There is a strong logical and empirical link between the U.S. Treasury yield curve and long-term economic trends, particularly expected inflation and the equilibrium short-term real interest rate. Accounting for variations in these two trends allows isolating cyclical factors in a non-arbitrage term structure model. Put simply, interest rates mean-revert to a ‘shifting endpoint’ that is driven by macroeconomics. According to new research, term structure models that include long-term macro trends substantially improve yield forecasts for the medium term as well as predictions of bond excess returns.

The post ties in with SRSV’s lecture on systemic trading value through researching macro trends.

The below are excerpts from the paper. Emphasis and cursive text have been added.

The gist

“[We provide] evidence that interest rates and risk pricing are substantially driven by time variation in the trend in inflation and the equilibrium real rate of interest…Our results confirm the predictions of no-arbitrage theory for the links between macroeconomic trends and the yield curve, and they demonstrate that these links are quantitatively important.”

“Accounting for fluctuations in both the equilibrium real short-term interest rate and expected future inflation substantially increases the accuracy of long-range interest rate forecasts, helps predict excess bond returns, improves estimates of the term premium in long-term interest rates, and captures a substantial share of interest rate variability at low frequencies.”

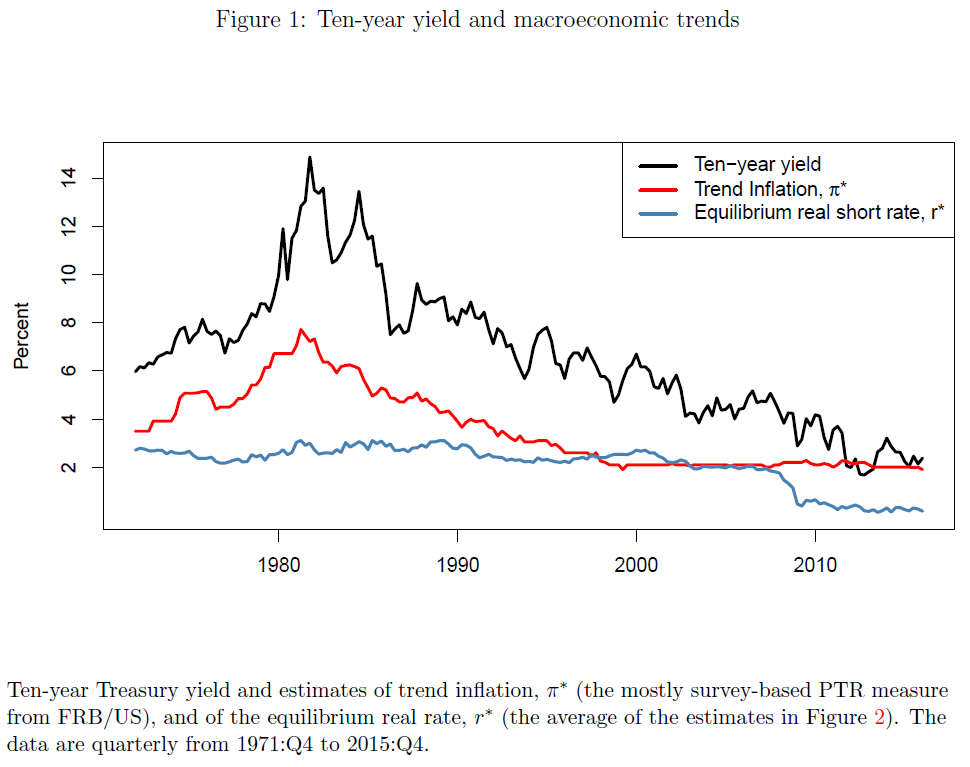

“Remarkably, thus far, there has been very little work addressing the effects of changes in the equilibrium real short-term interest rate on the dynamics of the term structure of interest rates…Long-term nominal interest rates reflect expectations of future inflation and real short rates…subject to a risk adjustment…A useful illustration of the potential importance of accounting for the equilibrium real rate is provided in the figure below…Much of the recent downtrend in yields seems to reflect a lower equilibrium real short-term interest rate.”

“Our empirical evidence linking inflation and real rate trends to the yield curve and risk pricing has far-reaching implications for modeling of interest rates and bond risk premia. In order to accurately capture interest rate dynamics, both structural and reduced-form models of the yield curve should allow for slow-moving trend components. The common approach of specifying a stationary system for the term structure of interest rates with constant means for the risk factors is problematic.”

