The IMF Financial Stability Report highlights two systemic weaknesses of plain-vanilla mutual funds: incentives for end investors to rush for the exit in distress and incentives for portfolio managers to herd. With deteriorating market liquidity and greater systemic importance of collateral values, these weaknesses become a greater concern for the global financial system.

IMF Global Financial Stability Report (2015), Chapter 3, “The Asset Management Industry and Financial Stability”, April 2015 http://www.imf.org/External/Pubs/FT/GFSR/2015/01/pdf/c3.pdf

On the global expansion and general systemic risks of asset management view post here.

On the potential destabilizing effects of real money funds on bonds markets view post here.

On the key allocation decisions of U.S. mutual funds and their drivers view post here.

The below are excerpts from the GFSR. Emphasis and cursive text have been added.

Size and systemic importance of asset management

“In recent years, credit intermediation has been shifting from the banking to the nonbank sector, including the asset management industry. Tighter regulations on banks, rising compliance costs, and continued bank balance sheet deleveraging following the global financial crisis have contributed to this shift.”

“Globally, the [asset management industry] industry now intermediates assets amounting to USD76 trillion (100% of world GDP and 40% of global financial assets… By now, the assets under management of top asset management companies are as large as those of the largest banks, and they show similar levels of concentration.”

“Banks are predominantly financed with short-term debt, exposing them to both solvency and liquidity risks. In contrast, most investment funds issue shares, and end investors bear all investment risk. High leverage is mostly limited to hedge funds and private equity funds, which represent a small share of the industry. Therefore, solvency risk is low.”

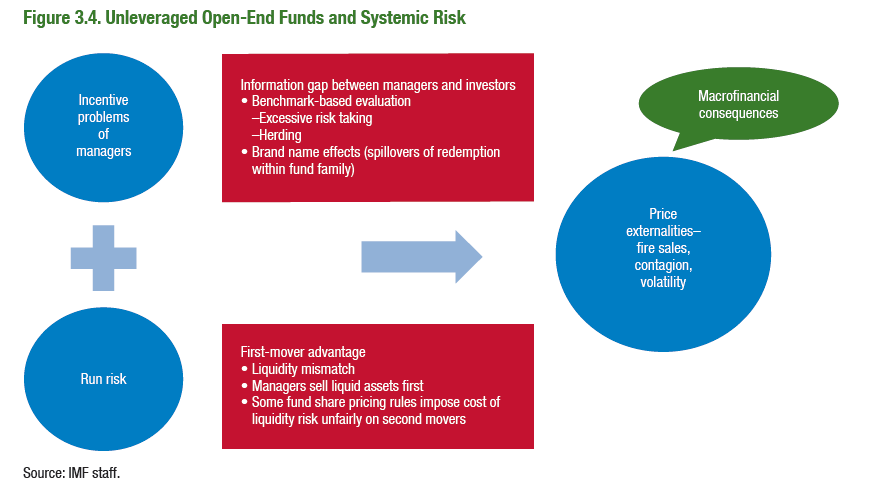

“Even…plain-vanilla funds [mutual funds and ETFs] can pose financial stability risks. ..Two main risk channels…are important…[i] a first-mover advantage for end investors (that is, incentives not to be the last in the queue if others are redeeming from a fund), which may result in fire-sale dynamics…[ii] incentive problems related to the delegation of portfolio management decisions by end investors to funds, which, among other things, may lead to herding.“

The first-mover incentives for end investors

“Open-end funds are exposed to redemption risk because investors have the ability to redeem their shares (usually on a daily basis) while funds have increasingly been investing in relatively illiquid securities such as high-yield corporate bonds and emerging market assets.”

“Generally, asset managers choose cash buffers and fee policies to limit liquidity risks, though competitive pressures have been reducing the use of redemption fees…Easy redemption options can create run risks due to a first-mover advantage. Investors can have an incentive to exit faster than the others…if the liquidation values of fund shares declines as investors wait longer to exit. This decline in value could happen for various reasons. First, asset managers may use cash buffers and sell relatively more liquid assets first in the face of large redemptions. Second, certain funds have fund share pricing rules that pass the costs of selling assets—possibly at fire sale prices—on to the remaining investors.

