A new IMF paper shows empirically that official currency interventions affect external imbalances and, by implication, exchange rate misalignments. There is a short-term flow impact, which is strongest when capital mobility is low. And there is a medium-term portfolio balance impact, which is strongest when capital mobility is high. Both effects are intuitive and offer lessons for FX trading strategies.

Bayoumi, Tamim, Joseph Gagnon, and Christian Saborowski (2014), “Official Financial Flows, Capital Mobility, and Global Imbalances”, IMF Working Paper 14/199, October 2014.

http://www.imf.org/external/pubs/ft/wp/2014/wp14199.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

The empirical analysis

“We use a cross-country panel approach to analyze the effect of net official flows on current accounts. The sample runs up to 26 years, from 1986 through 2011 although the baseline sample is de-facto restricted to the period of 1995–2010.”

“We define official financial flows as the acquisition and disposition of assets and liabilities denominated in foreign currencies by public-sector institutions in the reporting country. The dominant form of official flows is purchases of foreign exchange reserves. However, public-sector borrowing in foreign currency…[and] foreign asset purchases by sovereign wealth funds (SWFs) also count as official financial flows.”

The short-term flow effect of interventions

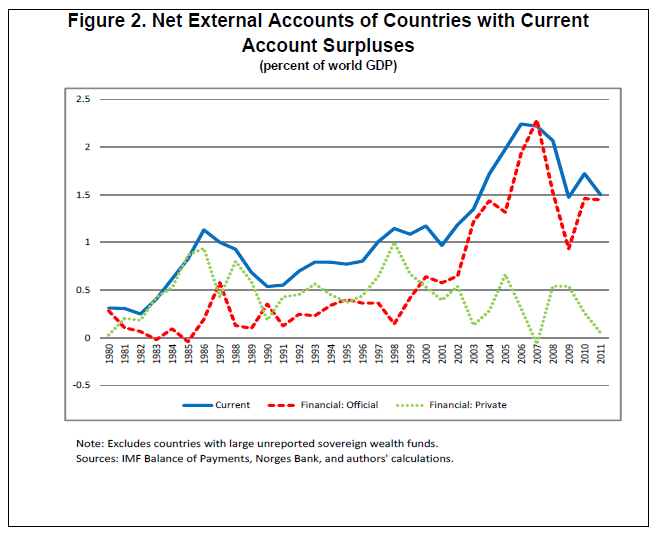

“We find that net official flows have a large but plausible effect on current account balances…[The figure below shows that ] the rise in current account imbalances since 2000 is clearly associated with an increase in net official flows of a strikingly similar magnitude, whereas net private flows declined slightly and appear unrelated to the combined current account surplus.”

“The estimated effect of net official flows on the current account when capital mobility is below the median is 0.66 [to] 0.71 in column [suggesting that USD1 intervention is associated with a USD0.66-0.71 change in the external balance]. The overall effect of net official flows when mobility is above the median is…0.11 [to] 0.03.”

“The impact of net official flows is importantly affected by the extent of international capital mobility… [Theoretically] there is a one-to-one relationship between net official flows and the current account when private financial markets are closed. And, in the opposite extreme of efficient financial markets with perfect capital mobility, sterilized official flows [under the uncovered interest rate parity] have no effect on the current account because they are fully offset by private flows.”

“We consider two broad types of controls: taxes and quantity controls. An across-the-board withholding tax on interest, dividends, and profits earned by foreigners creates a fixed wedge between domestic and foreign rates of return. If the withholding tax rate stays constant…then official flows have no effect on the current account because private flows adjust to maintain the fixed differential in the rates of return. Quantity controls place limits on the volume of private financial flows. Binding quotas on inward and outward private financial flows imply that, ceteris paribus, a change in net official flows must be exactly matched by a change in the current account. “

“There are strong reasons to believe that legal controls on financial flows are not the only factor influencing the mobility of capital… We [considered]…the WGI [World Bank’s Worldwide Governance Indicators] rule of law and regulatory quality indexes and the ICRG [The PRS Group’s International Country Risk Guide] composite risk index.”

The medium-term portfolio effect of interventions

“A further result is that there is an important effect of lagged net official flows…Because official flows have permanent effects on the relative supplies of assets in different currencies, they are likely to have long-lasting effects on exchange rates and current accounts through the portfolio balance channel.”

“In a world of risk-averse investors, the uncovered interest rate parity need not hold even in the absence of legal controls and even with high-quality regulatory regimes. Volatile exchange rates are a particularly important source of risk. The portfolio balance theory holds that relative supplies of assets in different currencies will influence the exchange rates between these currencies through investors’ desire to maintain a specific balance of portfolio holdings…An increase in domestic-currency assets will depreciate the domestic exchange rate, setting up expectations of higher future returns relative to returns on foreign currency and thus inducing investors to hold the additional supply.”

