A BOJ paper proposes an affine terms structure model for bond yields under consideration of the zero lower bound. It estimates the contribution of [i] expected real rates, [ii] real term premia, [iii] expected inflation rates, and [iv] inflation risk premia. In the U.S. yields have been driven mainly by expected real rates and real term premia in recent years. In Japan inflation expectations and inflation/deflation risk premia have played a greater role.

Imakobu, Kei, and Jouchi Nakajima (2015), “Estimating inflation risk premia from nominal and real yield curves using a shadow-rate model”, Bank of Japan Working Paper Series, No.15-E-1 April 2015 http://www.boj.or.jp/en/research/wps_rev/wps_2015/wp15e01.htm/

On evidence for a decrease in inflation compensation implied in bond yields view post here.

The below are excerpts from the paper. Headings and cursive text have been added.

The model for the analysis

“The affine-type term structure (ATS) model introduced by Duffie and Kan (1996) has become a widely accepted approach to decomposing nominal yields.”

N.B. An affine term structure model is based on two simple ideas. First, bond yields evolve overtime as an “affine” function (constant plus linear coefficients) in a set of stochastic variables. Second, yields at different maturities form an equilibrium that does not allow any market participant to make a profit from arbitrage.

“The standard ATS models are subject to estimation bias due to ignoring the zero lower bound constraint, and could produce misleading results.….[By contrast, an extended ATS model in form of a] shadow-rate term structure (SRTS) models specify a shadow rate that takes both positive and negative values…The nominal short rate is set equal to the shadow rate if the shadow rate is positive and to zero otherwise. This specification allows us to avoid the estimation bias inherent in the ATS model.”

Decomposing government bond yields

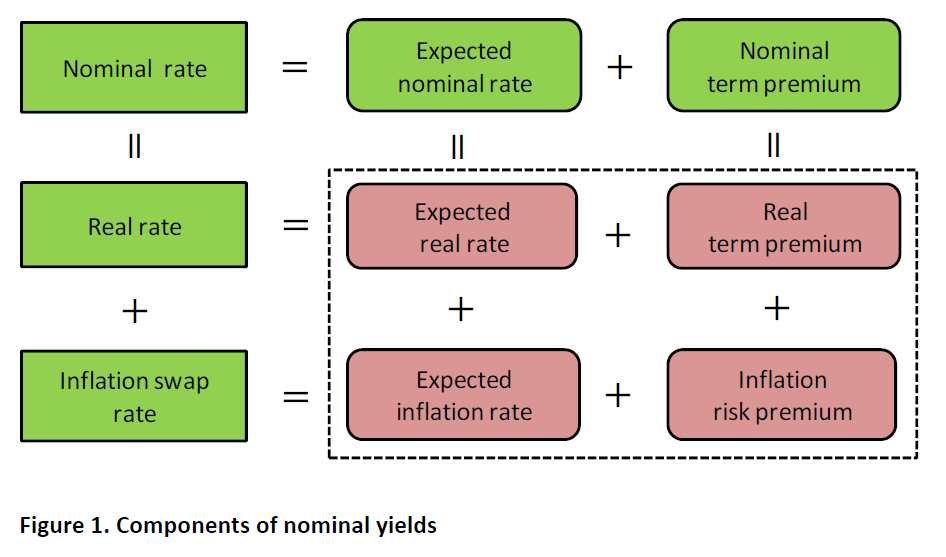

“A nominal bond yield can be decomposed into four components: expected real rate, real term premium, expected inflation, and inflation risk premium. This decomposition has become an accepted practice for measuring the effects of monetary policy.”

“The expected real rate is basically influenced by monetary policy, i.e., both the current policy stance and market participants’ view of how the policy will evolve… The real term premium generally reflects the real-term interest-rate risk – a wide variety of risks other than inflation risks – as well as investors’ preference for safe assets and various other factors including the central banks’ policy actions…We define the inflation components as the difference between the nominal and real yields.”

Interpreting the inflation risk premium

“The inflation risk premium is compensation for real return uncertainty caused by unexpected inflation or deflation. The model-implied inflation risk premium… can take both positive and negative values, depending on the correlation between the real stochastic discount factor and inflation expectations.”

“The real stochastic discount factor, or the pricing kernel, can be interpreted in several ways. One standard interpretation in the literature is that the real stochastic discount factor corresponds to the investors’ marginal rate of substitution as shown in the capital asset pricing model…For example, if inflation rises unexpectedly when the marginal utility is high, the real return for holding nominal bonds falls unexpectedly [N.B.: Marginal utility tends to be high when income or other investment returns are low]. In this case, the nominal bonds are risky assets and bond investors charge a positive premium on the bonds. Conversely, if inflation falls unexpectedly when the marginal utility is high, the investors benefit from holding the nominal bonds. Then, they are willing to pay a premium on the bonds. In this case, the inflation risk premium is negative.”

N.B.: The implication for institutional investors is that inflation premia would be positive if rising inflation was associated with lower returns on global assets. This is predominant when inflation is high and variable and central banks respond strongly to its changes. Inflation premia would be negative if falling inflation was associated with lower returns on global assets. This is more common in times of price stability or in deflation, when financial market returns are dominated by real economic and financial system shocks.

