A new IMF paper provides evidence that increased foreign participation in local-currency emerging debt markets has made these significantly more vulnerable to foreign interest rate and risk shocks. Concentration of the investor base and poor economic fundamentals appear to amplify such vulnerability.

Ebeke, Christian and Annette Kyobe (2015), “Global Financial Spillovers to Emerging Market Sovereign Bond Markets”, IMF Working Paper, WP/15/141.

http://www.imf.org/external/pubs/ft/wp/2015/wp15141.pdf

The below are excerpts from paper. Headings and cursive text have been added.

In a nutshell

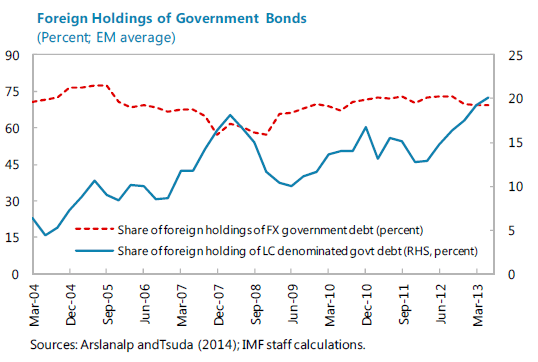

“Foreign participation in EM local-currency sovereign bond markets has increased. EM sovereigns are increasingly…able to borrow domestically long-term and abroad in local currency. While the risk of currency mismatches has decreased, increased foreign participation in local currency markets is associated with increased sensitivity of overall portfolio flows to global financial conditions.”

“Foreign participation and an undiversified investor base transmit global financial shocks to local-currency sovereign bond markets by increasing yield volatility and, beyond a certain threshold, amplify these spillovers…

- Higher foreign participation in local-currency denominated sovereign bond markets increases the transmission of global financial shocks, but especially once a threshold has been reached (foreign participation above 30 percent). Countries which have foreign holdings of local-currency government bonds around or above the 30 percent threshold are: Argentina, Hungary, Indonesia, Latvia, Malaysia, Mexico, Peru, Poland, South Africa, and Ukraine…

- Higher foreign holdings of foreign-currency denominated bonds do not appear to have an impact on the transmission of shocks…

- A higher concentration of the investor base (approximated using disaggregated data of the institutional profile of investors holdings EM total government debt) makes EM local-currency sovereign yields more sensitive to global financial shocks…

- Strong macroeconomic fundamentals—such as low inflation, strong and stable output growth, and moderate public debt levels—help reduce the level and the volatility of EM sovereign bond yields.”

On the rapid growth of local-currency EM bond markets and the FX risk transference from local borrowers to global asset managers view post here.

Investigation of global shock transmission

“This paper investigates the role of foreign participation in transmitting global financial shocks into EM government bond markets…Our sample uses quarterly data for 17 emerging market economies over 2004:Q1–2013:Q3. Countries in the sample are Argentina, Brazil, Colombia, Egypt, Hungary, India, Indonesia, Latvia, Lithuania, Malaysia, Mexico, Peru, Philippines, Poland, Romania, South Africa, Thailand, and Ukraine.”

“There are several channels through which external shocks may affect EM sovereign bond yields:

- The liquidity channel is captured by the U.S. 3 month t-bill rate. Higher t-bill rates raise the opportunity cost of investing in EM assets.

- The portfolio balance channel is captured by the U.S. 10-year Treasury bond rate. This measure captures the effect Fed action can have on long-term yields, resulting in portfolio rebalancing.

- The confidence channel indicator is [represented by] the VIX [the S&P500 implied equity volatility index]. The indicator captures market sentiment (global risk aversion) for investing in risky assets.”

“The dependent variables are the level and volatility of the 5-year local currency yield…Foreign participation is measured as foreign holdings of local-currency denominated government debt in percent of total government local-currency denominated government debt.”

On the importance of foreign participation in local EM debt

“Higher foreign participation increases the volatility of the yield, but decreases the level of the yield.

