Bank of Canada has assembled a new broad database on global public debt default. It shows that after sovereign delinquency had exceeded 5% of outstanding debt in the 1980s, it declined alongside falling interest rates to below 1% in the 2000s and has remained low despite the global financial and euro sovereign crises. In a longer (200 year) context sovereign default ratios have moved in long cycles, each stretching over several decades.

“Introducing a New Database of Sovereign Defaults”, David T. Beers and Jean-Sébastien Nadeau

Bank of Canada, Technical Report No. 101, 25 February 2014

http://www.bankofcanada.ca/wp-content/uploads/2014/02/tr101.pdf

The below are excerpts from the report. Emphasis and cursive text has been added.

The new database

“The Bank of Canada’s Credit Rating Assessment Group (CRAG) has developed a comprehensive database of sovereign defaults posted on the Bank of Canada’s website. Our database draws on previously published data sets compiled by various official and private sector sources. It combines elements of these, together with new information, to develop estimates of stocks of government obligations in default, including bonds and other marketable securities, bank loans, and official loans in default, valued in U.S. dollars, for the years 1975 to 2013 on both a country-by-country and a global basis.”

“An important reason is that there is no single internationally recognized definition of what constitutes a sovereign default….We consider that a default has occurred when debt service is not paid on the due date (or within a specified grace period), payments are not made within the time frame specified under a guarantee, or, absent an outright payment default, in any of the following circumstances where creditors incur material economic losses on the sovereign debt they hold:

- agreements between governments and creditors that reduce interest rates and/or extend maturities on outstanding debt;

- government exchange offers to creditors where existing debt is swapped for new debt on less-economic terms;

- government purchases of debt at substantial discounts to par;

- government redenomination of foreign currency debt into new local currency obligations on less-economic terms;

- swaps of sovereign debt for equity (usually relating to privatization programs) on less-economic terms; or,

- conversion of central bank notes into new currency of less-than-equivalent face value.”

A condensed history

“Cross-border bond financing for governments emerged in the 1820s, when newly independent states in Latin America and other regions, as well as some longer-established sovereigns, began issuing bonds denominated in foreign currency in European financial centres. Defaults soon followed on a substantial scale and persisted well into the 20th century.”

“After the Second World War, owing to pervasive national controls on capital movements, cross-border bond issuance by governments fell to low levels, as did defaults, and both remained low over nearly four decades. For a relatively brief period, in the 1970s and 1980s, foreign currency-denominated loans by banks eclipsed bonds in importance. Many developing and East European countries defaulted on bank loans in the 1980s and 1990s, leading to creditor losses. The banks’ subsequent exit from this business laid the groundwork for low- and middle-income sovereigns to regain access to cross-border bond markets in the 1990s, which continues to this day. Since then, bond defaults have risen again but remain well below their earlier historical peaks.”

“Three peak default periods stand out – between the 1830s and 1850s, when default rates exceeded 25 per cent; in the 1870s, when default rates averaged 18 per cent; and in the 1930s, when they reached 21 per cent. Of note, too, is the sharp decline in bond defaults after the Second World War that persisted through the 1980s. The resolution of many prewar bond defaults was the main driver of the fall in the default rate. At the same time, the fragmentation of the early post-Second World War cross-border financial markets limited bond market access to only the most creditworthy borrowers, and so defaults on new issues were low.”

“After 1945, lending to governments by the IMF and other newly established MLIs [multilateral lending institutions] quickly gained prominence…They increasingly targeted loans to developing country governments on concessional terms, and initially defaults on official loans were low….By the 1980s, however, the sharp rise in sovereign defaults on bank loans…was accompanied by growing defaults on loans from official creditors…official and private debt in default together amounted to nearly USD400 billion by 1990, with official debt accounting for about 11 per cent of the total. By 1995, the share of official creditor debt exceeded 40 per cent. The factors driving both bank loans and official loans into default were often closely linked, owing to the adverse fiscal impact in many countries from the spike in world oil prices and in U.S. short-term interest rates. The latter directly impacted the cost of syndicated bank loans contracted by many sovereign borrowers and helped ratchet up the real burden of their public debt.”

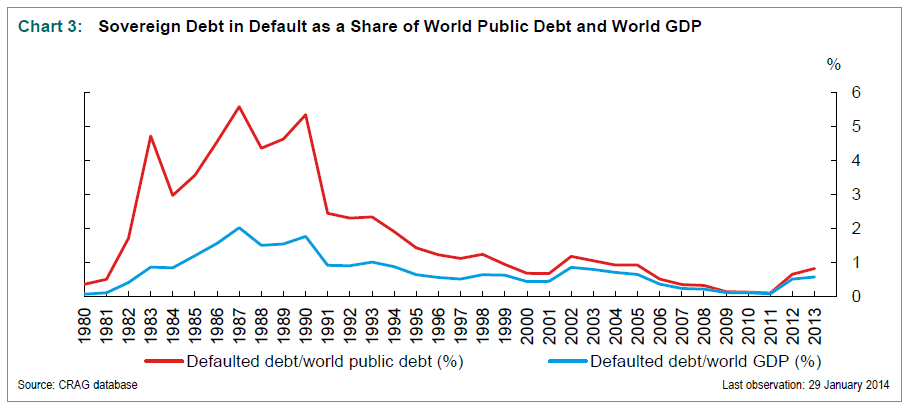

“Chart 3 scales the nominal value of debt in default by nominal global public debt and GDP to obtain a more macroeconomic perspective on the relative importance of sovereign defaults. At the start of the 1980s, defaults had minimal impact globally. However, by the middle of the decade [1980s], when fiscal stresses affecting low- and middle-income countries were most severe, the sovereign debt that defaulted, was restructured, and in many cases was ultimately written down peaked at just over 5 per cent of global public debt. The increase was milder in terms of global GDP, rising from near zero to about 2 per cent…the global footprint left by these debt workouts has since faded, despite Argentina’s big default in 2000 and, most recently, the restructurings of sovereign bonds and official loans in the euro area.”