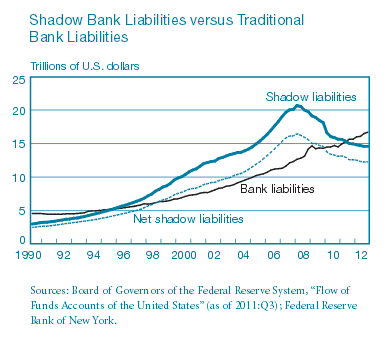

The New York Fed’s Economic Policy Review provides a basic overview of past and current shadow banking activities in the U.S. and beyond. Securitization and non-bank wholesale funding remain at the heart of the system. The relevance of shadow banking is likely to recover, as capital and liquidity standards in the regulated banking system are tightening.

http://www.newyorkfed.org/research/epr/2013/0713adri.html

The below are excerpts from the paper and the post. Cursive text and emphasis have been added.

What is shadow banking?

“Shadow banking activities consist of credit, maturity, and liquidity transformation that take place without direct and explicit access to public sources of liquidity or credit backstops.”

“Shadow credit intermediation performs an economic role similar to that of traditional banks’ credit intermediation. The shadow banking system decomposes the simple process of retail-deposit-funded, hold-to-maturity lending conducted by banks into a more complex, wholesale-funded, securitization- based lending process.”

How does shadow banking work?

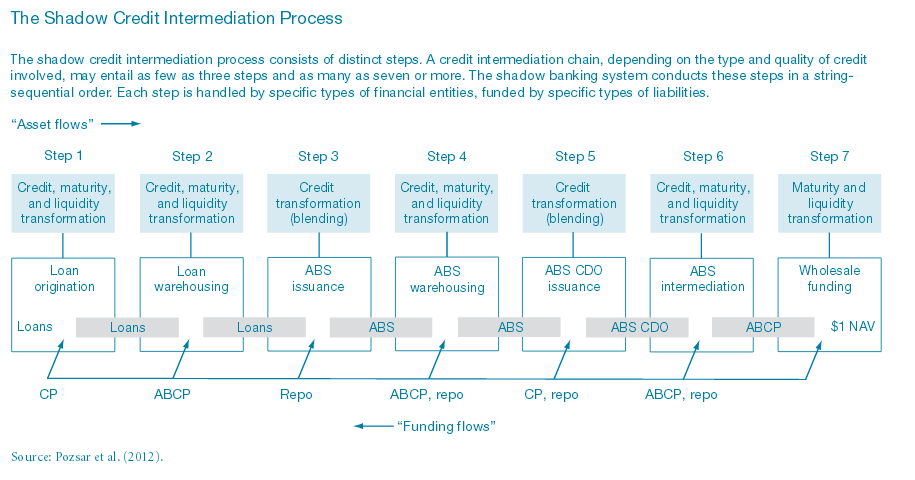

“Like traditional banks, shadow banks conduct financial intermediation. However, unlike in the traditional banking system, where credit intermediation is performed “under one roof ”—that of a bank—in the shadow banking system it is performed through a chain of nonbank financial intermediaries in a multistep process… The shadow banking system performs these steps of intermediation in a strict, sequential order. Each step is handled by a specific type of shadow bank and through a specific funding technique.

- Loan origination (such as auto loans and leases, non-conforming mortgages) is performed by finance companies that are funded through commercial paper and medium-term notes.

- Loan warehousing is conducted by single- and multi-seller conduits [investment vehicles that hold medium to long-dated assets] and is funded through asset-backed commercial paper (ABCP).

- The pooling and structuring of loans into term asset-backed securities are conducted by broker-dealers’ ABS syndicate desks.

- ABS warehousing is facilitated through trading books and is funded through repurchase agreements, total return swaps, or hybrid and repo conduits.

- The pooling and structuring of ABS into CDOs [collateralized debt obligations] are also conducted by broker-dealers’ ABS syndicate desks.

