,Yuan,Banknotes,At,A")

According to Nomura’s Zhiwei Zhang and Wendy Chen, “China is displaying the same three symptoms that Japan, the US and parts of Europe all showed before suffering financial crises: a rapid build-up of leverage, elevated property prices and a decline in potential growth…the most vulnerable areas are local government financing vehicles, property developers, trust companies and credit guarantee companies.”

China: Rising risks of financial crisis Nomura Asia Special Report 15 March 2013

Rapid build-up of leverage

“Empirically, the build-up of leverage has been identified as a simple but tried and tested leading indicator for financial crises in academic research…”

“Leverage in China‟s economy, as measured by the domestic credit-to-GDP ratio has reached its highest level since data was made available in 1978…as the government implemented proactive fiscal and monetary policies to support growth and relied on bank loans to finance the fiscal expansion….The domestic credit-to-GDP ratio, rose quickly from 121% of GDP in 2008 to 155% in 2012. Looking at China’s history over the last 30 years, there was a similar build-up of leverage in the 1990s which made the whole banking sector insolvent….International comparison also suggests the build-up of leverage since 2008 is dangerous. We notice an interesting common phenomenon which we call the ‘5-30 rule’, where financial crises in large economies are usually preceded by the leverage ratio rising sharply by 30% of GDP in the five years before the crisis is triggered.”

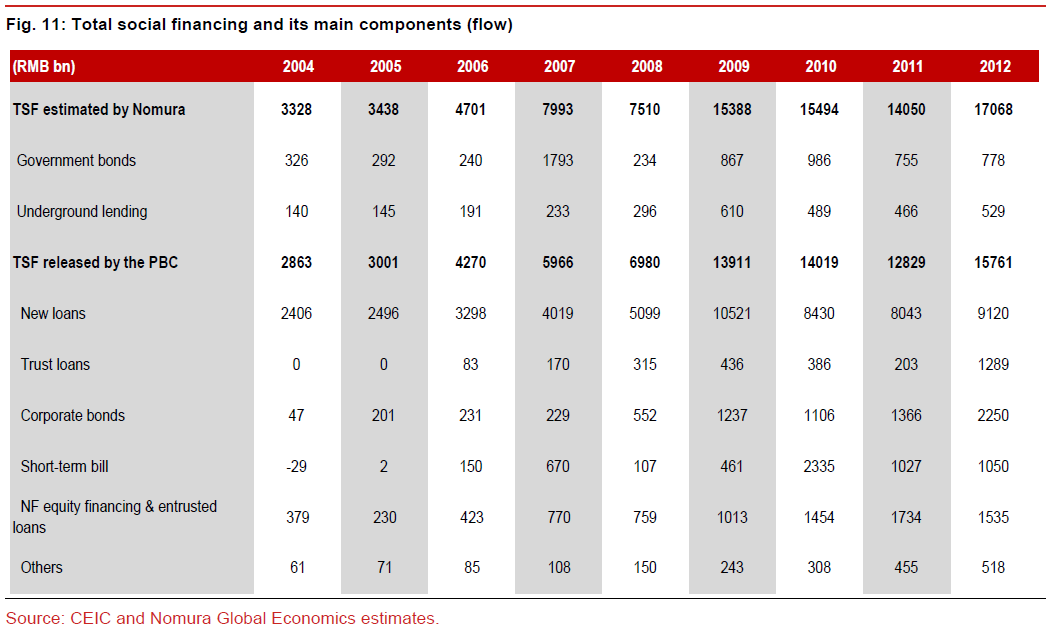

“The domestic credit-to-GDP ratio only captures credit provided by the official banking system and does not include credit supplied through the bond and equity markets, or the shadow banking system. In April 2011, the PBoC began to publish a ‘total social financing’ statistic, which attempts to measure overall credit supply to the economy…The main components are:”

- “Bank loans: Standard loans made by banks, which fall into the loan quota set by regulators. This has been the …dominant force in credit supply…largely driven by lending to local government financing vehicles.

- Trust loans: This refers to loans arranged by trust companies, which are non-bank financial institutions. They raise funds from retail and institutional investors before channeling them into specific projects. They are not constrained by bank loan quotas set by the regulators.

- Entrusted loans: These refer to lending from one company to another through the banks. Direct lending from one corporate to another is illegal in China, so cross-firm lending goes through the banking system.

- Corporate bonds: The amount of issuance has risen sharply in recent years… This is partly driven by deregulation of the bond market as regulators intentionally loosened control to foster the market’s development.

- Banker acceptance bills: These are a promised future payment issued by firms that are accepted and guaranteed by commercial banks. After acceptance, the bill becomes an unconditional liability of the bank, but the holder can sell it…Banker acceptances are frequently used in money market funds.”

“The other channel is underground lending, which is reportedly active in some regions such as Wenzhou and Erdos…the PBoC conducted a survey in mid-2011 and concluded that the stock was RMB3.38trn, equivalent to 5.8% of total bank loans.”

“Our estimate shows the stock of total ‘total social financing’ has risen by 62% of GDP to 207% in 2012 from 145% in 2008. The build-up of leverage is faster than that suggested by the official ‘total social financing’ -to- GDP ratio which shows a 58%-of-GDP increase from 129% to 187%, much faster than the domestic credit-to-GDP ratio, which rose 32% of GDP to 153% from 121% over the same period.”

