The variance risk premium is paid by risk-averse investors to hedge against variations in future realized volatility. Empirical evidence and intuition suggest that equity markets indeed pay over the odds for downside risk in mark-to-market variations but accept a discount for upside risk. The highest premium is paid for downside skewness risk. These forms of variance risk premia have been significant predictors of U.S. equity returns.

Feunou, Bruno, Mohammad R. Jahan-Parvar and Cedric Okou (2015), “Downside Variance Risk Premium”, Finance and Economics Discussion Series, Divisions of Research & Statistics and Monetary Affairs, Federal Reserve Board, 2015-020

http://www.federalreserve.gov/econresdata/feds/2015/files/2015020pap.pdf

On the variance risk premium in FX markets see post here and here.

On the role of risk aversion and risk perceptions for predicting equity returns see post here and here.

The below are excerpts from the paper. Emphasis and cursive text have been added.

What is a variance risk premium?

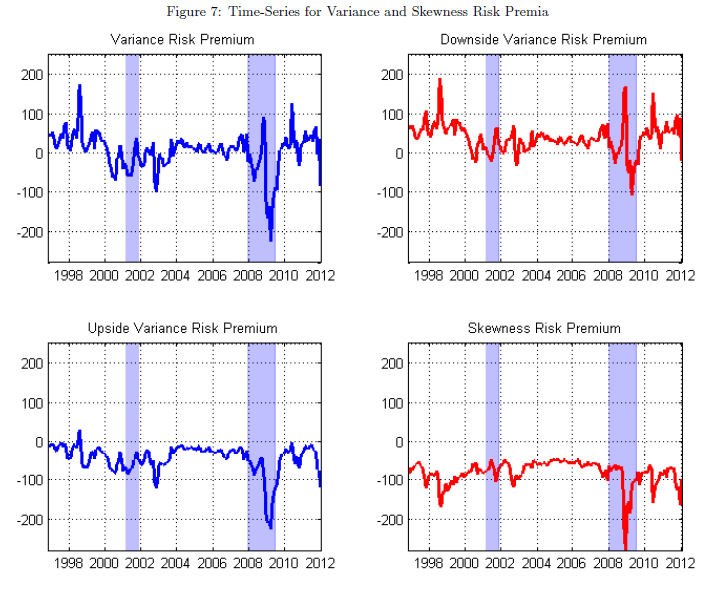

“We characterize the variance risk premium through premia accrued to bearing upside and downside variance risks…A number of recent studies have…argued that the variance risk premium – the difference between option-implied and realized variance – yields superior forecasts for stock market returns over shorter, within-year horizons (typically one quarter ahead)… the variance risk premium explains a nontrivial fraction of the time-series variation in aggregate stock market returns, and that high (low) variance risk premia predict high (low) future returns.”

“The variance risk premium can be interpreted as the premium a market participant is willing to pay to hedge against variation in future realized volatilities. It is expected to be positive because of the intuition that risk-averse investors dislike large swings in volatility, especially in ‘bad times’…The variance risk premium is in general positive and proportional to the volatility of volatility.”

“Intuitively, the variance risk premium proxies the premium associated with the volatility of volatility, which not only reflects how future random returns vary, but also assesses fluctuations in the tail thickness of the future returns distribution.”

What is the downside variance premium?

“We have decomposed the celebrated variance risk premium…to show that its prediction power stems from the downside variance risk premium embedded in this measure. The downside variance risk premium [is] the difference between option-implied, risk-neutral expectations of market downside volatility [which incorporate risk premia] and historical, realized downside variances.”

“We decompose equity price changes into positive and negative returns…We construct the realized variance…of intraday returns observed on that day. We add the squared overnight log-return…To build the risk-neutral expectation of realized variance [we use] prices of European put and call options…We build the variance risk premium…as the difference between option-implied and realized variances. Alternatively, these two components could be viewed as variances under risk-neutral and physical measures, respectively.”

“Our empirical analysis is based on the S&P 500 composite index as a proxy for the aggregate market portfolio. Since our study requires reliable high-frequency data and option-implied volatilities, our sample spans the September 1996 to December 2010 period.”

What is the skewness risk premium?

“To build [a] measure of skewness…we simply subtract downside variance from upside semi-variance…We introduce the notion of a skewness risk premium, closely resembling the variance risk premium. It can be shown that the skewness risk premium is defined as the difference between risk neutral and objective expectations of the realized skewness.”

How do downside variance risk and skewness risk premia predict equity returns?

“We…show empirically how the stylized facts documented in the variance risk premium literature are driven almost entirely by the contribution of the downside variance risk premium, the difference between realized and risk-neutral semi-variances extracted from high frequency data.”

“We find that on average…over 80% of the variance risk premium is compensation for bearing changes in downside risk. In addition, we show there is a contribution of the skewness risk premium to the predictability of returns which takes effect beyond the one-quarter-ahead window documented [for the variance risk premium]…The skewness risk premium performs well for intermediate prediction steps beyond the reach of short-run predictor such as downside variance risk or variance risk premia and long-term predictors such as price-dividend or price-earnings ratios alike.

“We show that the prediction power of the downside variance risk premium and the skewness risk premium increases over the term structure of equity returns. In addition, through extensive robustness testing, we show that this result is robust to the inclusion of a wide variety of common pricing factors. This leads to the conclusion that the in-sample predictability of aggregate returns by downside risk and skewness measures introduced here is independent from other common pricing ratios such as the price-dividend ratio, price-earnings ratio, or default spread.”

Why do downside variance risk and skewness risk premia predict equity returns?

“These observations boil down to a simple intuition: risk-averse investors ask for a premium to face risks they do not like while they are willing to pay for exposure to favorable uncertainties, risks they like…We highlight the inherent asymmetry in responses of market participants to negative and positive market outcomes.”

“There are good and bad uncertainties. On one hand, market participants like good uncertainty when returns are positive, as it signals the potential of earning an even higher return. In other words, risk-averse agents like upside variations, and are willing to pay to be exposed to fluctuations in the upside variance. This argument should induce a negative expected value for the upside variance risk premium. [Indeed, empirically] the average upside premium is about -4.41%…and usually negative through our sample period. On the other hand, investors dislike bad uncertainty (when returns are negative), as it increases the likelihood of losses. Because risk averse agents dislike downside variations, they are willing to pay a premium to hedge against fluctuations in future downside variances. Therefore, the downside variance risk premium is expected to be positive most of the time. These intuitions are supported by the empirical evidence…where the average downside variance premium is about 3.4%, and…usually positive.”

“Building on the same intuition, the sign of the skewness risk premium stems from the expected behavior of the two components of the variance risk premium…the average skewness risk premium is -7.8%. Alternatively, this negative sign may be interpreted as follows: market participants prefer higher skewness, and would like to be exposed to variations in future skewness.”

“Our study is also related to the recent macro-finance literature which emphasizes the importance of higher-order risk attitudes such as prudence – a precautionary behavior which characterizes the aversion towards downside risk – in the determination of equilibrium asset prices.”