Nomura research has summarized evidence of oversupply of residential property in China. Urban floor space per capita is now estimated to be higher than in some developed countries. Land conversion is still rising, while urbanization is slowing. Potential triggers for a sharp correction include interest rate liberalization, capital outflows and property taxes. A plunge in property activity would have serious economic and financial consequences.

“China’s property sector overinvestment, Part 1: The property market is the top risk”, Nomura Global Markets Research, 14 March 2014.

The below are excerpts from the reports. For access please contact your local Nomura representative. Cursive lines and emphasis have been added.

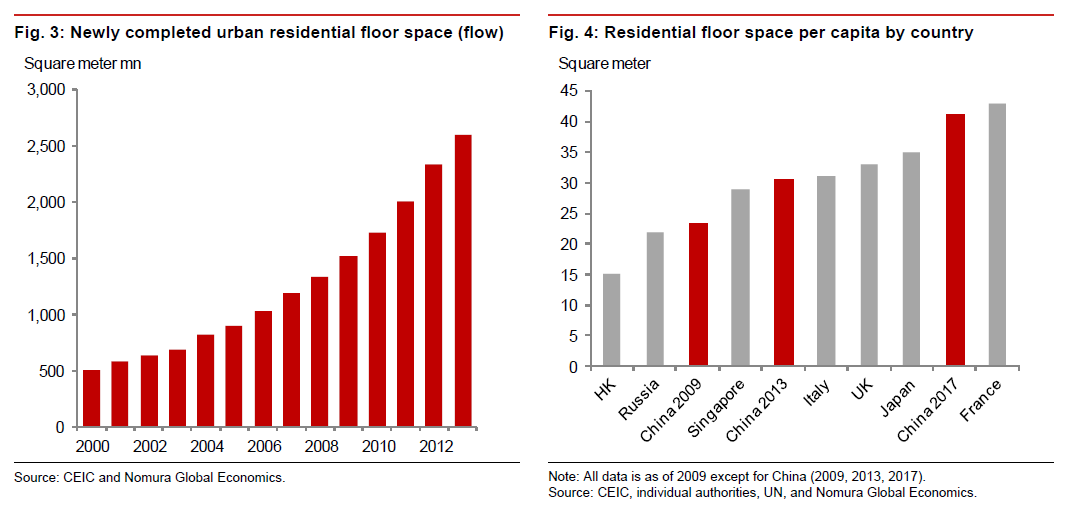

“In 2000, there was only 497 million square meters of newly completed urban residential floor space, but by 2013, this number rose to 2596 million square meters, an astonishing 423% increase. This implies average growth of 13.6% per year during this period, compared with average urban population growth of 3.7%.”

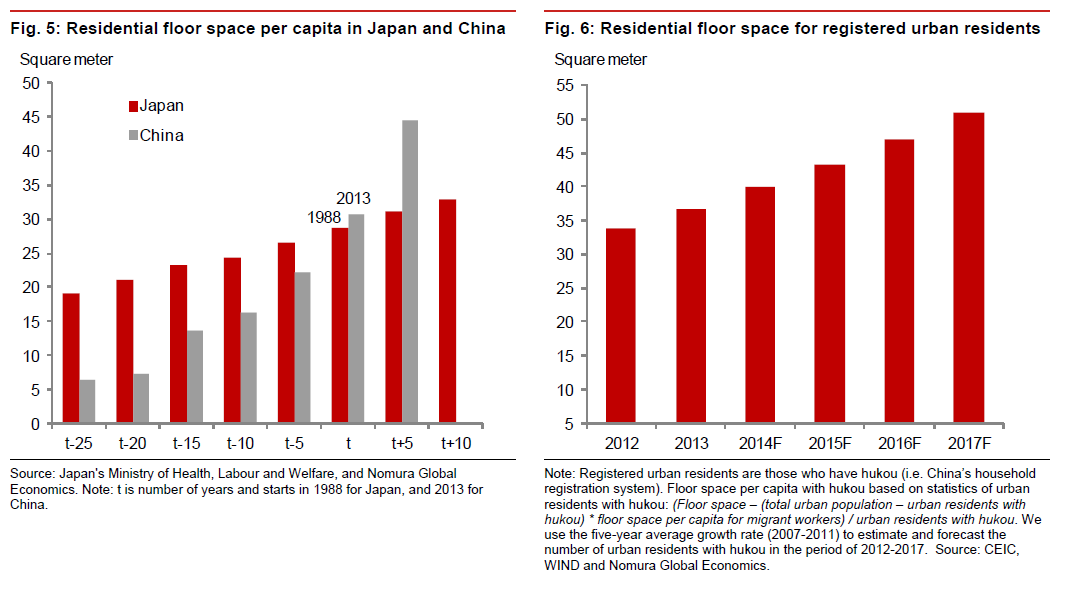

“We estimate residential floor space per registered urban resident may have reached 37 square meters by 2013, compared to 35 in Japan and 33 in UK. If the current trend holds, it will reach 51 square meters by 2017. Official data show inventory has risen by 182% from 2009 to 2013, yet land sales suggest that supply is set to rise quickly in coming years…In 2011 there were only two cities that were widely reported as ghost towns, but there are now more than 10 cities facing this type of problem.”