“These effects are captured in the coefficients on the lagged stocks of net official assets. An interesting result is that the total effect of lagged official assets is positive and significant in most regressions only when capital mobility is above the median.”

“The finding that interventions have smaller contemporaneous but larger lagged effects in countries with high capital mobility…is line with intuition. Low mobility implies that the flow effect is strong because investors cannot take advantage of arbitrage opportunities to offset official flows. Under low mobility, portfolio rebalancing effects – which require capital to be mobile – exist but matter less as the flow effect dominates. With high mobility, the immediate effect of interventions is greatly attenuated, but the implied changes in relative asset supplies have a small but persistent effect through the portfolio balance channel. It is important to note that the flow coefficient, especially under low mobility, is much larger than the lagged stock coefficient under either low or high mobility.”

“A one percentage point higher lagged stock of net official assets increases the current account by 0.07 percent. Because stocks of official assets typically are larger than flows, this is an important effect. For example, a relatively open economy with net official assets equal to 10 percent of GDP would have a current account that is higher by 0.7 percent of GDP than a comparable country with 0 net official assets, even if net official flows were the same in both countries. Because we have excluded net investment income from the dependent variable, this effect must reflect a lasting effect through the exchange rate rather than simply the earnings on official assets.”

An illustration of misalignments

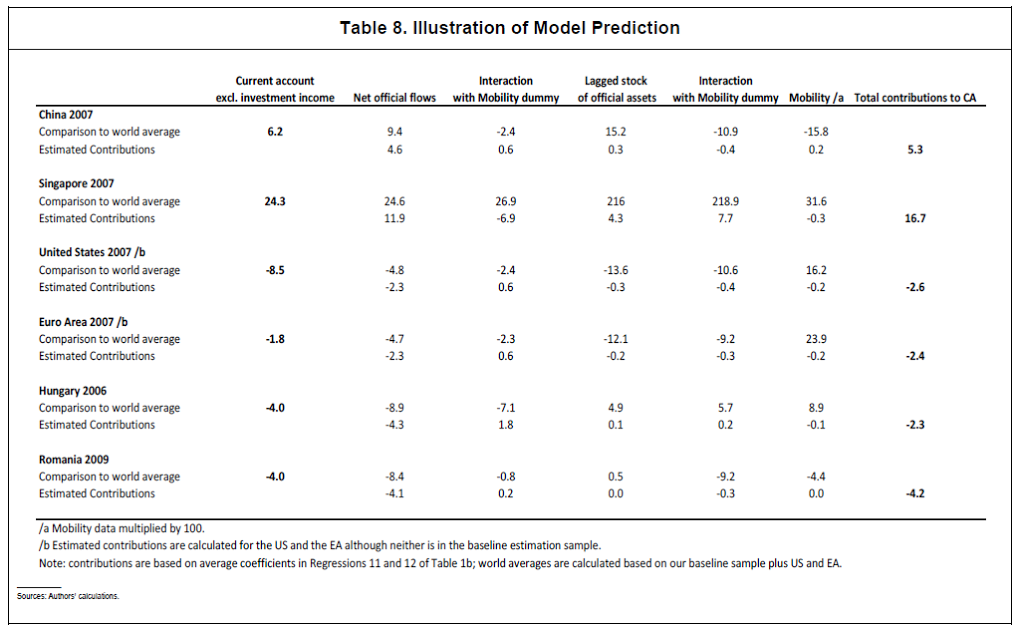

“[The table below] illustrates the importance of the variables central to our analysis for current accounts in specific country examples. It presents data and estimated contributions to the current account in percent of GDP based on our baseline model, relative to world averages. Specifically, it presents the overall effects of net official flows, official stocks, and capital mobility for specific countries and years…All data are expressed as deviations from unweighted averages across countries in percent of GDP.”

“China’s current account excluding net investment income was more than 6.2 percentage points larger than that of the average country in 2007. China’s net official flows were 9.4 percentage points higher than those of the average country… Singapore…had an even larger current account in 2007 but was characterized by high capital mobility. Singapore engages in massive net official flows and has an enormous stock of net official assets. Official flows, stocks, and capital mobility explain just over half of Singapore’s current account…. the United States and the euro area, had current accounts below the global average in 2007. These countries issue the world’s main reserve currencies and do not have significant net official flows or stocks. Because most countries did have positive net official flows and stocks in 2007, the data for these two countries are below the global averages.”