A new McKinsey report estimates that total debt of households, corporates, and governments has expanded 40% since 2007, reaching a total of 286% of GDP last year. Government debt ratios will be hard to contain through fiscal tightening and economic growth alone. China’s non-financial debt has quadrupled, with credit quality critically dependent on the real estate sector.

McKinsey Global Institute, “Debt and (not much) deleveraging”, McKinsey&Company, February 2014.

http://www.mckinsey.com/insights/economic_studies/debt_and_not_much_deleveraging

The below are excerpts from the report. Emphasis and cursive text have been added.

The debt megatrends since 2007

“We examine the evolution of debt and prospects for deleveraging in 22 advanced economies and 25 developing economies. Our research focuses on debt of the ‘real economy’—of households, non‑financial corporations, and governments—and treats financial-sector debt separately.”

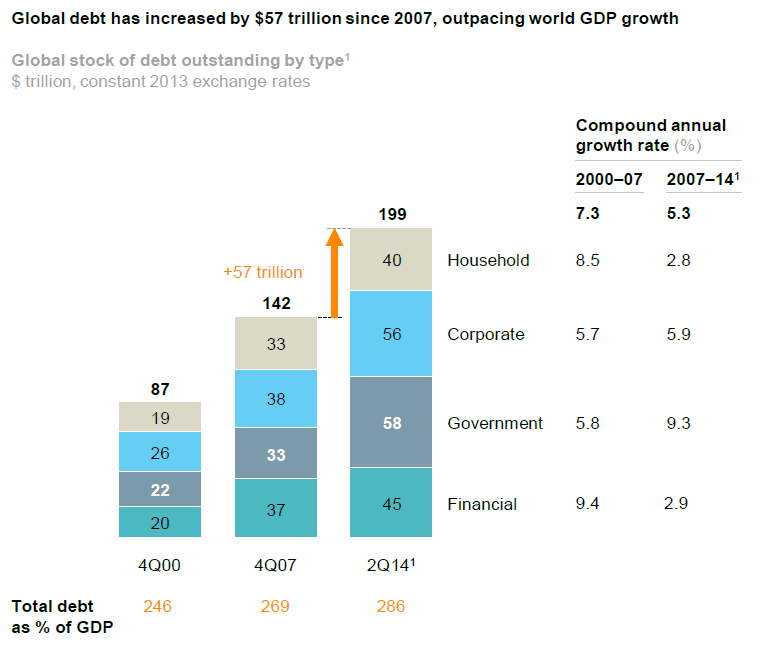

“Total global debt rose by USD57 trillion from the end of 2007 to the second quarter of 2014, reaching USD199 trillion, or 286%of global GDP…Developing economies account for roughly half of the growth…In advanced economies, government debt has soared and private-sector deleveraging has been limited… In a range of countries, including advanced economies in Europe and some Asian countries, total debt now exceeds three times GDP. Japan leads at 400 percent of GDP, followed by Ireland, Singapore, and Portugal, with debts ranging from 350 to 400 percent. Belgium, the Netherlands, Greece, Spain, Sweden, and Denmark all have debt exceeding 300 percent of GDP.”

“Given the magnitude of the 2008 financial crisis, it is a surprise, then, that no major economies and only five developing economies have reduced the ratio of debt to GDP in the “real economy” (households, non‑financial corporations, and governments, and excluding financial-sector debt). In contrast, 14 countries have increased their total debt-to-GDP ratios by more than 50 percentage points.”