“First- and second-tier cities are much less important than the other cities. The four first-tier cities (Beijing, Shanghai, Guangzhou and Shenzhen) accounted for only 5% of housing under construction and sales (both in square meter terms) and 8% of housing

investment in 2013 (in RMB terms). The 24 second-tier cities (mostly provincial capitals) only accounted for 28% of housing under construction…The remainder, a large number of third- and fourth-tier cities, comprised 67% of housing under construction… Property data for most third- and fourth-tier cities are not readily available, so it is difficult to gain a sufficient understanding of the current situation in these locations. Anecdotal evidence on a city level suggests that the situation is worsening.”

“Land sales soared by 52.4% in 2013 in value terms… We estimate that, in volume terms, land sales rose by 7.0% in first-tier cities, 3.7% in second-tier cities, and 23.2% in third- and fourth-tier cities in 2013 . They rose by 159.3%, 34.2% and 57.0%, respectively, in value terms. These increases partly reflect incentives from local governments aimed at boosting land sales to help ease financing pressures faced by local financing vehicles…This raises the supply of properties in the pipeline and exacerbates the demand-supply imbalance even further.”

Worsening demographics and urbanization trends

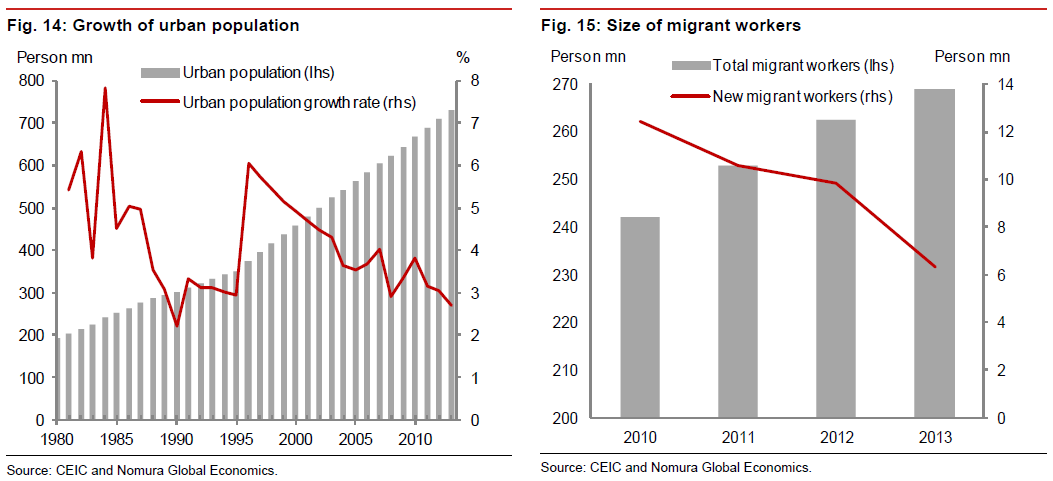

“The demographic trend became unfavourable for housing demand in 2012, when the working-age population dropped by 3.45m, its first decline since 1996. The…working age population dropped again by 2.27m in 2013. We believe this is a result of the one-child policy and expect this trend to continue in coming years.”

“If urbanisation continues at a rapid pace, properties that are vacant today may be filled by immigrants from rural areas. Indeed China’s urbanization ratio is still low at 53.7% in 2013 compared to over 80% in some developed economies… However… the size of the urban population grew by only 2.7% in 2013, its slowest rate of growth since 1996 and much lower than the average annual growth rate of 4% from 2000 to 2010. .. We believe urbanisation will continue to slow in coming years, as industrialisation slows, surplus rural labour is depleted, and local government attempts to expand urban areas are constrained.”

Potential triggers of a property price correction

“Several macro factors could trigger a correction in the property market, including a rise in interest rates, an opening up of capital account, the introduction of a property tax, and the anti-corruption movement…

- In recent years, financial liberalisation has been an objective of the government, and recent policies have resulted in more flexible interest rates… the Governor of the People’s Bank of China, Zhou Xiaochuan, indicated that the deposit interest rate will likely be liberalised in one to two years, and he expects interest rates to rise as a result… even the partial interest rate liberalisation enacted thus far has already led to higher interest rates.

