A new BIS paper provides evidence that since 2013 fluctuations in EM fund flows and EM bond prices have reinforced each other. Both redemptions and discretionary sales of fund managers have been pro-cyclical. In liquidity-constrained markets this behavior is prone to transmitting shocks and amplifying crises.

Shek, Jimmy, Ilhyock Shim and Hyun Song Shin (2015), “Investor redemptions and fund manager sales of emerging market bonds: how are they related?”, BIS Working Papers No 509, August 2015

http://www.bis.org/publ/work509.htm

The below are excerpts from the paper. Headings, cursive text and references to other posts have been added.

On EM bond funds

“The prolonged period of low global long-term interest rates has resulted in a shift in the pattern of financial intermediation as global banks have increasingly given way to long-term investors in the market for debt securities. The transmission of financial conditions across borders has taken the form of ‘reaching for yield’, declining risk premiums for debt securities and increased issuance of emerging market economy (EME) bonds.”

On the secular rise of asset management and its increased systemic relevance also view post here.

“The assets under management of dedicated EME bond funds have grown strongly over the past decade and stood at USD1.3 trillion at the end of 2014…Open-end funds allow investors to add or redeem investments. Exchange-traded funds (ETFs) are a form of open-end fund that is traded on exchanges. Closed-end funds, when set up, issue a fixed number of shares that are traded on secondary markets. Open-end mutual funds are much larger than closed-end funds and ETFs in terms of both the number of funds and the total amount of AUM… Around 98% (74%) of EME bonds (equities) managed by collective investment vehicles have mandates to follow an active investment strategy.”

Dedicated EM exposure has surged by over 55% from 2007 to 2014, with assets concentrated on few managers. View post here on how trading flows are correlated due to the widespread use of benchmarks. Also view post here on how foreign participation made local EM debt markets more vulnerable to global interest rate and risk shocks.

On redemptions

“Investor flows into collective investment vehicles such as mutual funds, hedge funds and private equity funds…tend to be positively correlated with fund performance [according to] a growing literature that examines the pro-cyclical investment behaviour of institutional investors. The Bank of England’s Pro-cyclicality Working Group (2014) defines pro-cyclicality as investing in a way that exacerbates market movements and contributes to asset price volatility or investing in a way that exaggerates the peaks and troughs of asset price or economic cycles.”

The last IMF Financial Stability Report also highlighted the motivation of end investors and fund managers to rush sales in distress, due to first-mover advantages and herding incentives (view post here).

Pro-cyclicality does not mean that either returns or flows are the original shock that triggered the market move. It only means that returns and flows reinforce each other and lead to market overreaction to fundamental shocks (view post here).

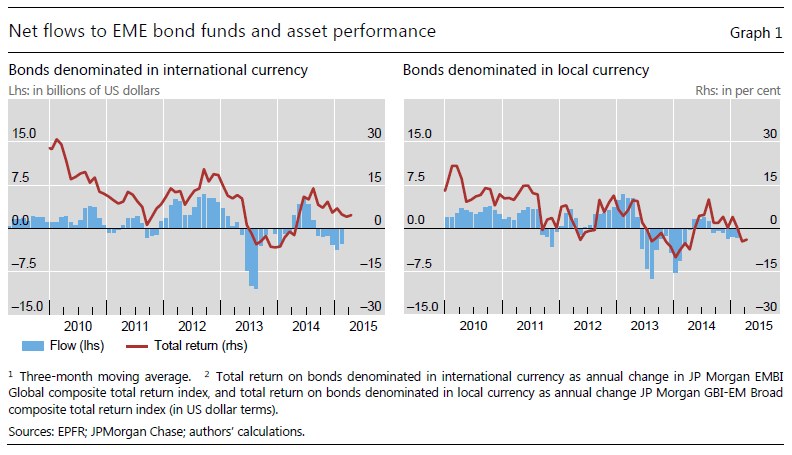

“We…examine in greater detail investor net flows in a sample consisting of 368 global EME bond funds for which weekly data on investor flows are available from the EPFR database for all 113 weeks from January 2013 to February 2015…We provide evidence that a large share of EME bond funds have often experienced sizeable redemptions, especially during the period of EME bond market turbulence, and that EME bond funds faced more severe redemption shocks than AE bond funds.”

“[The graph below] illustrates the positive co-movement between net flows to and returns on EME bond funds in the EPFR database.”

“The share of institutional investor funds facing sizeable outflows is smaller than that for retail investor funds both on average over the whole sample period and during severe outflow episodes…For advanced economies bond funds…redemptions are less severe than for EME bond funds, although the patterns are similar to those of the EME bond funds.”