Empirical analysis

“[The empirical analysis] applies to Japan’s and U.S. yield data. The data are monthly series (end-of-month) of nominal and real zero-coupon rates from January 1995 to December 2014. The real zero-coupon rate is given as the difference in the nominal zero-coupon rate from the zero-coupon inflation swap rate… In this analysis, the real yields are only available from April 2007 for Japan, and from January 2005 for the United States, due to data availability of inflation swap rates.”

“As for Japan, the shadow rates are below zero for almost all periods excluding the period from 2006 to 2008, right after the quantitative easing policy ended. This implies that the zero lower bound constraint has been constantly binding to the nominal short rate for these two decades. As for the United States, the shadow rate first turned to negative in 2009, staying below zero since then.”

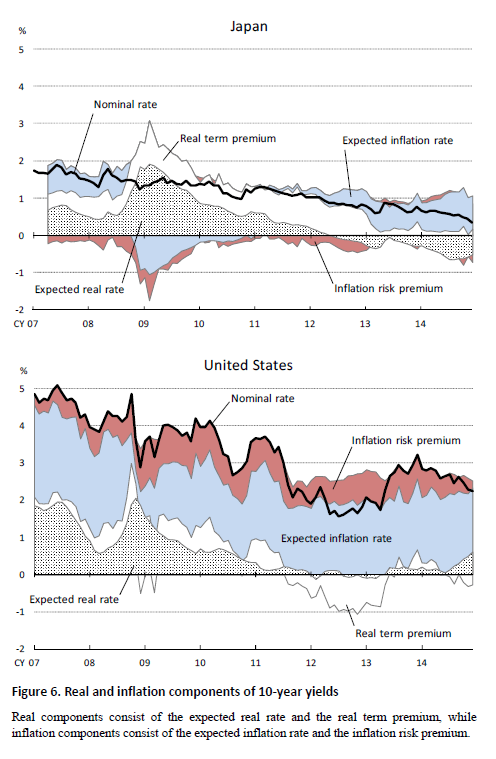

“[The figure below] shows the estimated components of the 10-year JGB and U.S. Treasury yields: expected real rate, real term premium, expected inflation, and inflation risk premium. One of the features common to Japan and the United States is the steady decline in the expected real rate…The low level of the expected real rate, currently negative in Japan, reflects the market participants’ view that monetary policy will remain accommodative for a while.”

“Another feature is the downward move in the real term premium after the Lehman shock. Japan’s real term premium, constantly positive through 2012, dropped sharply to around zero percent in 2013. The U.S. real term premium, though relatively volatile, moved downward and temporarily hit negative levels during the 2011-2013 period….The recent fall in the real term premium mainly reflects the central banks’ large-scale asset purchases, which are in effect through both a scarcity channel and a duration channel by tightening supply-demand conditions in their government bond markets. A decline in future uncertainty, suggested by the historically low volatility of long-term yields, may also contribute to the lower real term premium.”

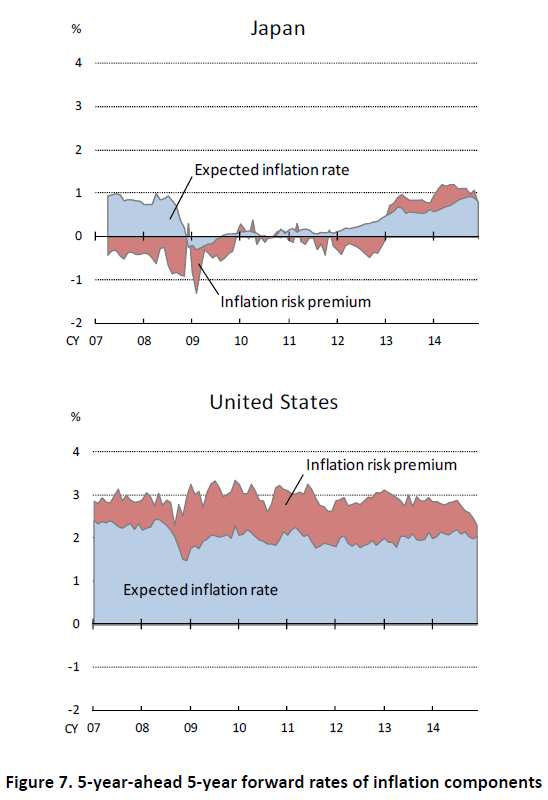

“In the United States, both the expected inflation and the inflation risk premium [5 years-5-years forward] are almost constant in the positive territory, implying that U.S. inflation expectations are more or less anchored.”

“In Japan, the following two changes in the dynamics of inflation expectations have contributed to an upward movement of the inflation components in recent years. First, the 5-year ahead 5-year forward rate of expected inflation remained at almost zero percent after the Lehman shock, but started to increase in 2012. Second, the negative forward rate of the inflation risk premium has disappeared since 2013. Although the expected inflation has not yet reached the Bank of Japan’s price stability target of 2 percent, these two changes imply that market concerns over deflation have subsequently weakened. Our estimates of inflation components closely match the movements in the survey measures of market expectations on future inflation.”