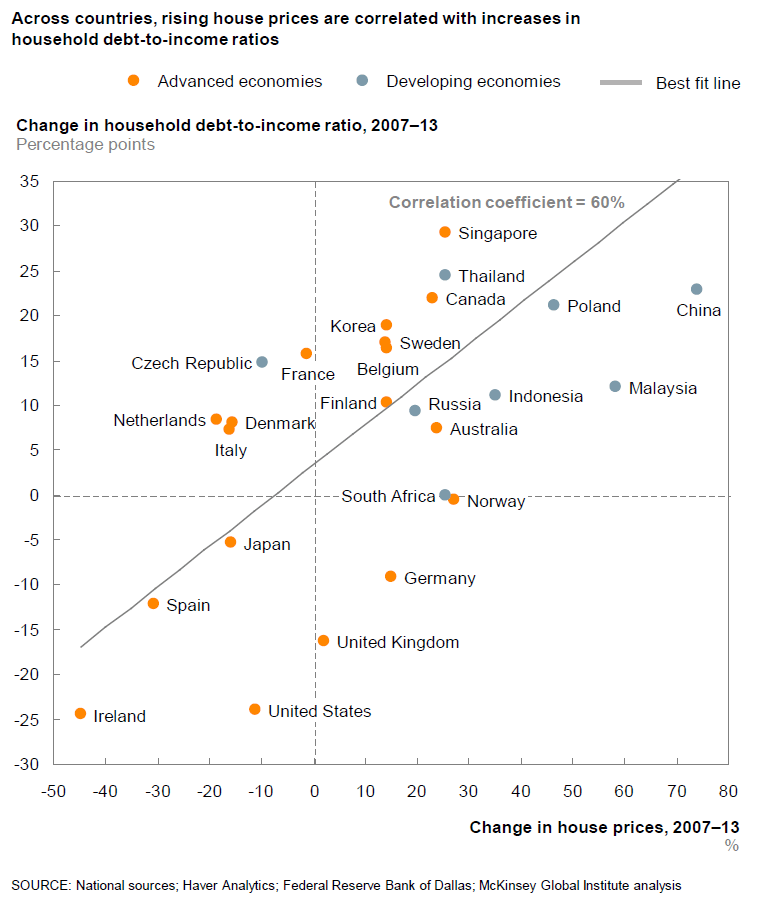

“Despite the tightening of lending standards, household debt relative to income has declined significantly in only five advanced economies—the United States, Ireland, the United Kingdom, Spain, and Germany. The United States and Ireland have achieved the most household deleveraging, using very different mechanisms (default in the United States, and loan modification programs in Ireland). Meanwhile, a number of countries in northern Europe, as well as Canada and Australia, now have larger household debt ratios than existed in the United States or the United Kingdom at the peak of the credit bubble.”

“Financial-sector debt relative to GDP has declined in the United States and a few other crisis countries, and has stabilized in other advanced economies. At the same time, banks have raised capital and reduced leverage. Moreover, the riskiest elements of shadow banking are in decline. For example, the assets of off-balance sheet special-purpose vehicles formed to securitize mortgages and other loans have fallen by USD3 trillion in the United States. Repurchase agreements (repos), collateralized debt obligations, and credit default swaps have declined by 19%, 43%, and 67%, respectively, since 2007.”

“Since 2007, corporate bonds and lending by non‑bank institutions—including insurers, pension funds, leasing programs, and government programs—has accounted for nearly all net new credit for companies, while corporate bank lending has shrunk. The value of corporate bonds outstanding globally has grown by USD4.3 trillion since 2007, compared with USD1.2 trillion from 2000 to 2007… Some specific types of non‑bank credit are growing very rapidly, such as credit funds operated by hedge funds and other alternative asset managers.”

The government debt issue

“Rising government debt (debt of central and local governments, not state-owned enterprises) has been a significant cause of rising global debt since 2007. Government debt grew by USD25 trillion between 2007 and mid-2014, with USD19 trillion of that in advanced economies.”

