Empirical evidence suggests that investors pay less attention to macroeconomic news when market sentiment is positive. Market responses to economic data surprises have historically been muted in high sentiment periods. Behavioral research supports the idea that investors prefer heuristic decision-making and neglect fundamental information in bullish markets, but pay more attention in turbulent times. This allows prices to diverge temporarily from fundamentals and undermines the conventional risk-return trade-off when sentiment is high. Low-risk portfolios tend to outperform subsequently. The sentiment bias also means that fundamental predictors of market prices work better in low-sentiment periods than in high-sentiment periods.

The below are quotes of the above paper and some other sources which are linked next to the quote. Emphasis, headings, and text in brackets have been added for clarity.

This post ties in with this site’s summary on macro information inefficiency.

Sentiment and inattention

“Investors need to take into account the effect of investor sentiment when trading on macroeconomic news…[Positive] sentiment seems to hinder the incorporation of public information into asset prices.”

“Investor sentiment can undermine the incorporation of macroeconomic fundamental information into stock prices around macroeconomic announcements…We provide evidence that the stock market response to macroeconomic news weakens in times of high investor sentiment. The reaction to macroeconomic information is 50 percent weaker in times of elevated bullish investor sentiment… The results hold for both good and bad macroeconomic news and remain robust when using alternative investor sentiment measures.”

“In periods of high… sentiment, investors’ reliance on heuristic processing of information is likely to increase and so investors are less sensitive to fundamental information. On the other hand, when sentiment is not high, investors are more likely to process information systematically and become more sensitive to news. This intuition is in line with the findings from psychology and financial literature. Psychologists have shown that emotions affect decision making and information processing, and individuals engage in more heuristic rather than systematic processing of information when facing positive emotions.”

Consequences of sentiment-based inattention

“In finance, recent [academic] articles have shown that investor sentiment undermines the relation between asset prices and their fundamental value…Sentiment-induced trading drives asset prices away from fundamentals and discourages rational arbitrageurs from betting against mispricing.”

“Sentiment undermines the traditional risk-return trade-off and distorts the link between economic variables and the equity premium… the predictability of the equity premium depends more on nonfundamental variables when sentiment is high. When sentiment is low, the connection between fundamentals and the equity premium is stronger.”

“We discover a striking two-regime pattern for…macro-related factors: high-risk portfolios earn significantly higher returns than low-risk portfolios following low-sentiment periods, whereas the exact opposite occurs following high-sentiment periods…sentiment-driven investors undermine the traditional risk-return trade-off, especially during high-sentiment periods.” [Shen, Yu, and Zhao, 2017]

“Our findings suggest that the economic variables do have strong predicting power as long as the market sentiment is not too high to distort the fundamental link between economic variables and equity premium too much…fundamental predictors are preferable to non-fundamental variables in periods of low sentiment while high sentiment periods largely favour non-fundamental predictor. Our findings are broadly consistent with the implications of the theories of sentiment.” [Chu, Li, He, and Tu, 2018]

“Stock portfolios with higher sensitivity to a set of macro-related risk factors earn lower returns in times of high sentiment. Their results indicate that macro-related risk factors are priced differently during times of high vs. low investor sentiment.”

“[Academic research] finds a stronger sensitivity of the stock market to macroeconomic news in times of high ambiguity. “

“Investors treat bad news as more relevant in bad times than in good times but treat good news the same in good and bad times.” [Zhou, 2015]

Measuring sentiment

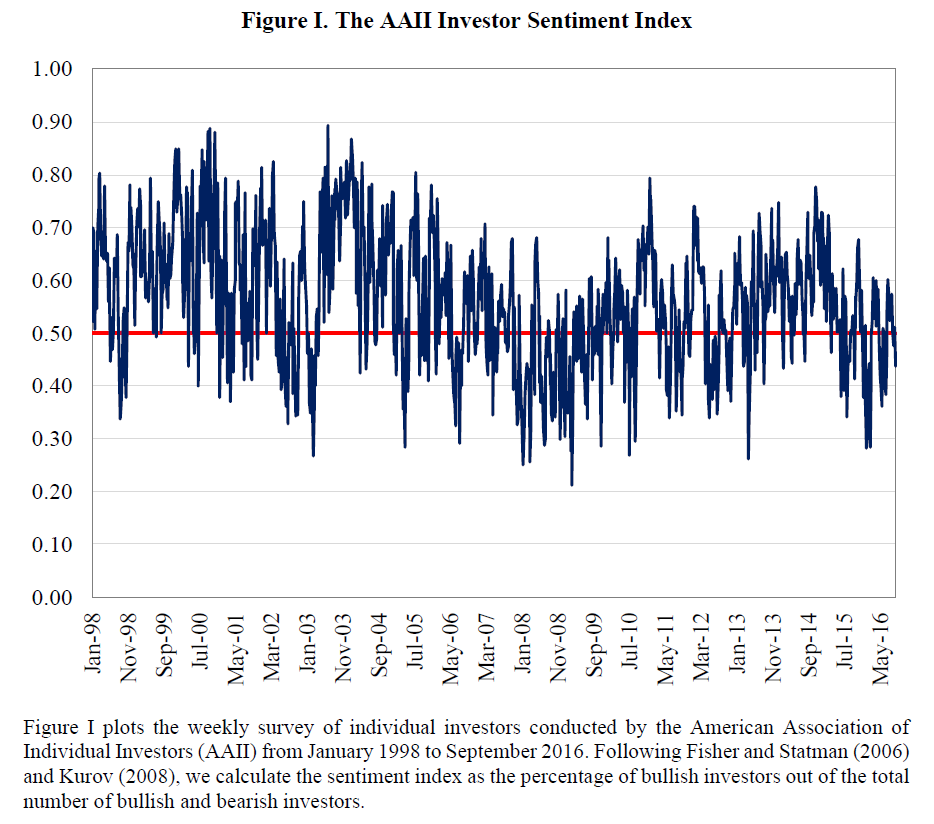

“We investigate the role of investor sentiment in the stock market response to macroeconomic news. We measure sentiment based on the weekly reports of the American Association of Individual Investors (AAII)… Each week, AAII asks its members the following question: ‘Do you feel that the direction of the stock market over the next six months will be up (bullish), no change (neutral), or down (bearish)?’ The survey is open to all AAII members…We compute the AAII sentiment as the ratio of the number of bullish investors to the total number of bullish and bearish investors.”

