Modern shadow banking provides large-scale risk transformation services that are highly pro-cyclical (view post here). This is a systemic concern mainly for one reason: most shadow banking activities lack formal transparent backstops, i.e. external risk absorption mechanisms that prevent large negative shocks from escalating.

“What Is Shadow Banking?”, Stijn Claessens and Lev Ratnovski, IMF Working Paper, WP/14/25

http://www.imf.org/external/pubs/ft/wp/2014/wp1425.pdf

The below are excerpts from the paper. Cursive lines and emphasis has been added

What is shadow banking?

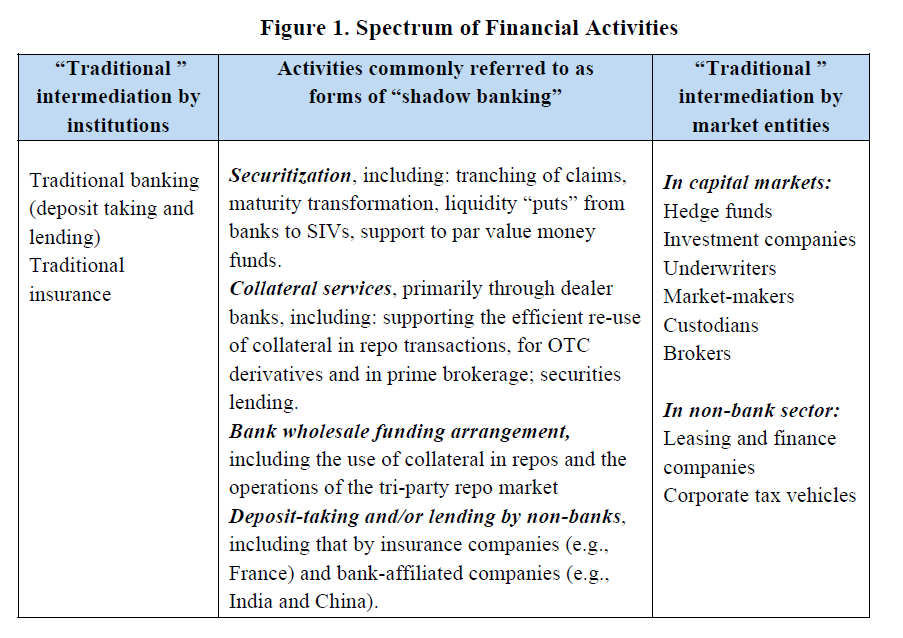

“We propose to describe shadow banking as ‘all financial activities, except traditional banking, which require a private or public backstop to operate.’ This description captures many of the activities that are commonly referred to as shadow banking today, as shown [below].”

“Only activities that need a backstop – because they combine risk transformation, low margins and high scale with residual ‘tail’ risks – are systemically-important shadow banking.”

Why does shadow banking need a backstop?

“Shadow banking, just like traditional banking, involves risk – credit, liquidity, and maturity risks – transformation… The purpose of risk transformation is to strip assets of ‘undesirable’ risks that certain investors do not wish to bear, as they do not have the competitive advantage [or] as regulations inhibits the type of risks they can take on…Shadow banking…aims to distribute the undesirable risks across the financial system…For example, in securitization shadow banking strips assets of credit and liquidity risks through tranching and providing liquidity puts. Or it facilitates the use of collateral to reduce counterparty exposures in repo markets and for OTC derivatives.”

“While shadow banking thus uses many capital markets type tools, it differs also from traditional capital markets activities – such as trading stocks and bonds – in that it needs a backstop. This is because, while most undesirable risks can be distributed and diversified away, some residual risks, often rare and systemic ones (‘tail risks’), can remain. Examples of such residual risks include systemic liquidity risk in securitization, risks associated with large borrowers’ bankruptcy in repos and securities lending, and the systematic component of credit risk in non-bank lending (e.g., for leveraged buyouts).”

“Shadow banking cannot generate the needed ultimate risk absorption capacity internally. The reason is that shadow banking activities have margins that are low, too low to support a backstop by themselves. To be able to easily distribute risks across the financial system, shadow banking focuses on ‘hard information’ risks that are easy to measure, price…credit scores and verifiable information.”

What type of backstop does shadow banking need?

“Shadow banking needs access to a backstop, i.e., a risk absorption capacity external to the shadow banking activity. The backstop for shadow banking also needs to be sufficiently deep. First, shadow banking usually operates on large scale, to offset significant start-up costs, e.g., of the development of infrastructure, and given the low margins. Second, residual, ‘tail’ risks in shadow banking are often systemic, so can realize en masse.”

“There are two ways to obtain such a backstop externally. One is private – by using the franchise value of existing financial institutions. This explains why many shadow banking activities operate within large banks or transfer risks to them… Another is public – by using explicit or implicit government guarantees. Examples include…the Federal Reserve securities lending facility that backstops the collateral intermediation processes, the implicit too-big-to-fail guarantees for tri-party repo clearing banks and other dealer banks , the bankruptcy stay exemptions for repos which in effect guarantee the exposure of lenders, or the implicit, reputational and other guarantees on bank-affiliated.”