There is theoretical reason and empirical evidence for a single global financial cycle driving capital flows across a wide range of markets. Federal Reserve decisions are one major cause for this cycle, challenging the independence of monetary policy elsewhere. Catalysts of financial cycles are leveraged investors with Value-at-Risk constraints, such as banks. One consequence is correlated risk across a wide range of leveraged investment strategies.

Miranda-Agrippino, Silvia, and Helene Rey (2014), “World Asset Markets and the Global Financial Cycle”, Working Paper [in progress]

http://www.helenerey.eu/RP.aspx?pid=Working-Papers_en-GB&aid=72802451958_67186463733

Rey, Helene (2013), “Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence”, Paper presented at the 25th Jackson Hole symposium, Wyoming, August 2013.

http://www.helenerey.eu/RP.aspx?pid=Working-Papers_en-GB&aid=84976899_67186463733

The below are excerpts from the papers. Emphasis and cursive text have been added.

Key point

“One global factor explains an important part of the variance of a large cross section of returns of risky assets around the world. This global factor can be interpreted as reflecting the time-varying degree of market wide risk aversion and aggregate volatility…reflecting the investment preferences of leveraged global banks with important capital market operations and that of asset managers such as insurance companies or pension funds.”

Evidence of the power of a global financial factor

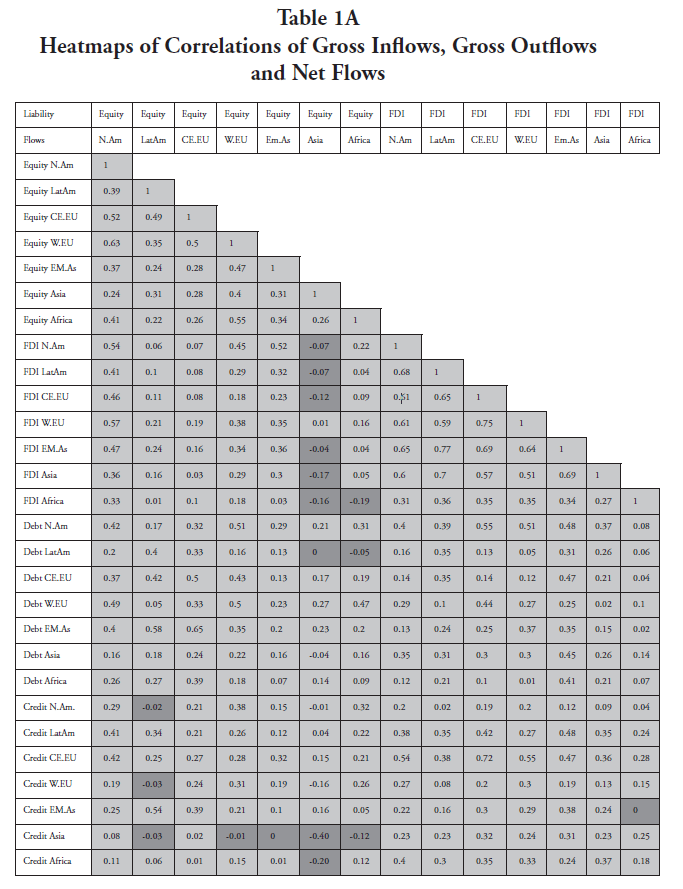

“Table 1a [below] presents a comprehensive heat map of [gross] capital inflows by asset classes into different geographical regions…The data are quarterly from the first quarter of 1990 to the fourth quarter of 2012 and come from the IMF International Financial Statistics…Most types of capital inflows are positively correlated with one another and across regions…The heat map of capital outflows by asset classes…shows an almost equally strong pattern of positive correlations…The commonality is particularly strong for credit and portfolio debt inflows.”

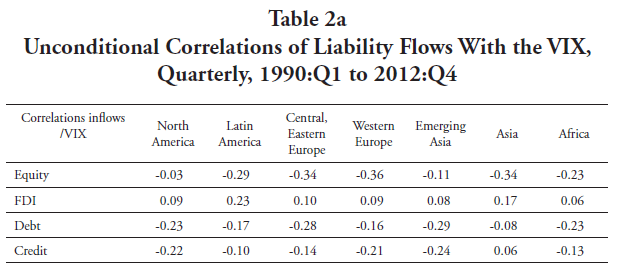

“More recently, several studies have found that movements in the VIX [representing the implied volatility of U.S. equity index options] are strongly associated with capital flows. The VIX is widely seen as a market proxy for risk aversion and uncertainty…Capital inflows are negatively correlated with the VIX, even at a geographically disaggregated level. Overwhelmingly, during tranquil periods characterized by low VIX, when uncertainty and risk aversion are low, capital inflows are larger. The only consistent exceptions are FDI inflows.”

“In all areas of the world, credit growth is negatively linked to the VIX. Correlations tend to be the strongest in North America and Western Europe. Leverage and leverage growth are also negatively related to the VIX in all the main financial centers”

“Using a large cross section of 858 risky asset prices distributed on the five continents, an important part of the variance of risky returns (25%) is explained by one single global factor…This result is remarkable given the size and the heterogeneity of the set…The high degree of correlation of the global factor with the VIX is striking…It can be understood as reflecting the joint evolution of the effective risk appetite of the market as well as realized market volatility. In turn the effective risk appetite of the market can be empirically related to the leverage of a subset of financial market intermediaries whose investment strategy is well approximated by a VaR constraint.”

The catalysts of the global financial cycle

“In a context in which global banks are risk neutral and subject to a VaR [Value-at-Risk] constraint…all the times then banks will adjust their positions depending on the perceived risk so that their VaR does not change; this mechanism implies that even when risk is low – or perceived as such – they will increase their exposure in a way that ensures their probability of default remains unchanged…They actively manage their leverage by adjusting their demand for assets in a way that makes leverage pro-cyclical or, in other words, increasing in the size of their balance sheets… [Empirical] results suggest that global banks have gone before the crisis through a phase in which they were building up leverage and loading up on systemic risk, getting high returns and then reverted abruptly after the crisis.”

“Global banks through leveraging and deleveraging effectively influence funding conditions for the entire financial system and ultimately for the broader international economy…In particular, easier funding or particularly favorable credit conditions can translate into an increase in credit growth, reduction of risk premia and run up of asset prices.”

On the pro-cyclicality of shadow banking view post here

The struggle with independent monetary policy

“US monetary policy has a significant effect on the leverage of US and European investors (particularly European and UK capital markets banks), on cross border credit flows and on credit growth worldwide. It also has a powerful effect on the global factor, the risk premium and the term spread….This points towards important effects of US monetary policy on the world financial system and the global financial cycle: US monetary policy contributes to set the tune for credit conditions worldwide in terms of volumes and prices.”

“Macroprudential policies are necessary to restore monetary policy independence for the non-central countries. They can substitute for capital controls, although if they are not sufficient, capital controls must also be considered.”