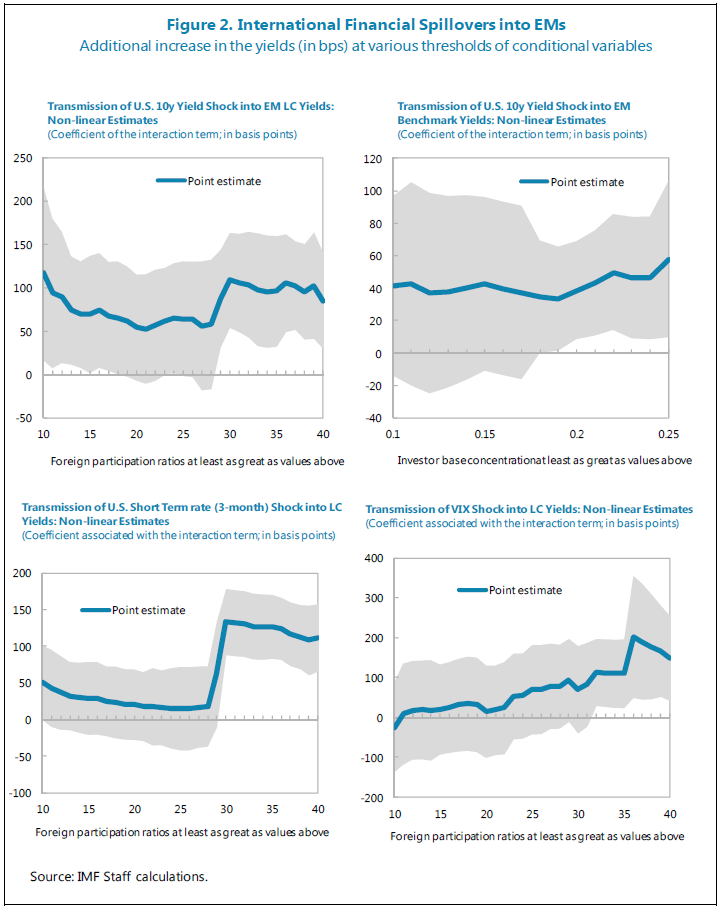

- We find that the transmission of shocks to the level of the local-currency yields is amplified at higher levels of foreign participation. In particular, the results suggest that foreign participation above 30–35 percent increases the transmission of global financial shocks in a significant way…As this level of foreign participation has mostly been reached by a number of EMs (Peru, Indonesia, Latvia, Hungary and Poland) after the global financial crisis, our econometric results suggest that the post-crisis period has therefore seen an intensification of financial spillovers into these EMs.

- When foreign holdings of local currency bonds lie above 35 percent, the transmission of a shock to the U.S. 10 year yield is amplified by an additional 100 bps. Past the 35 percent threshold, a 100 bps increase in the U.S. yields results in a rise in EM yields of around 140 bps (compared with an increase of only 40 bps below the 35 percent threshold).

- The transmission of shocks from the U.S. 3 month yield also depends on the degree of foreign participation, especially when it exceeds 30 percent. Past this threshold, a 100 bps increase in U.S. short-term interest rates increases EM yields by 140 bps (compared with no significant impact below the threshold)…

- In periods of global risk aversion (captured by a rising VIX), EMs in which foreign holdings reach around 32 percent of outstanding local currency-denominated bonds experience a larger impact from a shock to the VIX. A two-standard deviation shock in the VIX translates to a 130 bps increase in yields in EMs with foreign participation past the threshold (compared to no significant impact below the threshold).”

On the role of foreign participation in EM dollar debt

“The extent of foreign holdings of foreign currency-denominated bonds is not found to have an impact on either the level or the volatility of foreign currency-denominated bond yields. One possible explanation is the role of currency risk, which is important in the case of local currency-denominated bonds.”

On the importance of FX risk for local EM bond yields view post here.

On the role of concentration of the investor base

“The concentration of the investor base also matters for the transmission of global financial shocks. Our estimates suggest that a threshold of investor base concentration exists around the median of the Herfindahl index in the sample (around the value of 0.2). A high concentration of the investor base (above the 0.2 threshold) makes EM local-currency sovereign yields more sensitive to global financial shocks. A 100 bps increase in the 10-year U.S. yield increases local-currency sovereign bond yields by 70 bps when the investor base is significantly concentrated (i.e., above the 0.2 threshold) compared to 30 basis points when it is more diversified (below the threshold).”

On the rise and concentration of dedicated EM asset management view post here.

On the role of macroeconomic “fundamentals”

“Stronger macroeconomic fundamentals are generally associated with lower yield levels and reduced yield volatility. Higher indebtedness increases yield volatility, as does higher output growth volatility. Both factors serve to increase uncertainty in the real economy, which likely spills over into greater bond yield volatility. Higher real GDP growth decreases the level and volatility of both local and foreign-currency bond yields, as better growth prospects encourage more capital inflows and the country’s debt burden becomes easier to service.”