The shadow banking system creates money or money-like claims mainly through repurchase operations: cash managers “park” funds through short-term secured lending, while asset managers borrow against their securities to gain leverage. Large institutions have few alternatives to collateralized lending for cash management. Institutional cash pools and “shadow money” have been expanding rapidly over the past decade.

Poszar, Zoltan (2014), “Shadow Banking: The Money View”, Office of Financial Research, Working Paper, July 2, 2014

http://financialresearch.gov/working-papers/files/OFRwp2014-04_Pozsar_ShadowBankingTheMoneyView.pdf

On the size and risks of shadow banking also view posts here and here.

The below are excerpts from the paper. Headings and cursive text have been added.

Some general points on money

“Money is usually defined from a functional perspective as a ‘unit of account, store of value and medium of exchange.’ However…the quintessential attribute [is]…that money always trades at par on demand.”

“Overnight repos and constant NAV shares [of money market funds] are different…[from] demand deposits [because] they cannot be used for settlement purposes. But they are still considered money because they can be traded for a demand deposit at par on demand. In other words, they are convertible into payments system money, that is, cash, in the form of a demand deposit, which can then be used for settlement purposes. From the perspective of the holders of repos and constant NAV money fund shares the plumbing behind how these claims are converted into cash for settlement and transaction purposes does not matter as much as the price (par) at which they get converted into cash relative to par.”

“Money claims with stated maturities longer than overnight but less than a year are money-like claims. Money-like claims offer par at maturity (in the near-term) but not on demand, and in case one needs to convert them into payment systems money before maturity, they are breakable at a penalty or negotiable at prices normally very close to par.”

Institutional cash pools

“There are four categories of institutional cash pools: (1) the liquidity tranche of FX reserves; (2) the cash balances of global corporations; (3) the centrally managed cash balances of institutional investors and the largest asset managers; and (4) the cash collateral reinvestment accounts of securities lenders. In the aggregate, cash pools had at least USD6 trillion in cash under management at the end of 2013.”

“For [institutional] cash pools, money begins where M2 ends and because of a systemic shortage of safe, short-term, public assets, the bulk of cash pools are constrained to be invested in private money claims with some degree of credit risk — not out of choice, but for a lack of better alternatives…As the crisis has shown, intra-system holdings of uninsured money market instruments can pose threats to financial stability. Institutional cash pools hold money claims mostly for portfolio management reasons and because they are too large to be eligible for deposit insurance, their focus is on money claims’ safety.”

“Uninsured deposits are nothing more than unsecured and undiversified private credit claims (essentially, private bills) that in some states of the world may be worse credits than repos (which are secured claims) or prime money funds (which are backed by diversified portfolios of unsecured claims). In sum, without government insurance, deposits fall from the very top to the very bottom of the hierarchy of money.”

“Institutional cash pools are managed by cash portfolio managers (cash PMs) whose mandate is ‘do not lose.’ This mandate limits cash PMs to invest net payment surpluses in safe assets, or more precisely, safe, short-term assets with maturities ranging from overnight up to a year (that is, money and money-like claims) but usually not beyond.”

“Term cash balances can be invested in volume only in term repos collateralized by public or private securities and (depending on cash PMs’ appetite for safety versus yield) unsecured credit instruments such as uninsured certificates of deposit (CDs) and commercial paper (CP).”

Money creation through dealers and repos

“There are four core institutions engaged in the issuance of money claims in the modern financial ecosystem: the central bank, banks (small and large), dealer banks and money market funds. These institutions issue four core types of money claims. The central bank issues reserves. Banks issue deposits. Dealer banks issue repos. Money funds issue constant net asset value (NAV) shares.”