- ABS intermediation is performed by limited-purpose finance companies, structured investment vehicles (SIVs), securities arbitrage conduits, and credit hedge funds, which are funded in a variety of ways including, for example, repos, ABCP [Asset Backed Commercial Paper], MTNs [Medium Term Notes], bonds, and capital notes.

- The funding of all of the above activities and entities is conducted in wholesale funding markets by funding providers such as regulated and unregulated money market intermediaries… In addition to these cash investors—which fund shadow banks through short-term repo, CP, and ABCP instruments—fixed-income mutual funds, pension funds, and insurance companies fund shadow banks by investing in their longer-term MTNs and bonds.”

Who is involved in shadow banking?

“We identify three subgroups of the shadow banking system:

- The government-sponsored shadow banking subsystem refers to credit intermediation activities funded through the sale of agency debt and MBS…Government-sponsored enterprises,… include the Federal Home Loan Bank [FHLB] system in 1932, the Federal National Mortgage Association [Fannie Mae, 1938], the Government National Mortgage Association [Ginnie Mae, 1968], and the Federal Home Loan Mortgage Corporation [Freddie Mac, 1970]…Arguably, they were the first providers of term warehousing of loans and invented the originate-to-distribute model of securitized credit intermediation… GSEs largely securitize their loan and mortgage portfolios in pools of mortgage-backed securities, which are referred to as agency MBS. These MBS pass interest payments and principal payments through to the MBS holder, but the credit risk is retained by the GSEs. Agency MBS thus incorporate interest rate and prepayment risk, but not the default risk of individual borrowers.

- The “internal” shadow banking subsystem refers to the credit intermediation process of a global network of banks, finance companies, broker-dealers, and asset managers and their on- and off-balance-sheet activities—all under the umbrella of financial holding companies…The largest banks and dealers played a central role…in the origination, warehousing, securitizing, and funding of credit. As a result, the nature of banking changed from a credit-risk- intensive, deposit-funded, spread-based business to a less credit-risk-intensive, wholesale-funded process subject to run risk.

- The “external” shadow banking subsystem refers to the credit intermediation process of diversified broker-dealers and a global network of independent, nonbank financial specialists that includes captive and stand-alone finance companies, limited-purpose finance companies, and asset managers. The origination, warehousing, and securitization of loans are conducted mainly from the United States, but the funding and maturity transformation of structured credit assets are conducted from the United States , Europe, and offshore financial centers.… The external shadow banking subsystem is defined by 1) the credit intermediation process of diversified broker- dealers, 2) the credit intermediation process of independent, nonbank specialist intermediaries, and 3) the credit puts provided by private credit-risk repositories.”

Why shadow banks remain a systemic issue

“The funding of credit through the shadow banking system significantly reduced the cost of borrowing during the run-up to the financial crisis, at the expense of increasing the volatility of the cost of credit through the cycle.”

“Increased capital and liquidity standards for depository institutions and insurance companies are likely to increase the returns to shadow banking activity. For example, as pointed out in Pozsar (2011), the reform effort has done little to address the tendency of large institutional cash pools to form outside the banking system. Thus, we expect shadow banking to be a significant part of the financial system, although almost certainly in a different form, for the foreseeable future. ”

“In contrast to traditional banking’s public sector guarantees, the shadow banking system…[used] contingent lines of credit and tail-risk insurance in the form of wraps and guarantees. The credit lines and tail-risk insurance filled a backstop role for shadow banks…These forms of liquidity and credit insurance provided by the private sector, particularly commercial banks and insurance companies, allowed shadow banks to perform credit, liquidity, and maturity transformation by issuing highly rated and liquid short-term liabilities. However, these guarantees also acted to transfer systemic risk between the core financial institutions and the shadow banks…The failure of private sector guarantees to support the shadow banking system occurred mainly because the relevant parties—credit rating agencies, risk managers, investors, and regulators—underestimated the aggregate risk and asset price correlations. “