A new IJCB article shows that historically [i] inflation expectations had a strong impact on long-term yields and [ii] economic data surprises had a strong impact on inflation expectations. However, the influence of compensation for inflation and inflation risk on U.S. bond yields has faded in the era of non-conventional monetary policy.

Bauer, Michael, “Inflation Expectations and the News”, International Journal of Central Banking March 2015

http://www.ijcb.org/journal/ijcb15q2a1.htm

The below are excerpts from the article. Emphasis and cursive text have been added.

Inflation compensation and bond yields

“This paper uses two sources of information about inflation compensation: spreads in yields on nominal and inflation-indexed bonds [“TIPS” or U.S. Treasury Inflation Protected Securities whose par value rises with CPI inflation], and inflation swap rates…The break-even inflation rate is the difference between a nominal Treasury yield and the corresponding TIPS yield of the same maturity… that makes investments in indexed and non-indexed bonds equally profitable….Inflation swaps are financial contracts in which one party pays a fixed interest rate, the swap rate, and the other party pays the CPI inflation rate on an underlying notional….I also include an additional, novel measure of inflation compensation, which incorporates information from both sources and includes a liquidity adjustment.”

“Due to the risk of changes in inflation, inflation compensation generally contains an inflation risk premium… I focus on documenting patterns in inflation compensation and do not attempt to correct for a risk premium.”

“Unconditional correlations between daily changes in inflation compensation and in nominal rates are generally quite high, independent of the sample, frequency, or measure of inflation compensation. This correlation has varied over time…but the overall picture that emerges is one of a quite strong co-movement. The high correlations suggest that variability in inflation compensation was important for variation in nominal interest rates.”

Inflation expectations and bond yields

“To address the concern that [the close relation between inflation compensation and bond yields] might be driven by movements in risk premia or liquidity factors, I also investigate the behavior of survey-based inflation expectations…Survey expectations of future inflation are available from different sources. In my analysis I focus on the monthly Blue Chip Economic Indicators survey and the quarterly Survey of Professional Forecasters. In addition to near-term inflation expectations, both also include long-term expectations.”

“The correlations between changes in nominal interest rates and survey expectations of inflation are significant for short horizons, and in some cases for long horizons. The magnitudes of the correlations of nominal rates with inflation expectations are similarly high as those with inflation compensation at the same frequencies. This indicates that the co-movement of inflation expectations and nominal interest rates is substantial, and that it is expectations and not risk premia that explain the co-movement with inflation compensation.”

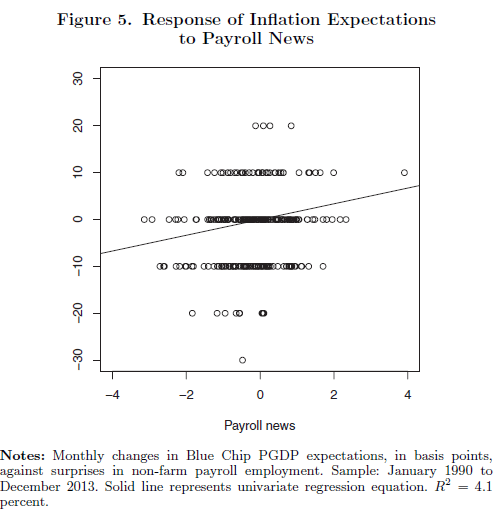

Economic data surprises and inflation compensation and expectations

“The evidence across all three measures of inflation compensation is consistent in that it suggests a high sensitivity of inflation compensation to macroeconomic news, comparable to the response of real rates. Inflation compensation is sensitive to both price-level news and real-side news, and, like nominal rate and real rates, typically responds in a pro-cyclical manner. The sensitivity is evident for both long-term yields and far-ahead forward rates.”

“The paper is the first to estimate the sensitivity of survey-based inflation expectations to macro news… sign. Overall, this regression-based evidence points to significant sensitivity of inflation expectations to macro news, and to an important role of inflation expectations in explaining the sensitivity of nominal rates. While the evidence is stronger for expectations at short horizons, there is also some evidence for the variability of long-term inflation expectations.”

The decline in inflation compensation and risk premia

“Long-term inflation expectations display economically important variation, and that they play a substantial role in explaining the variability of long-term nominal interest rates and their responses to macro news. One consequence of this conclusion is that a better anchoring of long-term inflation expectations, lowering their volatility and sensitivity to macroeconomic news, would likely reduce the variability of long-term interest rates.”

“Toward the end of the sample, correlations [of inflation expectations] with nominal rates decrease significantly…For most series the correlations drop to zero by the end of 2013…The decreasing correlations I have reported tentatively suggest that variation in inflation expectations is starting to become less important.”