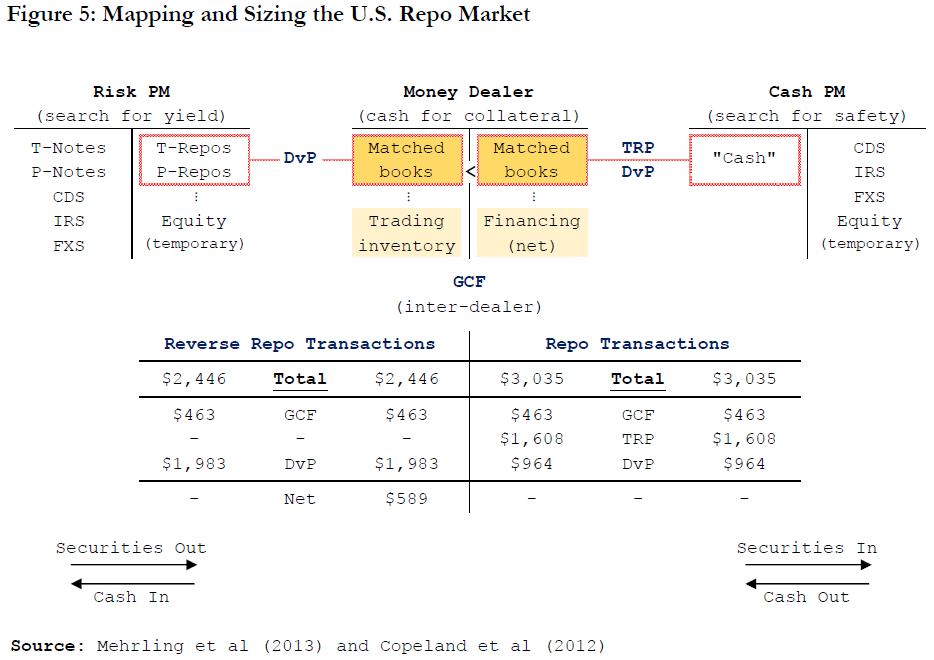

“Dealers are unique among core intermediaries. Unlike banks and money funds, dealers conduct money dealing not only with other intermediaries but also the buyside. Effectively, they are the primary source of funding for the entire spectrum of levered investment strategies in the asset management complex. Dealers are also the primary source of derivative trades. Dealer banks emerged as intermediaries between two types of asset managers: cash pools searching for safety via collateralized cash investments and levered portfolio managers searching for yield via funded securities portfolios and derivatives.”

“We can collectively think of buy-side customers that use repo as risk portfolio managers…Their unifying mandate is to ‘beat the benchmark’. What sets risk PMs apart from traditional, long-only investment managers is their ability to use leverage. Risk PMs may be hedge funds or any investment vehicle (such as an absolute return bond fund or unconstrained bond fund) or separate account with a mandate that allows the use of at least some leverage.”

“Bilateral repos and dealers play a role in facilitating all…forms of leverage.

- Consider the case of cash for funding. A risk PM — for example a mortgage REIT (or MREIT) — decides to go long a portfolio of agency RMBS with 10 percent equity down and the rest of the position funded. The equity is the M-REIT’s assets under management, and the M-REIT’s goal is to beat its benchmark using leverage through funding.

- Consider the case of cash for shorting. Every time a security gets shorted, a risk PM — a short seller — a dealer and a securities lender (in either an agent or a principal role) are involved…The short-seller posts cash as collateral (so-called initial margin) with a dealer to borrow the security in question.

- Consider the case of cash for margining… The risk PM’s choice of instruments for this tactical hedge are swaps executed with dealers’ swap desks.”

“Dealers are thus intermediaries between risk PMs and cash PMs…Risk PMs repo securities out and cash in (to get funding, to lend securities, to raise cash to pay margin on out of the money derivative positions), and on the flipside, cash PMs repo securities in and cash out (to lend cash on a secured basis or to build a short position in specific securities).”

“Asset managers’ money demand is not driven by transaction needs in the real economy but in the financial economy: in this sense, repo-based money dealing activities in the shadow banking system are about the provision of working capital for asset managers, much like real bills provided working capital for merchants and manufacturers in Bagehot’s world over 150 years ago.”

The drivers of rising secured funding

“Indeed, the secular rise of the volume of securities financing transactions such as repos and securities lending…is closely related to the proliferation of institutional cash pools and balance sheets with structural asset-liability mismatches since 2000. The latter include the balance sheets of reserve managers (due to sterilization costs), underfunded pensions and more broadly, fixed income return expectations that failed to adjust to the secular down-drift in interest rates since the 1980s. These mismatches are the drivers behind both the ‘low bang for the buck’ lending of large volumes of long-term Treasury and agency securities for the manufacture of safe, short-term assets for institutional cash pools via dealers’ repo liabilities, and allocations to ‘high bang for the buck’ leveraged investments such as hedge funds, separate accounts and absolute return bond funds that are significant consumers of dealers’ reverse repo assets.”

“The secular rise of cash PMs could be attributed to at least three macro imbalances…

- First, on the global level, the secular rise of managed FX regimes in relation to the U.S. dollar is one explanation for the rise of cash pools held by FX reserve managers in the form of FX reserves’ liquidity tranches, which are estimated at USD1.5 trillion.

- Second, on both the global and local levels, the largest global corporations are holding more cash than ever before, estimated at more than USD1.5 trillion. Unlike in previous decades, corporations today are net funding providers. There are many possible explanations for the increase in corporate cash pools. A likely contributing factor is the long-term secular increase in corporate profits as a share.

- Third, on the local level, the rise of cash pools within the asset management complex estimated at more than USD3 trillion is explained by consolidation among asset managers, the centralized liquidity management of fund complexes, and the secular growth in securities lending and derivative overlay strategies.”

“By contrast, the secular rise of risk PMs reflects imbalances between expected future investment returns, which exceed present yields on long-term investments on an unleveraged, long-only basis.”

“From a policy perspective, the fundamental problem at hand is a financial ecosystem that has outgrown the safety net that was put around it many years ago. Today we have a different class of savers (cash PMs versus retail depositors), a different class of borrowers (risk PMs to enhance investment returns via financial leverage versus ultimate borrowers to enhance their ability to spend via loans) and a different class of intermediaries (dealers who do securities financing versus banks that finance the economy directly via loans) to whom discount window access and deposit insurance do not apply.”