A new IMF policy paper defines global liquidity as the ease of funding in global financial markets. The concept is useful for understanding the commonality in global financial conditions, with four large financial centers dominating the world’s institutional funding. In the 2000s banks have been the main conduit of financial shock propagation, but asset managers may play a greater role in the 2010s (see also posts here, here and here).

“Global Liquidity – Issues for Surveillance”, IMF Policy Paper, March 2014

http://www.imf.org/external/np/pp/eng/2014/031114.pdf

The below are excerpts from the paper. Emphasis and cursive text has been added.

Useful definitions

“The expression ‘global liquidity’ is commonly used to refer to the ‘ease of funding’ in global financial markets. It is manifest in the extent to which borrowing constraints are binding in accessing international funding and can be captured in how conditions in financial centers – systemic, reserve currency economies – are transmitted to other financially open economies through capital flows. As it is often identified both with conditions prevailing in major financial markets and intermediaries, and monetary policy conditions, it lies at the intersection of microeconomic, financial, regulatory and macroeconomic factors.”

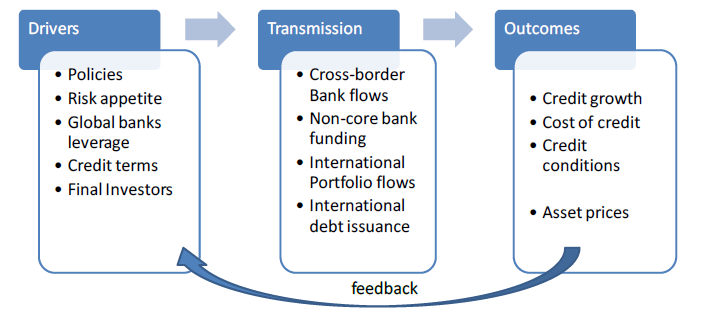

“Consistent with this conceptualization of global liquidity, one can distinguish between drivers, transmission channels, and financial conditions outcomes. In this framing, ease of global finance is driven by conditions prevailing in major financial markets, is transmitted internationally by globally operating financial intermediaries and activities in international financial markets, and together with country-specific factors, leads to local financial conditions outcomes.”

Evidence of commonality in global financial conditions

“There is ample evidence that financial shocks propagate internationally, generating positive and negative spillovers (IMF Spillover reports, 2011-13). Typically such financial shock transmission is defined as co-movements in asset prices and quantities that go beyond what would appear to be justified by economic fundamentals alone.”

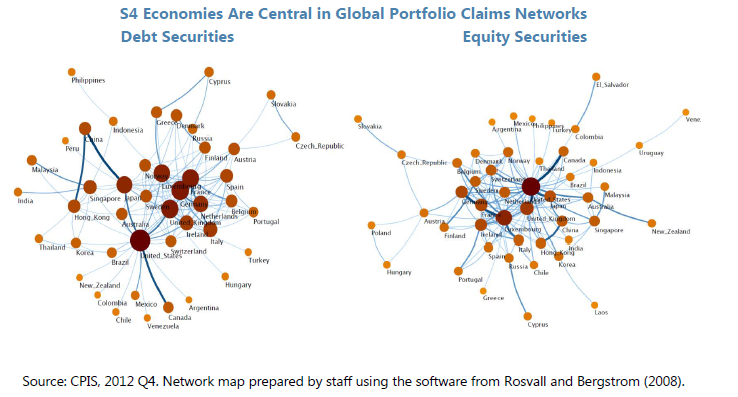

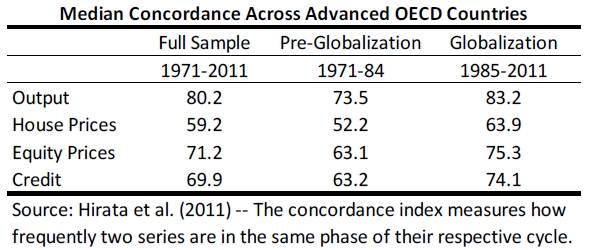

“The increased synchronization of fluctuations in credit and asset prices has been empirically documented. Across advanced economies in particular, synchronicity of credit cycles is high, with some increase over time…While the international financial conditions seems to be driven by changing conditions in financial centers (in particular the four globally systemic economies – Euro area, Japan, the United States, and the United Kingdom, or “S4”), and correlations are higher across advanced economies, co-movement extends to many emerging markets.”

Causes of commonality in global financial conditions

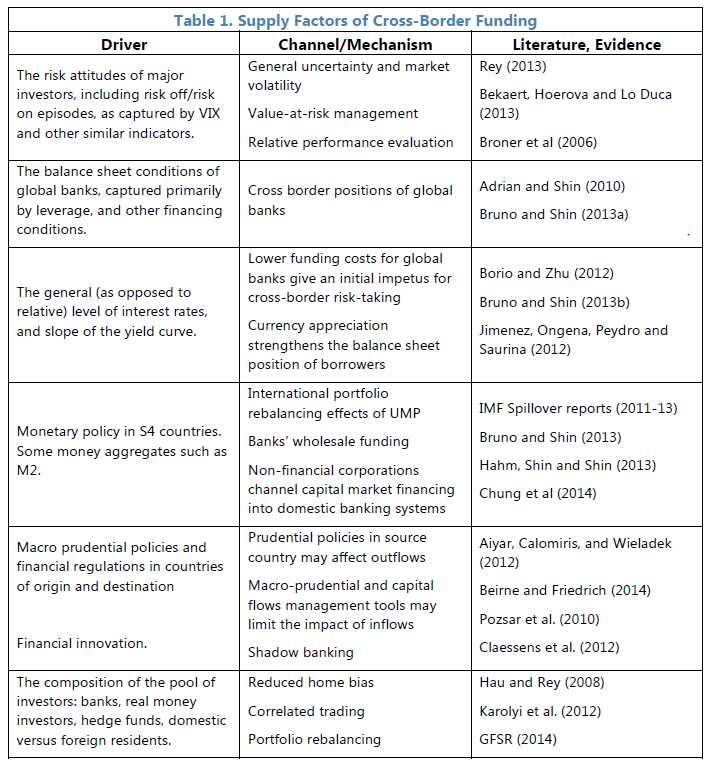

“The fast growth of cross-border bank funding was a key feature of the pre-crisis period and its subsequent reversal of the post-crisis period. BIS international banking statistics show the predominance of a few advanced economies in international bank lending and borrowing.”

“Another channel through which liquidity conditions in financial centers can be transmitted globally is via international bond and equity portfolio flows. In recent years, asset management firms have significantly expanded their global presence, especially in bond markets. In fact, since 2008, the fraction of bond markets under management by mutual funds has increased almost fivefold in emerging markets (view post here) and threefold in advanced economies…The importance of global factors for portfolio flows relates to the centrality of the S4 financial systems in these markets…The centrality of S4 economies in these networks reflects not only their size, but also the extent to which their financial systems serve as conduits in the intermediation of global flows.”