On fund managers’ response

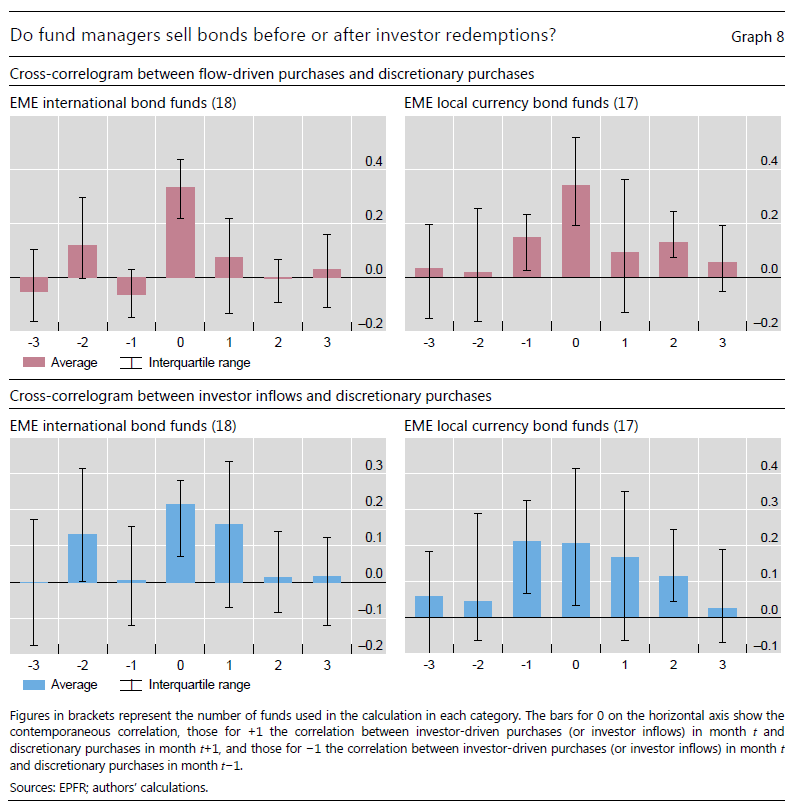

“Bond sales may result either from the sales needed to meet investor redemptions or from discretionary sales beyond that implied by investor redemptions.”

“Discretionary sales by fund managers tend to reinforce the sales driven by redemptions by ultimate investors… we find positive contemporaneous correlations between flow-driven purchases and discretionary purchases and also between investor inflows and discretionary purchases for both EME international bond funds and EME local currency bond funds…The magnitudes are…economically significant. One hundred dollars’ worth of bond sales due to investor redemptions is accompanied by roughly 10 dollars’ worth of discretionary bond sales.”

“Discretionary sales reflect the hoarding of cash by asset managers during periods of market turbulence. Gauging their quantitative significance is an important precondition for an overall judgment on the marketwide liquidity impact of one-sided markets and fire sales…The co-movement of redemptions and discretionary sales reflects the hoarding of cash by fund managers in the face of greater anticipated redemptions amid unsettled market conditions.”

On the systemic consequences

“Thus, rather than cushioning the selling pressure on EME bonds during a redemption spree, there appears to be an additional significant impetus to the selling pressure due to fund managers’ discretionary sales.”

“The hoarding of cash might reflect efforts by the asset managers to maintain what they see as a prudent level of cash holdings in the face of market volatility and investor redemptions. However, what is prudent from the point of view of an individual asset manager may nevertheless give rise to concerted selling episodes that exacerbate one-sided markets and add to spillover effects on broader financial conditions.”

A specific feature of local EM bond markets is limited liquidity. Outflows and fear of escalation often cause ‘proxy hedging’ through FX forward market (view post here). However, the resulting depreciation and volatility of local EM currencies itself then raises FX risk of local market investments and can trigger yet more outflows (view post here).

“The collective action problem associated with the hoarding of cash has a parallel in the systemic consequences of deleveraging by banks and other financial intermediaries. The leverage of banks and other financial intermediaries tends to be pro-cyclical, rising during booms and falling in busts…In the same vein, cash hoarding by asset managers may generate fire-sale externalities that exacerbate market liquidity conditions. This is so even if asset managers employ little leverage. The channel of spillovers is through shifts in the composition of assets, rather than deleveraging.”

“[Other research papers] show that neither fund managers nor investors are contrarian, especially during crises, and that their behaviour seems to amplify crises and transmit shocks…[Other papers] identify run-like incentives… created by the first-mover advantage and short-term liquidity concerns, and in turn draw parallels with the global game literature on bank runs. Indeed, the less liquid the underlying assets are, the greater are the spillover effects of investor redemptions to remaining investors, thereby exacerbating the selling pressures in a run-like episode.”