The systemic importance of commodity trading firms (CTFs) deserves attention. Key points to understand are [i] CTFs’ core business is logistics, storage and processing, [ii] they are exposed to basis risk rather than outright price risk, [iii] their profitability depends on volumes and derivatives markets liquidity, [iv] they perform little traditional bank-style term transformation, but [v] they are financial intermediaries, by offering funding and structured product services.

Pirrong, Craig (2014), “The Economics of Commodity Trading Firms”, White paper by Trafigura

http://www.trafigura.com/site-information/corporate-brochure/trafigura-whitepaper/

The below are excerpts from the paper. Contents has been re-arranged to focus on aspects that are critical for financial market participants. Emphasis and cursive text has been added.

The essential functions of CTFs are logistics, storage and processing

“Commodity trading firms are all essentially in the business of transforming commodities in space (logistics), in time (storage), and in form (processing). Their basic function is to perform physical ‘arbitrages’ which enhance value through these various transformations.”

“The primary role of commodity trading firms is to identify and optimize those transformations. An important determinant of the optimization process is the cost of making the transformations. These costs include transportation costs (for making spatial transformations), storage costs (including the cost of financing inventory), and processing/refining costs. These costs depend, in part, on [physical and regulatory] constraints [and] bottlenecks in the transformation processes. All else equal, the tighter the constraints affecting a particular transformation process, the more expensive that transformation is.”

“Commodity traders characterize their role as finding and exploiting ‘arbitrages’. An arbitrage is said to exist when the value of a transformation, as indicated by the difference between the prices of the transformed and untransformed commodity, exceeds the cost of making the transformation… Consider a spatial transformation in grain. A firm can buy corn in Iowa for $5.00/bushel (bu) and finds a buyer in Taiwan willing to pay $6.25/bu. Making this transaction requires a trader to pay for elevations to load the corn on a barge, and from a barge to an oceangoing ship; to pay barge and ocean freight; to finance the cargo during its time in transit; and to insure the cargo against loss. The trader determines that these costs total $1.15/bu, leaving a margin of $0.10/bu. If this is sufficient to compensate for the risks and administrative costs incidental to the trade, the trader will make it.”

CTFs typically take ‘basis risk’ or ‘spread risk’ rather than price risk

“This description of a typical commodity trade illustrates that the commodity traders are primarily concerned with price differentials, rather than the absolute level of commodity prices… price levels affect the profitability of commodity trading primarily through their effect on the cost of financing transactions, and their association with the volume of transactions that are undertaken.”

“Most commodity trading firms do not speculate on movements in the levels of commodity prices. Instead, as a rule they hedge these ‘flat price’ risks, and bear risks related to price differences and spreads—basis risks [i.e. the differential between the price of a physical commodity and its hedging instrument.]… The basis is less volatile than the flat price, but there is still a risk of large losses… CTFs accept and manage basis risk in financial markets.”

“From time to time commodity trading firms engage in other kinds of ‘spread’ transactions that expose them to risk of loss. A common trade is a calendar (or time) spread trade in which the same commodity is bought and sold simultaneously, for different delivery dates. Many commodity hedges involve a mismatch in timing that gives rise to spread risk. For instance, a firm may hedge inventory of corn in October using a futures contract that expires in December.”

CTFs’ profitability depends on volumes, margins and derivatives market liquidity

“The profitability of traditional commodity merchandising depends primarily on margins between purchase and sale prices, and the volume of transactions. These variables tend to be positively correlated: margins tend to be high when volumes are high, because both are increasing in the (derived) demand for the transformation services that commodity merchants provide… This means that variations in the quantity of commodity shipments, as opposed to variations in commodity flat prices, are better measures of the riskiness of traditional commodity merchandising operations.”

