A Banca d’ Italia paper reminds us that the market impact of economic data surprises depends on the state of the economy and forecast diversity. In particular, the surprise impact tends to be greater, when predictions are tightly clustered around a ‘consensus’. Conversely, uncertainty seems to help preparing markets for shocks.

Pericoli, Marcello and Giovanni Veronese (2015), “Forecaster heterogeneity, surprises and financial markets”, Banca d’Italia, Temi di Discussione (Working Papers), No. 1020, July 2015.

The below are excerpts from the paper. Headings and cursive text have been added.

Why economic data surprises matter

“Macroeconomic news should impact directly interest rates and foreign exchange rates, as they are clearly intertwined with the monetary policy stance…The updated trajectories on inflation and growth will lead to an update also of the expected path of interest rates, thereby affecting long-term yields, as well as the risk premia.”

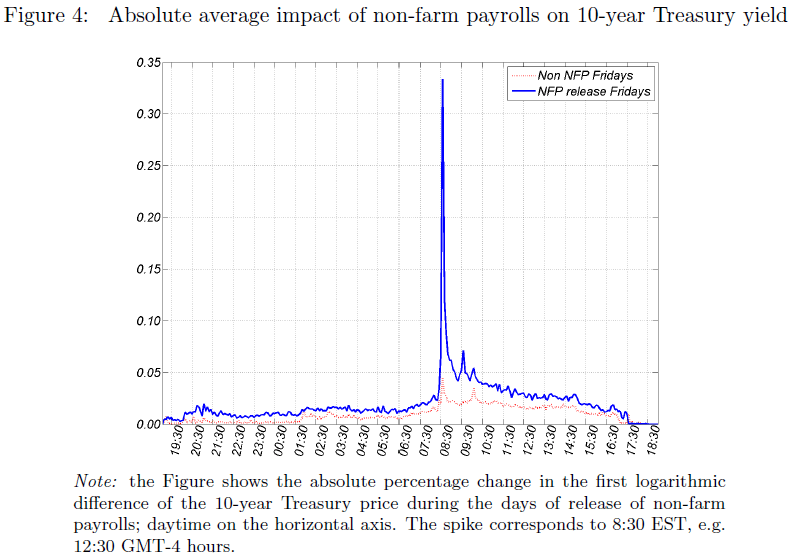

“[Among U.S. economic indicators] non-farm payrolls have the largest impact on US long-term yields (e.g. a one per cent unexpected change in non-farm payrolls increases 10-year yields by 4.23 basis points) followed by the ISM index, retail sales, the advance GDP rate of growth, and consumer confidence. Initial jobless claims and trade balance show a significant impact on long-term yields.”

Why the importance of data surprises changes

“The reaction of asset prices to macroeconomic surprises is not the result of a mechanical rule followed by market participants, but rather it depends on the state of the economy and financial markets. ..The impact of macroeconomic news on various asset classes becomes stronger when conditioning on the state of the economy.

- Markets may follow with more attention particular macroeconomic variables according to the phase of the business cycle, as well as to the policy reaction function that markets deem likely…In the late 1970s and early 1980s trade balance and unemployment were actively tracked by investors as they feared that US policymakers would respond to deficits or high unemployment…during the 2000s, the introduction of US policy targets in terms of inflation and output gap has somewhat shifted the focus of markets to more timely and coincident indicators. [Bacchetta and van Wincoop, 2013].

- [There is evidence for] a significant time variation in the responses to news of yield curves and exchange rates. …Several indicators of the state of the economy (e.g. the level of policy rates, risk conditions) influence the estimated response. In particular, US bond yields increase in response to ‘good news’, but less so when risk is elevated…reflecting some…market perceived financial stability objective for monetary policy. [Goldberg and Grisse, 2013]

- Interest rates are expected to react differently to macroeconomic news as the bound is approached… interest rates…[have become] almost insensitive to macroeconomic news after the QE program in the US, especially at the shorter horizons. [Swanson and Williams, 2014]

- As to bond markets…macroeconomic announcements are most important when they contain bad news for bond returns in expansions and, to a lesser extent, good news in contractions. [Beber and Brandt, 2010]

- US macroeconomic news are found to impact more than European news, in light of their greater timeliness. [Ehrmannn and Fratzscher, 2005]

- Asset price response to information critically depends on the degree of dispersion of prior beliefs…In particular, when beliefs heterogeneity is more pronounced the price response to news is shown to be more muted. [Ottaviani and Soerensen, 2015]”

The impact of heterogeneous beliefs

“We show that heterogeneity, proxied by the dispersion of analysts’ forecasts around each macroeconomic release, is an important source of variation in the response of asset prices. We find that the more forecasters disagree ex-ante regarding an upcoming scheduled macroeconomic announcement, the more muted is the price response to the macroeconomic surprise…This result holds for the main US macroeconomic surprises and is robust to the frequency of the data used in the estimation.”