- Contrary to conventional wisdom, China‟s capital account is actually quite volatile, despite pervasive capital controls. In fact, China’s capital account volatility in 2013, as measured by the move of the financial account balance (i.e., net capital flows) as a share of GDP on quarterly basis , was similar to India’s and Brazil’s. .. A more open capital account allows Chinese investors to diversify their investments globally. This applies to corporates as well as households.

- On 24 February at the G20 meeting, Minister of Finance Lou Jiwei said that China will speed up the implementation of property tax reform. China still does not collect a property holding tax on a national level, but there are a few pilot programs, including one in Shanghai.

- The new leadership in China has been pushing its anticorruption movement since taking over in early 2013. This has led to numerous officials being arrested on corruption charges… We believe the risks to corrupt officials from holding properties in China have risen, as the government has developed a database to track property ownership in major cities. Indeed, we have witnessed a growing list of high-profile cases where officials who hold numerous properties are prosecuted.”

Recent evidence of property price correction

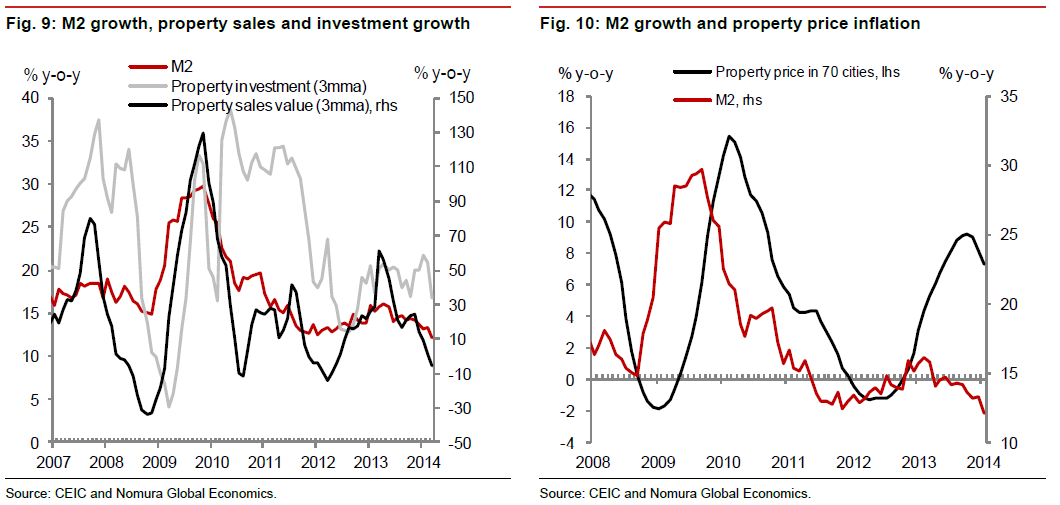

“Property investment growth turned negative in four of China’s 26 provinces in Q1 2014. In two provinces it fell by 25% y-o-y. Every property market leading indicator at the national level turned down in Q1, and for most monthly indicators the rate of decline accelerated through the quarter… We believe the correction in the property market was triggered by monetary policy tightening that started in mid-2013. Indeed, property market cycles in China have been driven by monetary policy. The turning points in M2 growth match the turning points of property sales and transaction-based prices reasonably well, and lead the turning points of property investment growth.”

Why a property market correction is a systemic risk

“[Property investment] has become a pillar of growth for China, making up 16% of GDP, 33% of fixed asset investment, 20% of outstanding loans, 26% of new loans, and 39% of government revenues in 2013. If it slows sharply, we see no obvious replacement to support growth.”

“We highlight four transmissions through which the systemic importance of the property sector is illustrated…

- Direct property investment comprised 26% of total fixed asset investment in 2013. Furthermore, the property sector is highly connected to other manufacturing and services sectors, such as construction, steel, cement, chemical, transportation and leasing industries… An estimated 33% of total investment was directly and indirectly attributable to the property sector in 2013 [implying that it contributed 16% to GDP]. This suggests that a 10% drop in property investment would reduce GDP growth by 1.6pp…

- Infrastructure investment is mostly financed by…local government financing vehicles that depend heavily on land sales for revenue, which in turn depend on booming property markets. Infrastructure and property investment combined accounts for approximately half of total investment….

- In 2013, the share of property loans (including mortgage loans and loans to developers) to total outstanding loans rose to 20% from 14% in 2005…In addition, we believe property developers are major borrowers in the shadow banking sector, although their actual exposure is unclear.

- Total government revenues reached…29% of GDP in 2013….39% of which was related to the property market. Specifically, land sales accounted for 23% of total government revenues. Property-related taxes accounted for …15% of total government revenue in 2013. Local governments are more reliant on land sales than the central government, and their fiscal conditions have become increasingly challenging.”