The rapid growth in local-currency bond markets in emerging countries has transferred foreign exchange risk from local borrowers to global institutional investors and mutual funds. Gross capital inflows have soared, magnifying the dependence of flows on mutual fund holdings, particularly on volatile open-ended fixed income funds. In the wake of these changes the “beta” of local emerging market assets has risen and the tendency towards herding has increased.

IMF Global Financial Stability Report, March 2014, Chapter 3

http://www.imf.org/External/Pubs/FT/GFSR/2014/01/pdf/c2.pdf

The below are excerpts from the report. Emphasis and cursive text has been added.

Structural changes in emerging markets

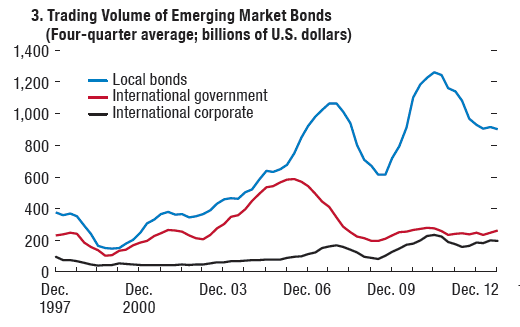

“Improved fundamentals in emerging market economies and the persistently low yields in advanced economies have…helped foster the development of local financial markets and of new asset classes, such as local-currency-denominated sovereign debt. Global investors are directly entering local currency bond markets, while the local institutional investor base has also been expanding. At the same time, the relative role of cross-border bank lending has declined.”

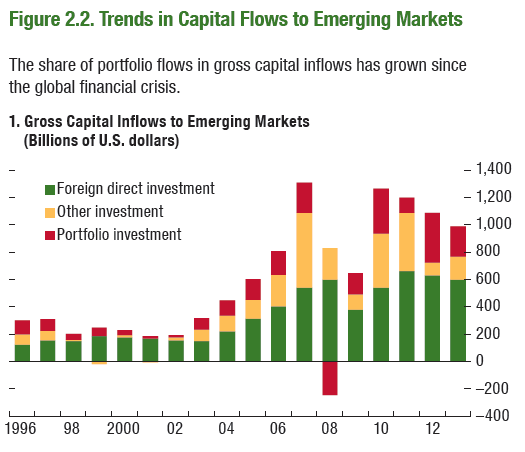

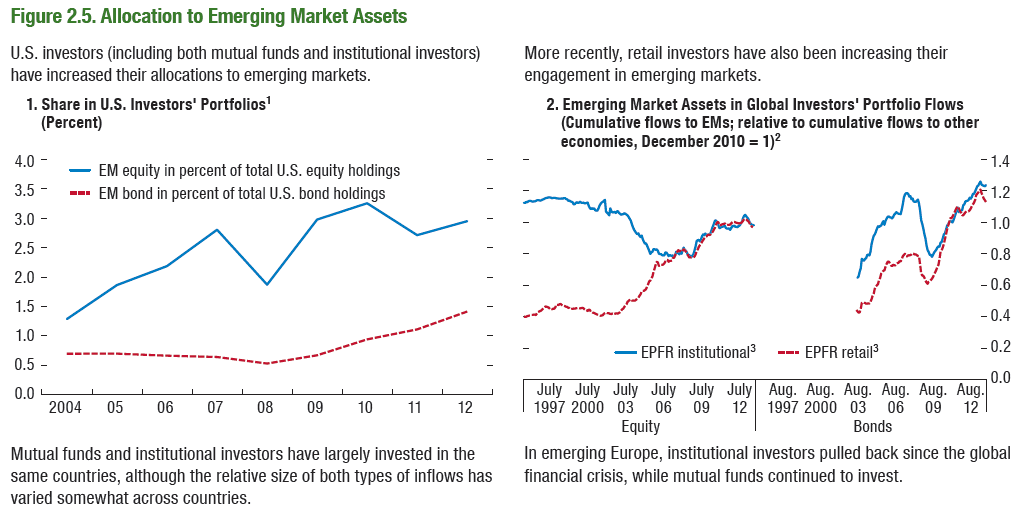

“Over the past decade, institutional investors have been allocating more funds to emerging markets. Despite differences in mandates, all types of institutional investors are attracted to emerging market assets by their relatively high returns. Economic growth trends, real currency appreciation, and deepening capital markets in emerging market economies have spurred the demand for emerging market assets…Gross capital flows to emerging markets have quintupled since the early 2000s, and the most volatile component—portfolio flows—has become a more important part of the mix. Since the global financial crisis, portfolio flows to these economies—especially bond flows—have risen sharply.”

