An empirical paper by Prokopczuk and Symeonidis investigates the drivers of commodity price volatility over the past 50 years. On the economic side inflation changes had been critical until price growth compressed over the past decade. Also economic recessions have been conducive to larger (industrial) commodity fluctuations. From the 2000s the importance of financial risk variables has gained weight, an apparent tribute to the “financialisation” of commodities trading.

“The economic drivers of time-varying commodity market volatility”,

Marcel Prokopczuk and Lazaros Symeonidis

http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2013-Reading/papers/EFMA2013_0441_fullpaper.pdf

The below are excerpts from the paper. Cursive text and emphasis have been added.

Scope and main points of the paper

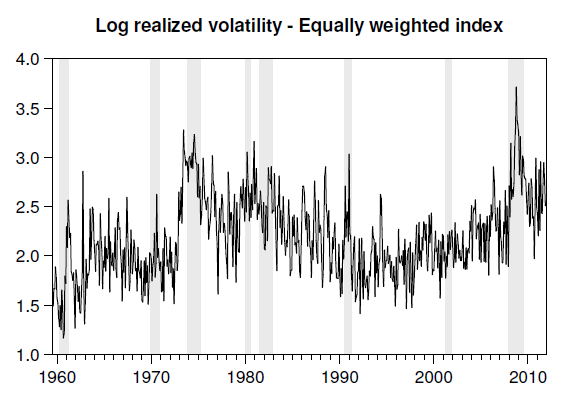

“Our data source is the Commodity Research Bureau (CRB). We employ the entire history of daily prices available for each commodity futures contract. The longest sample covers the period from July, 1959 to December, 2011…The 33 commodities included in our index can be classified in four different categories: (i) Agricultural (grains and soft commodities), (ii) Livestock, (iii) Energy and (iv) Metals (industrial and precious metals)… A proxy for commodity market volatility of month t is computed as the square root of the sum of daily squared returns.”

“During recessions aggregate commodity market volatility is higher on average. Inspecting the individual commodity groups, we observe that volatility is significantly higher for metals, but not for agricultural and livestock portfolios.”

“Inflation volatility appears to be the most significant individual predictor [of commodity price volatility] in economic and statistical terms…inflation volatility is highly significant at the 1% level for the whole sample period of 1970–2011…This positive effect may be related to the higher trading activity in commodities during periods of high inflation uncertainty since they are widely considered as good a hedge against inflation. In the 2001–2011 sub-period, which includes the recent commodity price boom, the significance and the magnitude of the impact of inflation uncertainty seems to weaken.”

“We find evidence of a strong bi-directional causal link between inflation uncertainty and commodity return volatility…During the recent period after the ’90s there is more evidence that commodity volatility causes inflation volatility than the other way around.”

“Constructing proxies of macroeconomic uncertainty based on the BlueChip Economic Indicators survey, we [find that]…differences in beliefs of professionals regarding short-term economic fundamentals have a strong effect on aggregate commodity market volatility. Moreover, the macroeconomic uncertainty measures based on survey expectations contain information additional to that already contained in macroeconomic volatility estimates.”

The impact of market uncertainty

“Factors related to financial market conditions, such as the default return spread, the term spread or the VIX offer explanatory power for many portfolios and sub-periods. Controlling for commodity-specific factors, we observe that these are significant determinants of commodity return volatility in many cases.”

The impact of commodity specific factors

“We construct aggregate measures of variables that are central to fundamental commodity pricing theories, namely the theory of storage and the theory of normal backwardation (view post here). Specifically, we focus on aggregate measures of: (i) the commodity futures basis, (ii) the growth of open interest in commodity futures and (iii) the hedging pressure of commercial and non-commercial traders, respectively.”

“We observe that the measure of aggregate commodity futures basis, although insignificant in the entire sample period, enters with a highly significant and large in absolute value coefficient in the second half of the sample (1991–2011). Its sign is negative and consistent with the predictions of the theory of storage.”

“Furthermore, the effect of aggregate hedging pressure is positive for aggregate commodity market volatility and significant at the 5% level, while its sign suggests that volatility increases with higher hedging demand…Speculative pressure, on the other hand, is important only in the period after 2000.”

“This result can be regarded as evidence that even though commodity markets have become more integrated with financial markets, they are still segmented to some extent.”