“CTFs have various kinds of liquidity risk…

- Market liquidity… As frequent traders, commodity trading firms are highly sensitive to variations in market liquidity.… Commodity trading (including specifically hedging) frequently requires firms to enter and exit positions quickly… Liquidity can vary across commodities; e.g., oil derivative markets are substantially more liquid than coal or power derivatives markets… Liquidity can decline precipitously, particularly during stressed market periods. Since market stresses can also necessitate firms to change positions (e.g., to sell off inventory and liquidate the associated hedges), firms can suffer large losses in attempting to implement these changes when markets are illiquid and hence their purchases tend to drive prices up and their sales tend to drive prices down.

- Funding liquidity…Traditional commodity merchandising is highly dependent on access to financing. Many transformations (e.g., shipping a cargo of oil on a very large cruise carrier) are heavily leveraged (often 100%) against the security of the value of the commodity. A commodity trading firm deprived of the ability to finance the acquisition of commodities to transport, store, or process cannot continue to operate… Stressed conditions in financial markets typically result in declines of both market liquidity and funding liquidity. Relatedly, stresses in funding markets are often associated with large price movements that lead to greater variation margin payments that increase financing needs.

- Hedging liquidity. CTFs use futures exchanges to hedge commodities. Loss-making hedges incur costs daily before offsetting profits on physical commodities are realized.”

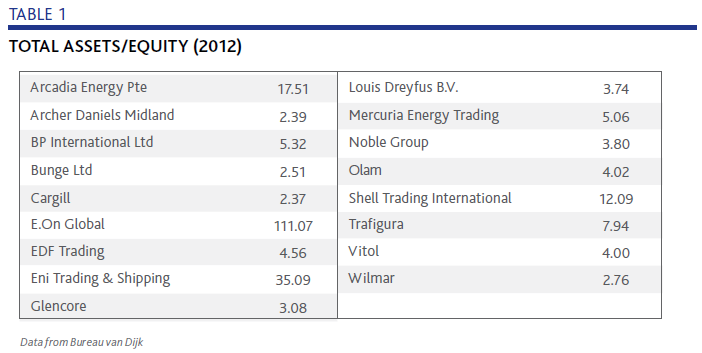

CTFs are less leveraged than banks and perform little maturity transformation

“Leverage for the largest, most asset-heavy CTFs is similar to non-financial US corporations. Other CTFs are more highly leveraged but much less leveraged than banks… One measure of total leverage is total assets divided by book value of equity. [The table below]…presents this measure for 2012 for 18 trading firms for which data are available. This ratio ranges from 2.38 (ADM) to 111 (E.On Global). The average [massively distorted by E.On] is 18, and the median is 4…The ratio of assets to equity for [U.S. non-financial] corporations was 2.06… for US banks that have been designated Systemically Important Financial Institutions (“SIFIs”), the mean leverage is 10.4″

“CTFs’ balance sheets are structured differently from banks. In general, short-term assets are funded with short-term debt and long-term assets with long-term funding.”

“In the past decade, some commodity trading firms have also arranged non-traditional short-term financings that could be characterized as ‘shadow bank’ transactions. These include the securitization of inventories and receivables, and inventory repurchase transactions….[However] these structures do not generally exhibit the maturity mismatches that contributed to runs on the liabilities of some securitization vehicles during the financial crisis… These non-bank financing vehicles may become increasingly important because broader financial trends may constrain the availability of, and raise the cost of, traditional sources of transactional financing.”

CTFs function as financial intermediaries

“CTFs also act as financial intermediaries for their customers through complex transactions that bundle financing, risk management and marketing services. Common structures include trade credit agreements, pre-financing, commodity prepays, and tolling arrangements [agreement with an owner of a commodity to process it for a specified fee]. Banks and other financial institutions remain, overwhelmingly, the ultimate source of credit. CTFs act as conduits between these financial institutions and their customers.”

“Commodity trading firms provide various forms of financing and risk management services to their customers. Sometimes commodity marketing, financing, and risk management services are bundled in structured transactions with commodity trading firms’ customers.”

“Many banks have (or had) commodity trading operations. Prominent examples include J. Aron (part of Goldman Sachs since 1981), Phibro (once part of Citigroup and before that Salomon Brothers, though it is now not affiliated with a bank), and the commodity trading divisions of Morgan Stanley, J. P. Morgan Chase, and Barclays.”