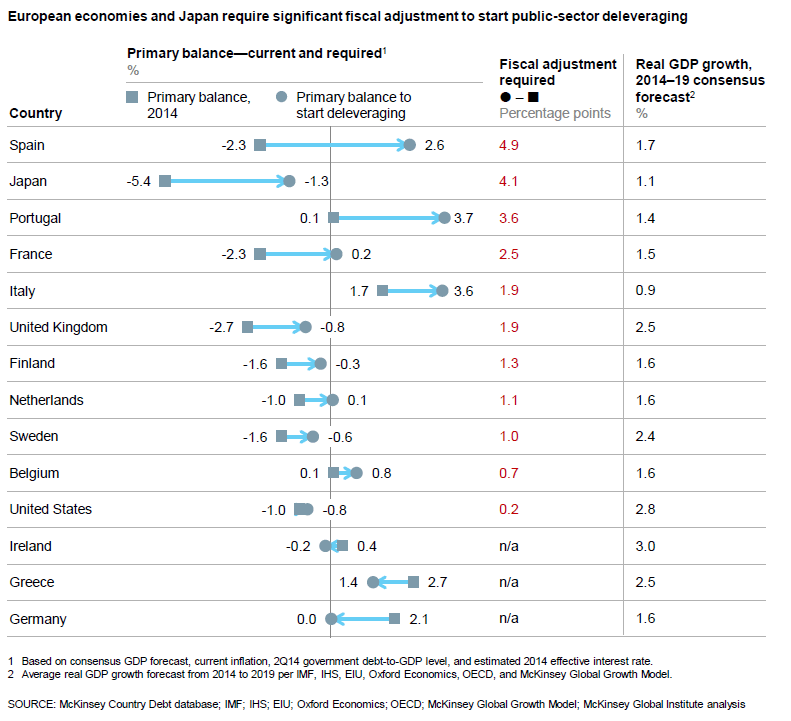

“To reduce their debt-to-GDP ratios, governments need to either run fiscal surpluses large enough to repay debt (reducing the numerator in the ratio) or raise nominal GDP growth (the denominator)… Given current primary fiscal balances, interest rates, inflation, and projected real GDP growth rates over the next five years, we calculate that the ratio of government debt to GDP will continue to grow in many advanced economies, including Japan, the United States, the United Kingdom, and a range of European countries.”

“Debt in some countries would become very large: Japan’s government debt, for instance, could exceed 250 percent of GDP by 2019, up from 234 percent today. A range of European economies are projected to have government debt-to-GDP ratios that exceed 150 percent: Portugal (171 percent), Spain (162 percent), and Italy (151 percent), while Greece’s government debt is projected to be 175 percent of GDP despite the improvement.”

“We calculate that the fiscal adjustment (or improvement in government budget balances) required to start government deleveraging is close to 2 percent of GDP or more in six countries: Spain, Japan, Portugal, France, Italy, and the United Kingdom. Attaining and then sustaining such dramatic changes in fiscal balances would be challenging. Furthermore, efforts to reduce fiscal deficits could be self-defeating, inhibiting the growth that is needed to reduce leverage.”

For government debt issues also view SRSV posts here, here, and here.