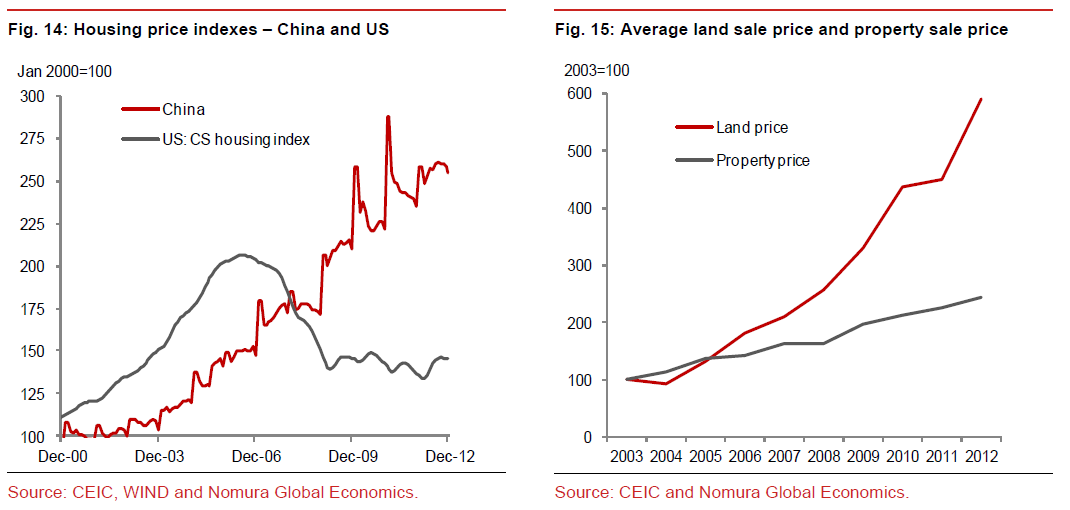

“Property sector conditions seem rather benign, with prices rising by only a very moderate, cumulative 113% over the period 2004 to 2012 in major Chinese cities…[However] a recent academic paper provided a hedonic [quality-adjusted] index for 25 major cities. According to three professors in Tsinghua University and National University of Singapore (Wu, Deng and Liu, 2013), property prices rose by 250% from 2004 to 2009, far outstripping the level of growth in the official index. By comparison, it also rose faster than the Case-Shiller US housing price index, which climbed by 84% from 2001 to its peak in 2006.”

“Furthermore, land prices rose even more sharply than property prices. According to official statistics, the average price per square meter of land at sale was just RMB573 in 2003 (USD69.2 on the 2003 exchange rate), rising to RMB3,393 in 2012 (USD537) – a 492% rise over 10 years.”

Decline of potential growth

“The demand-supply ratio in the urban labor market is arguably the best indicator of wider labor market conditions in China. The ratio was persistently below 1 before 2009, suggesting the labor market was over-supplied, mostly due to the large influx of migrant workers from inland rural areas. But in 2009 the trend reversed. The ratio climbed above 1 in Q4 2009 and remained there for 12 consecutive quarters. Even when GDP growth slowed to 7.4% in Q3 2012, the ratio remained above 1, which suggests to us that the potential growth rate has likely slowed to 7.0-7.5%.”

The vulnerability of major economic sectors.

“The main risks lie mostly in three areas: local governments, property developers and non-bank financial institutions.”

- “While the overall public sector does not have a solvency problem, local governments are facing tough challenges… Most local government investment is not yet profitable, because of the large share that has gone into infrastructure projects, such as the building of subways and highways, which require substantial investment upfront but take many years to break even. Indeed, financial statements disclosed by most LGFVs [local government funding vehicles] who sought capital from the bond market show negative cash flows. Tianjing Urban Construction Company, the largest LGFV in the country, reported that its cash flow in 2011 fell to -RMB31bn from -RMB7bn in 2010… Many LGFVs have managed to stay solvent because local governments provided new capital, subsidies and guarantees to allow them to issue new debt. New capital is often in the form of land, the value of which is subject to substantial market risks… When land sales failed to provide the required incremental growth in funding for LGFVs in 2012, they turned to “urban construction” bonds and infrastructure trust products… It is not clear to us how the LGFVs will be able to finance their growing investments in 2013 and beyond. We estimate the current outstanding debt of LGFVs at around RMB11trn. Assuming 10% of the principle becomes due in 2012 and an interest rate of 6%, the LGFVs would need RMB1.76trn just to repay existing debt – more than the total amount of urban construction bonds issued in 2012.

- Bank weakness comes from three main sources. The first is loan exposure to LGFVs, which reached RMB9.25trn as of September 2012, which accounted for 14.1% of total outstanding bank loans… The second source is exposure to property developers. The size of loans made to property developers has been constrained by regulators, but at end-2012 stood at RMB3.9trn, or 6.2% of total loans outstanding… A far more problematic and less transparent risk stems from so-called wealth-management products (WMPs) that banks sell to retail investors. According to the CBRC, the amount of WMPs outstanding soared to RMB7.1trn by end-2012, equivalent to 7.4% of bank deposits.

- The trust companies quickly became the second-largest group of non-bank financial institutions in terms of assets under management (AUM) (Figure 39). In 2008, AUM for the sector was only RMB1.2trn, smaller than the insurance sector (RMB3.3trn) and mutual funds (RMB2.6trn). By 2012, this AUM had rocketed to RMB7trn, exceeding both the insurance (RMB6.9trn) and mutual fund (RMB2.9trn) sectors… There have been five boom-and-bust cycles in the trust sector since 1980. Each time the boom was associated with an economic upturn and the bust amplified the deleveraging process and damaged the economy.”