In its October 2012 World Economic Outlook the IMF presented a 135-year study on public debt reduction strategies. It points out that debt stocks of over 100% of GDP have not been uncommon and do not normally lead to restructuring. Indeed, in the developed world out of 26 episodes only 3 ended in default (Germany and Greece). Successful debt-reduction strategies typically use growth-enhancing and easy monetary policies.

The Good, the Bad, and the Ugly: 100 Years of Dealing with Public Debt Overhangs

IMF World Economic Outlook October 2012

IMF World Economic Outlook October 2012

http://www.imf.org/external/pubs/ft/weo/2012/02/pdf/c3.pdf

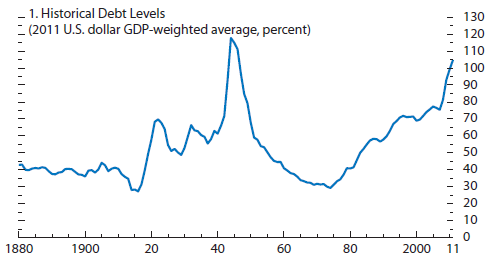

“Public debt in advanced economies has climbed to its highest level since World War II. In Japan, the United States, and several European countries, it now exceeds 100% of GDP. Low growth, persistent budget deficits, and high future and contingent liabilities stemming from population-aging-related spending pressure and weak financial sectors have markedly heightened concerns about the sustainability of public finances.

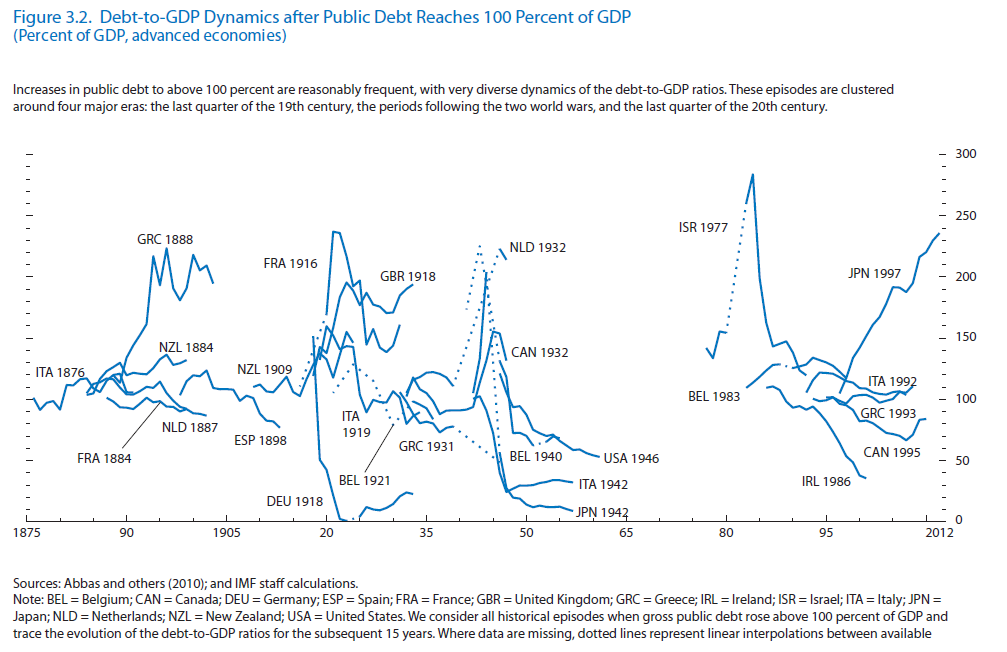

The IMF reviewed a database for “advanced” economies since 1875 to study 26 identified episodes of excess debt, specifically the evolution of the debt-to- GDP ratio for 15 years after the 100% threshold was crossed. A basic line chart (see below) conveys three key insights:

-

Public debt levels above 100% of GDP are not uncommon. Of the 22 advanced economies for which there is good data coverage, more than half experienced at least one high-debt episode between 1875 and 1997. Furthermore, several countries had multiple episodes: three for Belgium and Italy and two for Canada, France, Greece, the Netherlands, and New Zealand.

-

The dynamics of the debt-to-GDP ratios [after they reached 100% of GDP] are quite diverse, with some countries experiencing additional large increases and others witnessing sharp reductions.

-

The episodes are clustered around four major eras: the last quarter of the 19th century, the periods following the two world wars, and the last quarter of the 20th century. The 19th century debt build-up was related mainly to nation building and the railroad boom. The post–World War II episodes are connected with the enormous and widespread military effort and subsequent rebuilding, although some start earlier, during the Great Depression. The episodes in the last cluster during the 1980s and 1990s have their genesis in the breakdown of the Bretton Woods system, when government policy struggled with social issues and the transition to current economic systems.

Among the 26 episodes, only 3 feature default: Germany (1918), which suspended war reparations in 1932, and Greece (1888, 1931), which defaulted in 1894 and 1932, respectively. These episodes have little relevance for the challenges faced by advanced economies today for at least two reasons. First, they involve very peculiar features that set them apart from others: the post–World War I political instability in Germany, the nation-building effort of Greece at the turn of the 19th century and the subsequent Greco-Turkish war of 1897, and a period of deep internal political instability in Greece after the 1919–22 war with Turkey. Second, in these defaults a large proportion of public debt was denominated in foreign currency (or gold), which made debt repayment subject to exchange rate fluctuations.

After reaching 100% of GDP, the debt-to-GDP ratio tends to decline, even though at a very moderate pace. This tendency to reverse is not present at lower levels of debt, for example when debt rises above 60% of GDP.

The relationship between inflation and debt reduction is…ambiguous. Although hyperinflation is clearly associated with sharp debt reduction, when hyperinflation episodes are excluded, there is no clear association between the average inflation rate and the change in debt. Finally, a relatively stronger growth performance is associated with debt reduction when hyperinflation episodes are excluded.

For countries currently struggling with high public debt burdens, the historical record offers important lessons.

- The first lesson is that fiscal consolidation efforts need to be complemented by measures that support growth: structural issues need to be addressed and monetary conditions need to be as supportive as possible. In Japan, for example, weaknesses in the banking system and corporate sector limited monetary policy efficacy and led to weak growth, which prevented fiscal consolidation.

- The case of the United Kingdom (from 1918-1933) offers a cautionary lesson for countries attempting internal devaluation. The combination of tight monetary and tight fiscal policy, aimed at significantly reducing the price level and returning to the pre-war parity, had disastrous outcomes. Unemployment was high, growth was low, and— most relevant—debt continued to grow.

- Consolidation plans should emphasize persistent, structural reforms over temporary or short-lived measures. Belgium (from 1983-98) and Canada (1995-2010) were ultimately much more successful than Italy in reducing debt, and a key difference between these cases is the relative weight placed on structural improvements versus temporary efforts. Moreover, both Belgium and Canada put in place fiscal frameworks in the 1990s that preserved the improvement in the fiscal balance and mitigated consolidation fatigue.