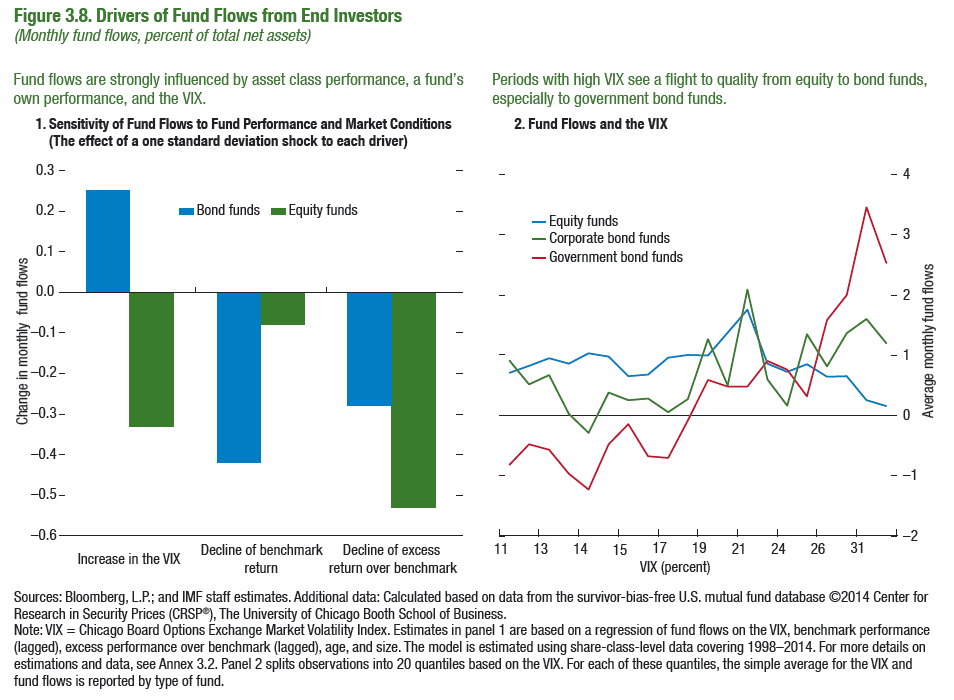

“End investors’ flows to funds, especially those from retail investors, are pro-cyclical… Fund flows increase after good market performance of the respective asset class. This indicates that investors pursue momentum strategies, increasing their allocation to asset classes that have performed well in the past, and selling past losers. End investors engage in a flight to quality during episodes of stress. “

“In the United States, funds issuing redeemable securities are required to sell, redeem, or repurchase such securities based on the NAV of the security ‘next computed’ after receipt of the order. Transaction costs—trading fees, market impact, and spread costs—are borne by the funds. This reduces a fund’s NAV, possibly by a substantial amount if market liquidity dries up.”

“The [empirical] analysis finds evidence consistent with the notion that mutual fund investments affect asset price dynamics, at least in less liquid markets… Surprise outflows are associated with lower same week asset returns in emerging markets, and to a lesser extent in U.S. high-yield bond and municipal bond markets. The annualized price impact is not negligible: bond returns rise by about 5 percentage points when aggregate fund inflows are higher than the top 25th percentile, and fall by a similar magnitude for outflows exceeding the top 25th percentile across bond categories. In emerging markets, and also in the U.S. municipal bond market, the negative price effects from sell-offs tend to be larger than the positive price effects from purchases. The price impact of surprise flows is significantly larger when global risk aversion (as measured by…VIX) is high.”

The herding incentives for portfolio managers

“A common way of providing incentives is to evaluate asset managers relative to their peers and to benchmarks. This evaluation can take direct or indirect forms: (1) managers’ compensation can be linked to relative performance or (2) investors inject money into funds that perform well relative to their benchmarks. [These incentives]… can lead to a variety of dynamics with potentially systemic implications…

- Evaluation relative to average performance tends to induce risk-averse portfolio managers to mimic the behavior of peers…Incentives to herd are reinforced because end investors can exit funds quickly, and mutual fund managers cannot afford to wait until their peers’ private information is revealed and incorporated fully in asset prices…When fund managers lose AUM because of poor performance, ‘‘flights to quality’’ may occur.

- If fund managers become more risk averse in response to past losses, and if they are evaluated against their peers or benchmarks, they may be induced to retrench to the benchmark in response to losses.”

- “Relative performance is a main driver of fund inflows. Investors disproportionately pour money into funds with strong recent performance, creating an incentive for managers of poorly performing funds to increase risks. Funds with excess returns over their benchmark receive disproportionately more inflows…Investors inject money into winning funds to a greater extent than they punish poor performers, implying a convexity in the performance-inflow relationship.”

“Empirical evidence of mutual fund herding is abundant… Herding among U.S. mutual funds is on the rise across fund styles. This finding is true for both U.S. equities and corporate bonds in recent years. For U.S. equities, mutual funds appear to co-move more during distress episodes. Retail-oriented funds show consistently higher levels of herding than do institutional oriented funds.”

For an explanation of herding and its causes view posts here and here.

On empirical evidence for herding view post here.

How weaknesses translate into systemic risks

“Although these risks are not fundamentally new, their relevance has risen with structural changes in the financial sectors of advanced economies. The relative importance of the asset management industry has grown, and banks have also retrenched from many market-making activities, contributing to a reduction in market liquidity. Moreover, the role of fixed-income funds, which entail larger contagion risks than traditional equity investment, has expanded considerably. A broader range of products are available to less sophisticated investors. Last, the prolonged period of low interest rates in advanced economies has resulted in a search for yield, which has led funds to invest in less liquid assets.”

“If intermediation through funds raises the probability of fire sales of bonds that are held by key players in the financial sector or that are used as collateral, then the risk of destabilizing knock-on effects on other institutions rises, with potentially important macro-financial consequences. Similarly, if funds exacerbate the volatility of capital flows in and out of emerging markets or increase the likelihood of contagion, significant consequences will be endured by the recipient economies.”