Reasons and evidence of increased vulnerability

“The ability of governments to issue their debt in local currency has reduced their currency mismatches, but the transfer of exchange rate risk to investors may have made portfolio flows more volatile….The role of bond funds, especially local currency bond funds, open-end funds with easy redemption options…has risen… The composition of international mutual funds investing in emerging markets has been changing, with a growing importance of globally operating funds that do not focus on emerging markets…Growing investment from institutional investors that are generally more stable during normal times is welcome, but these investors can pull back more strongly and persistently when facing an extreme shock.”

“Fixed-income flows are substantially more sensitive to global push factors than are equity flows, and their importance in overall capital flows is growing…Mutual fund investor flows…are generally more sensitive to global factors than those of institutional investors, and they are expanding exposures to emerging markets, making flows more sensitive to push factors.”

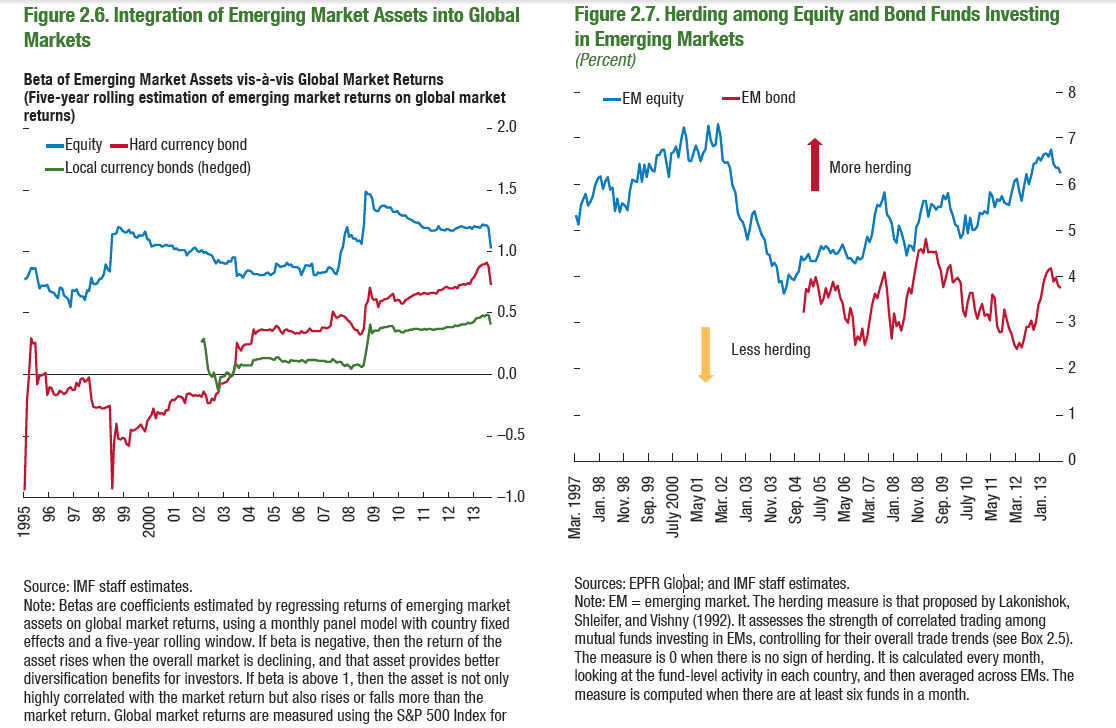

“As emerging markets have become increasingly integrated with global markets, global factors have increasingly driven emerging market asset returns. Although the heightened correlation of local asset returns with global market returns (beta) during the global financial crisis may partly reflect the effects of higher asset volatility typical of weak markets, equity beta has remained at high levels (above one) since then… At the same time, herding among international equity investors is on the rise. If international investors buy or sell assets simply because they observe other investors doing so, this can amplify boom-bust cycles in financial markets.”

“While domestic macroeconomic conditions matter, investor herding among global funds continues, and there are few signs of increasing differentiation along macroeconomic fundamentals during crises over the past 15 years.”