of GDP] by December 2014. Since 2009, the shadow banking entities have increased their share in the total assets of the financial sector from 33% to 37%.”

The FSB estimates that worldwide shadow banking has reached about 120% of global GDP. For more details view post here.

“Growth of the non-bank financial sector has gathered pace again in recent years, following the global financial crisis and a shift to market-based funding. ..The rapid expansion of non-money market investment funds has been the main driver of growth…and accounts for a significant proportion of its assets. The sector has expanded by almost 30% since 2010, excluding valuation effects. Assets managed by investment funds…have increased by EUR4.0 trillion (74%) over the past five years…to reach EUR9.4 trillion in the fourth quarter of 2014…At the same time, money market funds and financial vehicle corporations have declined in volume terms.”

“The growing role of non-bank entities in the financial sector there implies that the systemic relevance of these entities is increasing.”

The contagion issue

“Concerns relate to investment funds’ increasing role in credit intermediation and capital markets, and the implications for the wider financial system and the real economy…Since almost all large asset management companies in the euro area are owned by banks or bank holding companies, reputational problems in the asset management arm could spill over to the parent company.”

“Possible channels of risk contagion and amplification include correlated asset exposures, as well as mutual contractual obligations in derivatives markets, and securities lending and financing transactions…euro area non-bank entities are important providers of bank funding and hold roughly 10% of bank debt securities. Conversely, euro area banks’ direct exposures to non-bank entities amount to 8% of the aggregate balance sheet of MFIs. In addition, banks can provide liquidity backstops, indemnification or credit lines to non-banks in times of stress.”

On the risk of shadow banking contagion to regulated banks also view posts here and here.

The liquidity issue

“There is a growing concern about the potentially destabilising role of non-bank entities in sharp price adjustments in asset markets…Vulnerabilities result from liquidity transformation and the pro-cyclical provision of liquidity to financial markets.”

“The bond fund sector is large in size (EUR3 trillion), holds a significant proportion of illiquid assets and plays an important role as provider of marginal liquidity in secondary bond markets. Smaller in size, real estate funds likewise engage in liquidity transformation with a focus on investment in assets that are highly illiquid. The hedge fund sector…within and outside the euro area are important providers of market liquidity, especially in the less liquid asset markets.”

“Investment funds hold a relevant and growing proportion of the debt securities of euro area banks, governments and non-financial corporates. In the less liquid non-financial corporate markets, more than 25% of debt securities outstanding are now held by investment funds, a share that has increased significantly not only over the last few years, but also in the recent past. In the much larger markets for government and bank debt securities, investment funds still hold relevant shares of 12% and 9% respectively. Any large-scale portfolio rebalancing among investment funds could therefore result in significant swings in asset prices and market liquidity.”

“Investment funds could consume, rather than provide, liquidity under stressed conditions…In the past, substantial outflows could be observed, in particular after major market events and sustained periods of stress. Following debt sustainability concerns in the euro area in August 2011, for instance, funds experienced comparably large outflows that amounted to more than 15% of the total assets for European high-yield institutional funds.”

“Any future large-scale fund outflows could be aggravated by strategic complementarities among funds’ investors that result from first-mover advantages. Run-like risks arise from the issuance of callable equity used to fund relatively illiquid portfolios. Investment funds that invest in thinly traded assets face higher asset liquidation costs, but may also find it much harder to price their shares efficiently.”

On the pro-cyclical momentum of redemptions and herding in mutual funds view post here.

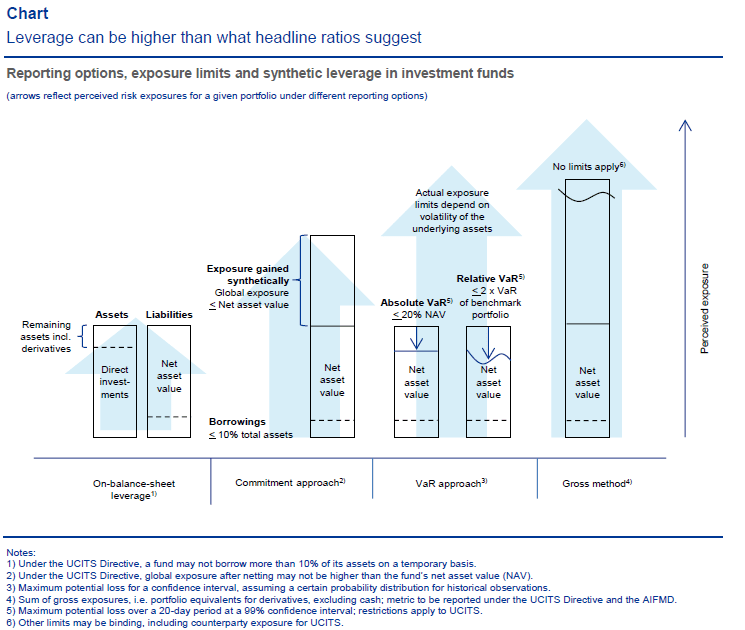

The “synthetic leverage” issue

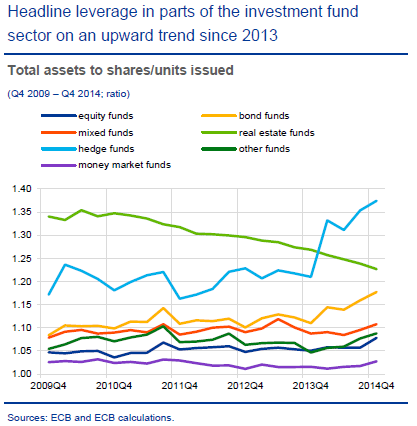

“Since average leverage ratios of investment funds are more than ten times smaller than those of banks, solvency risks seem to be limited – even when considering the more highly leveraged real estate and hedge funds… Banks are funded mainly by callable debt, i.e. deposits and notes, in addition to longer-dated liabilities, while investment funds issue predominantly callable equity. Therefore, balance sheet leverage ratios are relatively low for investment funds.”

“However, leverage differs greatly among the various entities and there may be pockets of high leverage in parts of the investment fund sector where it is potentially destabilising, but masked by the aggregate figures. For instance, some hedge fund strategies are known to involve high leverage, such as relative-value and global macro strategies.”

“Data from the ECB’s investment fund statistics show that balance sheet leverage has been on an upward trend since 2013, in particular in the case of hedge funds and bond funds… Further data suggest that the use of derivatives is especially high and growing not only among hedge funds, but also among bond funds in comparison with other types of investment funds.”

“Swaps, futures and other derivatives allow investment funds to gain exposures to asset classes even without having them fully funded. In addition to balance sheet leverage, contingent commitments from such transactions create “synthetic leverage”… Such “synthetic leverage” can stem from derivative instruments or securities financing transactions that create exposures contingent on the future value of an underlying asset, which becomes evident, for instance, when a derivative position’s value moves strongly.

“Although the UCITS Directive [EU rules of “Undertakings for Collective Investment in Transferable Securities”] regulates leverage, it is possible under the current regulatory framework to gain exposures synthetically. Depending on the metric used, such exposures can imply higher leverage than suggested by headline ratios… Synthetic leverage can add to liquidity spirals, especially in times of distress, due to the high volatility of synthetically created exposures and the pro-cyclical nature of margining requirements associated with them.”