Assessing the risk of equity market “crashes”, academic work has focused on price-earnings ratios and bond-stock earnings yield differentials. A recent paper by Lleo and Ziemba provides theoretical reasoning and empirical support for these warning signs.

Lleo, Sebastien and William Ziemba (2014), “Does the Bond-Stock Earning Yield Differential Model Predict Equity Market Corrections Better Than High P/E Models?”, SRC (Systemtic Risk Centre) Discussion Paper No 18 August 2014

http://eprints.lse.ac.uk/59290/

The below are excerpts from the paper. Emphasis and cursive text have been added.

Crash prediction models in academia

“Considerable efforts have…gone into understanding to what extend long-term returns are predictable. [The table below shows] the evolution of the Price-Earnings ratio over selected 20-year periods with high annualized returns. In each period the P/E ends 1.6 to 4.7 times higher than it started. Furthermore, there is a 90% correlation between annualized returns and ending P/E ratio.”

“Ziemba and Schwartz (1991) published the first crash prediction model, called the bond-stock earnings yield differential model (BSEYD). The focus of the BSEYD is not on forecasting a specific level of performance but on predicting a specific type of rare market event…The Bond-Stock Earnings Yield relates the yield on stocks (measured by the earnings yield) to the yield on nominal Treasury bonds [by subtracting the former from the latter].”

“Consigli, MacLean, Zhao, and Ziemba (2009) propose a stochastic model of equity returns based on an extension of the BSEYD model inclusive of a risk premium in which market corrections are endogenously produced by the bond-stock yield difference.”

“Maio (2013) also shows that the ‘yield gap’, which corresponds to the difference between the earnings yield (or dividend yield) on a stock market index and the long-term yield on Treasury bonds, predicts returns better than other models based on dividend yield.”

Crash prediction measures and asset pricing models

“The first contribution of this paper is to relate…[Price-Earnings and Bond Stock Earning Yield Differential] models to asset pricing theory…The BSEYD uses price and earnings. The BSEYD also factors in prevailing interest rate levels. We can… relate the BSEYD model to the equity risk premium, earnings growth and government bond yield, [which would stipulate that in equilibrium the BSEYD should depend negatively on the equity risk premium (f) and relate to earnings growth (g), the dividend payout ratio (d) and the yield on the government bond (r) according to the below formula:]”

“The BSEYD model is closely related to the Fed Model…In its most popular form, the Fed model states that in equilibrium, the one year forward looking earnings yield of the S&P500 [based on one year forward looking earnings] should equal to the current yield on a 10-year Treasury Note.”

Statistical significance tests for crash prediction

“Crash prediction…statistical tests are conducted with respect to events, namely equity market corrections, as opposed to returns…Fundamentally, one can give correction prediction models a binary interpretation: a market crash either occurs or not… This means that correction prediction models are nonlinear but simple. Using this binary interpretation, it is possible to conduct the tests efficiently using a likelihood ratio. “

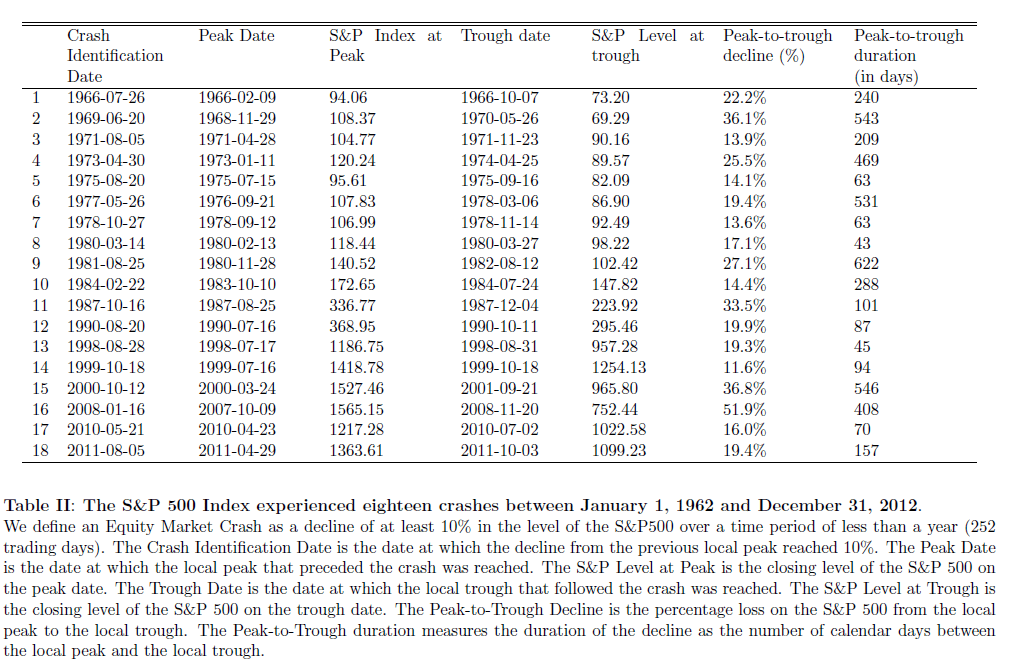

“In our analysis, we use daily S&P 500 data from January 1, 1950 to December 31, 2012, and earnings and P/E data for the period January 29, 1954 to December 31, 2012… We define an equity market crash as a decline of at least 10% in the level of the S&P500 over a time period of at most a year (252 trading days). [The table below] shows the 18 crashes that occurred between January 1, 1962 and December 31, 2012.”

“Crash prediction models such as the BSEYD model or the continuous time disorder detection model generate a signal to indicate a downturn in the equity market at a given horizon. This signal occurs whenever the value of a specific measure (in our case P/E or BSEYD) crosses a threshold… We define the threshold as a confidence level. We start with a standard 95% one-tail confidence interval based on a Normal distribution.”

“Bond Stock Earning Yield Differential [BSEYD]…the logarithmic BSEYD model, and to a lesser extent the P/E [Price/Earnings] ratio, are statistically significant robust predictors of equity market crashes… regardless of the definition of earnings and of the model used for the threshold. The BSEYD and logBSEYD models based on average earnings are significant at or near the 99.5% level. The P/E measure is statistically significant at a 95% level across all model specifications. On the other hand, the logP/E measure does not appear to have crash prediction ability.”