N.B.: From a practitioner’s angle the mitigating effect of forecast disagreements on economic data surprises is plausible for many reasons. First, dispersion of forecasts is visible before the data release (conveniently in tables posted on Bloomberg) and, hence, prepares traders for the scope of possible outcomes. Second, forecasts tend to be dispersed particularly when data are subject to distortions, such as weather effects or strike action. In these cases data contain less information on underlying trend. Third, if traders rely (at least in part) on particular economists’ forecasts then diversity in predictions will translate into diversity of positions ‘into the number’. Hence, it would be less likely that the whole market is caught with the ‘wrong position’.

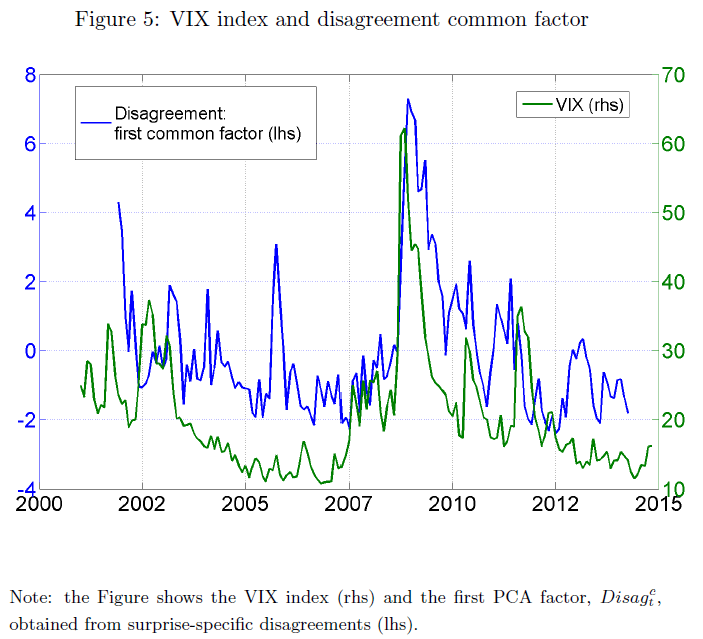

“For most indicators, disagreement displays a significant positive serial correlation…Forecaster heterogeneity regarding several US key macroeconomic indicators is driven not only by variable-specific factors, but also by a sizeable common component. This common component displays some co-movement with the VIX index, a popular proxy of global risk aversion and overall economic uncertainty.”

Annex: Basics of the empirical analysis

“We analyze the impact of macroeconomic surprises and individual heterogeneity on exchange rates and long-term interest rates in the United States and in Germany from 1999 to 2014. The time span allows the comparison of surprises impact during normal times, during the global financial crisis, and during the implementation of the unconventional measures of monetary policy.”

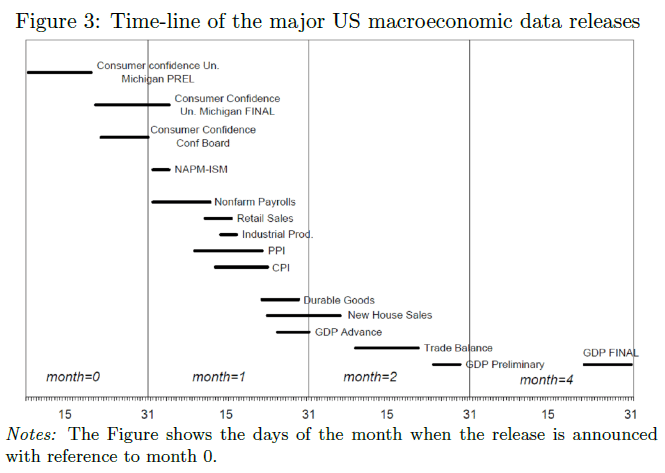

“We use the Bloomberg real-time data on the expectations and realizations of the most relevant U.S. macroeconomic indicators to estimate announcement surprises. The Bloomberg economic calendar contains a survey of economists’ forecasts for each US scheduled macroeconomic release. Surprises are defined as the difference between the median forecast and the actual announcement… In our analysis we consider a set of 12 US key macroeconomic indicators.”

“We use our novel dataset on US macroeconomic surprises and disagreement in conjunction with the US dollar-euro exchange rate and long term interest rates in the US and in Germany.”

“Forecasters heterogeneity is found to vary considerably across releases…We exploit this unique source of information obtained from Bloomberg to construct an announcement specific measure of forecaster heterogeneity. Accordingly, we define disagreement as the standard deviation of their forecasts.”

“The actual release often falls outside the support of the distribution of forecasters expectations, suggesting that beyond the difficulty to forecast a particular indicator, there also may be a general tendency to cluster around the consensus median, in order to avoid extreme deviations from the average forecast…Considerable differences exist across indicators: more than a quarter of the Non-farm payrolls releases fall outside the analysts range of forecasts, compared to less than 5 per cent for the advance GDP growth.”