The China debt issue

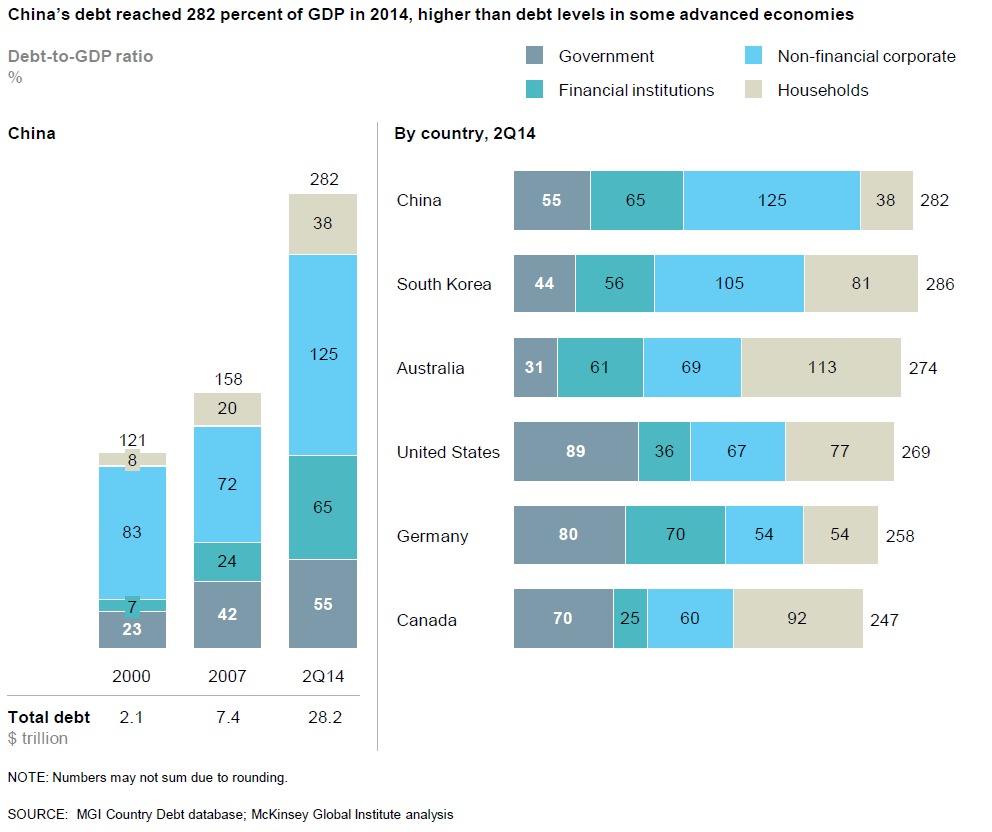

“Fueled by real estate and shadow banking, China’s total debt has quadrupled, rising from USD7 trillion in 2007 to USD28 trillion by mid-2014. At 282 percent of GDP, China’s debt as a share of GDP, while manageable, is larger than that of the United States or Germany. Several factors are worrisome: half of loans are linked directly or indirectly to China’s real estate market, unregulated shadow banking accounts for nearly half of new lending, and the debt of many local governments is likely unsustainable.”

“Loans by shadow banking entities total USD6.5 trillion and account for 30 percent of China’s outstanding debt (excluding the financial sector) and half of new lending. Most of the loans are for the property sector. The main vehicles in shadow banking include trust accounts, which promise wealthy investors high returns; wealth management products marketed to retail customers; entrusted loans made by companies to one another; and an array of financing companies, microcredit institutions, and informal lenders. Both trust accounts and wealth management products are often marketed by banks, creating a false impression that they are guaranteed.”

“A large part of the credit boom in China since 2007 has been related to real estate. New construction, measured by gross floor area, has grown by 9 percent a year since 2008 in Tier 1 cities such as Beijing and Shanghai, by 11 percent in Tier 2 cities, and by 18 percent in Tier 3 cities. Property prices have increased as well, as households have bought homes and invested in real estate to find better returns than bank deposits offer. An index of prices in 40 Chinese cities rose by 60 percent from 2008 to August 2014…We estimate that as much as 45 percent of China’s debt (excluding financial-sector debt), or nearly USD9 trillion, is directly or indirectly related to real estate.”

For China debt problems also view SRSV post here and here.

The consequences

“Business leaders should expect that debt will be a drag on GDP growth and continue to create volatility and fragility in financial markets. Policy makers will need to consider a full range of responses to reduce debt as well as innovations to make debt less risky and make the impact of future crises less catastrophic.”

“Given current growth projections, interest rates, and fiscal balances, government debt is likely to continue to grow. Policy makers, therefore, will need to consider a broader range of actions to stabilize or reduce government debt…With the levels of government debt today, the lack of political will for prolonged austerity in many countries, and the inability to restart economic growth, some countries may have no option but to consider new mechanisms for restructuring sovereign debt. The IMF has proposed reforms to enable sovereign debt restructuring to proceed more efficiently… Another option is to rethink how central bank holdings of government debt are treated in any analysis of debt sustainability. Today, the central banks of the United States, the United Kingdom, and Japan hold 16, 24, and 22 percent, respectively, of government bonds outstanding in their countries. These holdings are largely the result of the quantitative easing… Whether central banks could cancel their government debt holdings is unclear. Any write-down in their value would wipe out the central bank’s capital. While this would have no real economic consequence, it would likely create financial market turmoil.”

“A plausible concern is that the combination of an overextended property sector and unsustainable finances of local governments could result in a wave of loan defaults in China, damaging the regular banking system and potentially creating a wave of losses for investors and companies that have put money into shadow banking vehicles. While this could cause serious damage to the economy, we also find that China’s government has the capacity—if it chooses to use it—to bail out the financial sector even if default rates were to reach crisis levels.”