“[The figure below] plots the AAII sentiment measure over our sample period. Investor sentiment does fluctuate significantly over time, reaching a maximum value of about 0.9 and a minimum value of about 0.2.”

“We re-run our analysis using three other measures of sentiment…the Baker-Wurgler investor sentiment, the University of Michigan consumer sentiment, and the SENTIX individual investor sentiment…The results are consistent with those based on the AAII sentiment.”

Measuring macro news

“We focus on a specific type of information, the information incorporated in scheduled U.S. macroeconomic news, and examine whether investor sentiment affects the stock market response to such news…Macroeconomic news is a fundamental indicator of the ongoing economic environment. Financial markets are expected to respond to such news, especially when the actual numbers released are not in line with the expected values.”

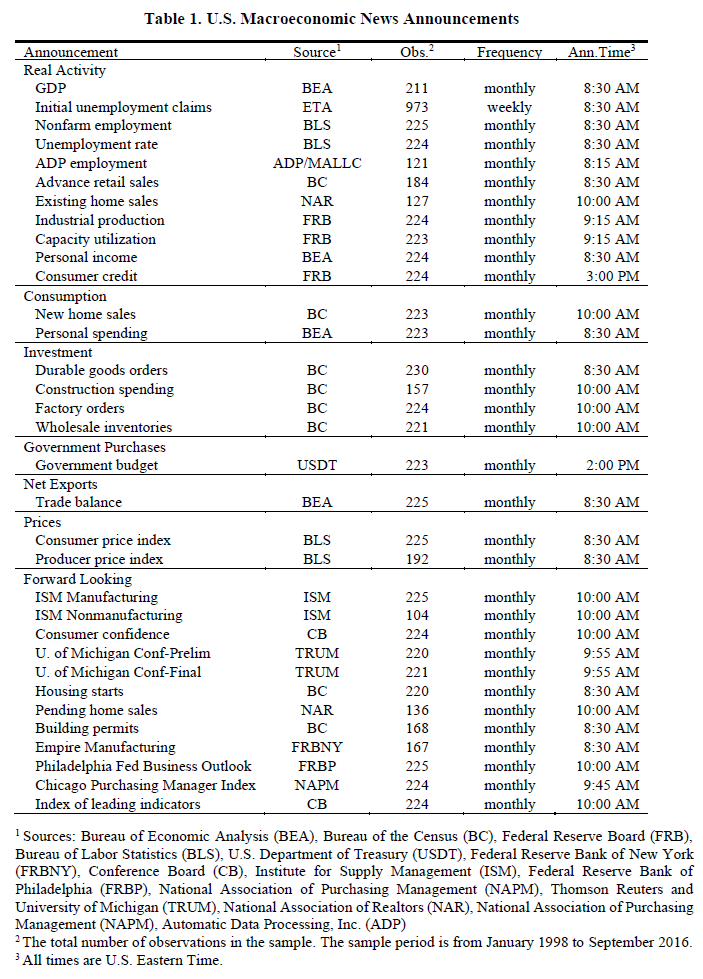

“[The below table] reports the basic description of the macroeconomic announcements.”

“We first examine whether the stock market reacts to 33 important U.S. macroeconomic announcements. For each announcement, we calculate the announcement surprise as the difference between the actual and the expected value of the released macroeconomic indicator… We compute the news surprises as the difference between the actual released value and the expected value of a macroeconomic indicator. Then, we standardize the surprises [by] the sample standard deviation of [the difference between] the announced value of macroeconomic indicator [and] the expected median value of the Bloomberg forecast.”

“Most of the macroeconomic announcements have significant effects on the aggregate stock market return…For instance, the stock market increases significantly when the actual GDP growth is greater than the pre-announcement consensus. Higher than expected GDP growth indicates that the overall economy is performing well, which is good news for stocks. The results also show that the market responds negatively to unemployment rate surprises…All the announcements in the ‘real activity’ category, with the exception of ‘Capacity Utilization’ and ‘Personal Income’, have a significant impact on the stock market. Moreover, positive surprises for ‘New Home Sales’, ‘Personal Spending’, ‘Durable Goods Orders’, ‘Factory Orders’, and ‘Trade Balance’ are good news for the stock market. However, for CPI and PPI, the two announcements under the category ‘Price’, positive surprises are bad news for stocks.”

The empirical evidence

“Our results show that a high bullish investor sentiment undermines the stock market reaction to macroeconomic news. These findings hold in an aggregate macroeconomic specification that treats all announcements the same, and also in an individual analysis that distinguishes among announcement types.

“The effect investor sentiment has on the stock market response to macroeconomic news is economically significant. Based on the aggregate macroeconomic specification, one standard deviation increase in [sentiment] leads to about 50 percent decrease in the stock market response to macroeconomic announcements…One standard deviation increase in sentiment leads to a 37 percent decrease in the stock market response to ‘Initial Unemployment Claims’ and a 51.6 percent decrease in the market response to ‘Nonfarm Employment’. Our findings are also robust. The dampening effect sentiment has on the stock market reaction to macroeconomic shocks holds for both good and bad macroeconomic news.”