The model

“Our theoretical framework is a stylized affine term structure model for real and nominal yields that demonstrates how, under absence of arbitrage, changes in the inflation trend and the equilibrium real short rate affect interest rates…We model inflation as the sum of trend, cycle, and noise components…The one-period real rate also has trend and stationary components, respectively, the equilibrium real rate and the cyclical real-rate gap…The final state variable determining interest rates is a risk price factor, which follows an independent autoregressive process…The model is completed by a specification for the log real stochastic discount factor…for which we choose the usual essentially affine form.”

“The trend components, expected long-term inflation and the equilibrium real short-term interest rate, naturally act as level factors by affecting yields of all maturities equally. The cyclical components are slope factors as they affect short-term yields more strongly than long-term yields, and their loadings approach zero for large maturities. The risk premium factor affects long-term yields more strongly than short-term yields.”

“The model has several predictions about the relationship between interest rates and the two macroeconomic trends…

- A first straightforward prediction is that for any yield maturity, the detrended yield [subtracting expected long-term inflation and the equilibrium real short-term interest rate] will be much less persistent than the yield itself. The difference in persistence is particularly pronounced for long-term yields or forward rates, which place a heavy weight on the trend components…Interest rates mean-revert to a ‘shifting endpoint’ that is driven by both macroeconomic trends…

- The fact that interest rates do not have a constant mean but contain the stochastic trend also has important implications for yield forecasts…In particular, long-range forecasts that account for the equilibrium nominal short rate should improve upon the common forecast benchmark of a random walk…

- A third area in which macro trends may be empirically relevant is for the prediction of excess bond returns…Detrending interest rates with inflation helps estimate bond risk premia…Therefore, our model’s prediction is that including [macro trends] should improve the predictive power of excess return regressions and the estimation of bond risk premia…

- Finally, the model predicts that macroeconomic trends should play a particularly important role in accounting for interest rate changes at low frequencies. The trend components are highly persistent, so while their influence can be obscured by transitory volatility at higher frequencies, they should key drivers of interest rate changes over longer intervals (e.g., over several years or more). This pattern implies that variance ratios of changes in the trend components relative to changes in interest rates should exhibit a pronounced tendency to rise with the span of the changes.”

The empirical analysis

“Our data set is quarterly and extends from 1971:Q4 to 2015:Q4. The interest rate data are end-of-quarter zero-coupon [U.S.] Treasury yields…with maturities from one to 15 years. We augment these data with three- and six-month Treasury bill rates.”

“For measuring the macroeconomic trends, we simply take existing estimates from the macroeconomics literature. Our goal is to assess whether such off-the-shelf measures can provide evidence linking the inflation and real rate trends to the yield curve and risk pricing…

- For trend inflation…we employ a well-known survey-based measure, namely, the Federal Reserve’s research series on the perceived inflation target rate…It measures long-run expectations of infl ation in the price index of personal consumption expenditure (PCE)…

- [As] macro-based estimation of the equilibrium real interest rate [we] aggregate and smooth the information from three specific modeling strategies…[and] take their average…the model of Laubach and Williams (2003), in which the unobserved natural rate is inferred from macroeconomic data using a simple structural specification and the Kalman filter….the estimates of Lubik and Matthes (2015), who employ a time-varying parameter VAR model, and Kiley (2015), who augments the Laubach-Williams model with credit spreads.”

On the estimation of the equilibrium real interest rate view post here.

The findings

“As a first test, we document that time variation in both expected long-term inflation and the equilibrium real short-term interest rate is responsible for most of the persistence in yields. While interest rates themselves are extremely persistent, the difference between long-term interest rates and the equilibrium nominal short rate…exhibits quick mean reversion. Furthermore, regressions of long-term yields on the macroeconomic trends recover the unit coefficients predicted by our theoretical model…The trend components of inflation and the real rate are related to interest rates exactly as standard finance theory predicts.”

“Second, we show that accounting for both macroeconomic trends leads to substantial improvements in interest rate forecast accuracy at medium and long forecast horizons relative to the usual…forecasting benchmark…We document that, relative to the random walk alternative, the improvements in forecast accuracy from including the trend components are both economically and statistically significant.”

“Third, accounting for a time-varying equilibrium real short-term interest rate is important for understanding return predictability and estimating bond risk premia…[Previous academic work presented] strong evidence for the predictive power of the inflation trend for excess bond returns, which suggests that incorporating the inflation trend is important to understand the risk premium/expectations hypothesis decomposition…we extend the results…by introducing shifts in the equilibrium real interest rate into the prediction of risk premiums, and we find substantial improvements from incorporating the equilibrium real short-term interest rate in predicting excess bond returns.”

“As a final avenue of empirical examination, we compare the variance of changes in the trend components of inflation and real rates to the variance of interest rate changes at different frequencies…A large share of the interest rate variability faced by investors over longer holding periods was due to changes in the macroeconomic trend components of nominal yields.”